I’m proud to feature our first guest post! Michael L. is the creator of Super Millennial. He teaches people how to evaluate their financial situation, simplify money management & learn how to automate their investments to reach their financial goals. Subscribe for his personal finance “Keys To Success” PDF and blog updates HERE.

Note from FP: I was inspired to have Michael share this post after talking with several friends who insisted that individual stock picking was their path to wealth. I’m a diehard index investor and fully believe that any investor should keep their investing life as simple as possible. As Michael explains, you should be lazy when it comes to investing. I couldn’t agree more.

Enjoy what Super Millennial has to share with us!

Simplicity, it’s what we all want to achieve in every area of our life. That’s why we have Netflix instead of cable (plus it’s cheaper), endless two day Amazon Prime deliveries, or Postmates making your favorite restaurant deliverable….This post will show you how simple it is to do even in your financial life!

Hopefully by now you understand how important it is to invest in the stock market to grow your money over time. As the saying goes, “No one ever got rich from a savings account”, especially nowadays with less than one percent interest. But the next question many people ask is where do I invest? Should you buy stocks, bonds, mutual funds, or even invest in gold online? This question alone shows why a lot of people avoid the market entirely, it’s complicated!

Honestly you don’t have to be a genius, wall street guru, or financial analyst to be a smart investor at any age. All you need to do is focus on investing in low cost index funds in your 401K, Roth IRA, or brokerage accounts INSTEAD of picking individual stocks. Make it a habit over time and your money will be diversified, have low management fees, and track the market, which historically over time has averaged roughly 8% returns over the past century, slightly better than your >.1% savings account.

While everyone wants to be Gordon Gekko or Jordan Belfort as a stock picking guru/day trader, the chances of success are very small for the average investor. Picking stocks is expensive, takes time to research the companies, and can be a lot riskier than index funds. By picking stocks individually you:

- Have a lot of your “eggs” in one basket. Example: If the company has a bad earnings call or something affects the stock your investment will be directly related.

- Live and die by one company. This happens a lot when people invest their 401K or employee stock into their employer, there may be benefits but it can also cloud your judgement as you’re already emotionally invested to the company.

- Have to stay actively engaged & research the stock. Who wants to read earnings calls, understand a balance sheet & learn their price to earnings (P/E) ratio? Just typing that made me bored…

Is index investing as sexy as buying Netflix seven years ago and making 300% gains? Or Amazon or Apple a few years ago? The simple answer is NO, but unless you have a few hours a week to study each stock in your portfolio don’t bother with individual stocks until you have a decent amount of wealth built up. Instead of stock picking focus on index funds or consider direct indexing for a more personalized approach! !

What’s an index fund?

As the name implies, index funds follow a specific index (like the S&P 500 or Dow Jones). Historically these have returned ~8-9% returns annually. While you may get more in some years from individual stock picking you may also lose a lot more on down years. Index funds try to keep performance consistent and reliable.

Investopedia defines it as “A type of mutual fund with a portfolio constructed to match or track the components of a market index, such as the Standard & Poor’s 500 Index (S&P 500). An index mutual fund is said to provide broad market exposure, low operating expenses and low portfolio turnover.”

Basically it means that index funds are a single fund that invests in HUNDREDS of individual stocks or bonds. Let’s look at an example to simplify;

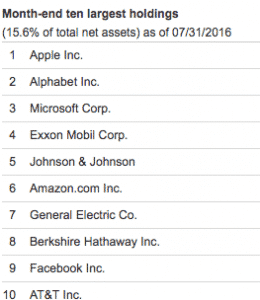

VTI (the stock ticker symbol) is known as the Vanguard Total US Stock Market Index. One of the biggest funds available; it currently holds 3,682 stocks worth $458 BILLION.

Here are the 10 biggest stocks in the fund:

All are very big companies and would take thousands of dollars to invest in each company. Instead with an index fund you get to be partially invested in all of these big 10 companies and thousands of others instead of buying each stock individually. This is an example of an index STOCK fund, meaning no bonds are in these funds. An example of a bond fund would be BND; a fund that has 7,911 bonds that make the fund worth $171 billion.

Now you’ve understood the “hard” part about the original question…Where do I invest my money?

Next up is understanding how to be LAZY with your portfolio to keep the theme of simplicity going.

In fact you want to make your strategy as lazy as possible, which is known as a LAZY portfolio. This is the only time I’m asking you to be lazy in life but it’s a strategy I have implemented and don’t have much stress when it comes to contributing to my portfolio. “Lazy Portfolios” are meant for you to be able to invest in a few funds and be fully diversified with just a few clicks.

Make sure you are comfortable with your asset allocation and figure out which percentage of stocks/bonds will match your risk tolerance. Here is an example of a TWO fund portfolio which is great if you’re just starting out & think investing is hard!

LAZY PORTFOLIO Example

Pros

- Low management fees (which means you keep more $$$)

- Low minimum investment (1 share of each)

- ***As of 8/23/16 VTI is trading at $112/share & BND is trading at $84/share

- Passively Managed

- Diversified (between the two funds you have 3,682 stocks in VTI & 7,911 bonds in BND

Cons

- Doesn’t have any international exposure

This portfolio is good for beginning investors who don’t have a ton of capital and want to keep it as simple as possible. It can also be a great place to start and build upon. If you’d like international exposure as well, look at VXUS, which is a total international stock fund that is invested in 6,041 different international stocks. By choosing two or three funds you have an extremely low cost, diversified portfolio. Does this seem much easier than studying and buying each stock, or even the top ten in the funds? It should!

Most people don’t invest until it’s too late because it seems tedious, they don’t understand how to, or where to invest & because it requires constant upkeep (who wants that?). Lazy portfolios are the exact opposite & make your life simple. Next time you decide to procrastinate on making your first investment read this post to remember how SIMPLE this is…Lazy Portfolios will let you set it & forget it!

And that’s the goal, to keep our lives simple and easy.

This post may contain affiliate links.

More Recommended Ebike/Scooters

Check out these other ebikes and scooters I've reviewed:

- Urban Arrow Ebike – Last year, I made one of the largest purchases I’ve ever made – I bought a $9,000 electric cargo bike from Urban Arrow. In my Urban Arrow review, I will discuss what it is and why I decided to buy this bike, as well as discuss how impactful a bike like this can be on your journey to financial independence.

- Troxus Explorer Step-Thru Ebike – The Troxus Explorer Step-Thru is a fat-tire ebike that I’ve had the pleasure of riding for a while now. It has amazing power, great looks, and awesome range. If you’re looking for a great fat-tire ebike that offers a lot for the price, the Troxus Explorer Step-Thru is definitely one for you to consider. Check out my Troxus Explorer Step-Thru Review.

- Hovsco HovBeta Ebike – The HovBeta is a folding ebike with great specs and a lot of interesting features, and importantly, it’s sold at a good price point. I’ve had a blast commuting with it and using it to do deliveries with DoorDash, Uber Eats, and Grubhub. Check out my Hovsco HovBeta Ebike Review.

- Vanpowers Manidae Ebike – The Vanpowers Manidae is a fat tire ebike that I’ve been riding as my primary winter commuting bike and have also been using it to do food delivery with apps like DoorDash, Uber Eats, and Grubhub. After clocking in a decent number of miles with this ebike, I wanted to write a post sharing what my experience with the Vanpowers Manidae ebike has been like. Check out my Vanpowers Manidae Review.

- Sohamo S3 Step-Thru Folding EBike Review – A Great Value Folding Ebike – The Sohamo S3 Step-Thru Folding Ebike is an entry-level folding ebike that offers a lot of value for the price point. I’ve been riding the Sohamo S3 for a while now, putting the bike through its paces, and I have to say, this bike has exceeded all of my expectations. Check out my Sohamo Review.

- KBO Flip Ebike – The KBO Flip is an excellent bike. I’ve had a great time riding it and think it’s a versatile bike that can be used for a lot of purposes and can fit a variety of lifestyles. It’s worked out great for me as a general commuter bike and as a food delivery bike. Check out my KBO Flip Review.

- Hiboy P7 Commuter Ebike – The Hiboy P7 is an excellent electric commuter bike that’s offered at an affordable price point. The range and speed of this bike are both very good, so you won’t have any trouble getting anywhere you need to go with it. As a food delivery vehicle, this is also good – with how much range it offers, you’ll be able to work all day on a single charge. Check out my Hiboy P7 Commuter Electric Bike Review.

- Himiway Escape Ebike – The Himiway Escape is an interesting bike for anyone looking for a moped-style ebike. If you’re a gig economy worker, the Himiway Escape is particularly interesting and it’s possible to think of it as an investment, especially if you can opt to do deliveries with the Himiway versus using a car. It’s not cheap, but you can definitely make your money back when you compare the mileage you’ll put on your car versus using an ebike. Check out my Himiway Escape Bike Review.

- Espin Sport Ebike – The Espin Sport is a good ebike for someone who is looking for an ebike that feels and rides more like a regular bike. There are many ebikes that are really only bikes in name. In reality, they’re basically electric mopeds. The Espin Sport, by contrast, is a bike you could probably ride without the battery and you’d feel like you’re just riding a regular bike. Check out my Espin Sport Review.

- Varla Eagle One Scooter – The Varla Eagle One is an excellent scooter that can make sense for a lot of people. It can work as a primary mode of transportation. You can use it to work on gig economy apps like DoorDash, Uber Eats, and Grubhub. And it can also be a recreational vehicle if you’d prefer to use it for that. Check out my Varla Eagle One Review.

- Varla Falcon Scooter – The Varla Falcon is an excellent scooter that offers a good amount of power at a lower price point compared to more powerful scooters. It’s not exactly an entry-level scooter, nor is it a high-powered scooter. I think it fits somewhere in-between those two categories – an intermediate scooter if I had to give it a category. Check out my Varla Falcon Review.

- Hiboy S2 Scooter – The Hiboy S2 is an excellent entry-level commuter scooter that's perfect for someone looking to save some money in transportation costs and improve their commute. Check out my Hiboy S2 Review.

- Hiboy S2R Scooter – The Hiboy S2R is one of the more interesting electric scooters I’ve been able to test out. It’s not a high-powered scooter, but for an everyday transport option, it’s very useful, especially given some of the unique features that it has. Indeed, for the price, the Hiboy S2R might be the best value scooter I’ve used. Check out my Hiboy S2R Review.

- Fucare H3 Scooter – The Fucare H3 is a fun scooter and I’ve enjoyed testing it out. For a daily commuter or quick trips or errands, the Fucare H3 is probably the scooter I’ll use. It’s portable and easy to maneuver, so it’s just easier to take on the road when I need it. Check out my Fucare H3 Scooter Review.

More Recommended Investing App Bonuses

For additional investing app bonuses, be sure to check out the ones below:

- M1 Finance ($75) – This is a great robo-advisor that has no fees and allows you to create a customized portfolio based on your risk tolerance. You also get $75 for opening an account. Check out my M1 Finance Referral Bonus – Step-By-Step Guide.

- SoFi Invest ($25) – SoFi Invest is an easy brokerage account bonus that you can earn with just a few minutes of work. Use my SoFi Invest referral link, fund your SoFi Invest brokerage account with just $10 and you’ll get $25 of free stock. I also have a step-by-step guide for the SoFi Invest referral bonus.

- Robinhood (1 free stock) – Robinhood gives you a free stock valued between $2.50-$225 if you open an account using my referral link.

- Public (1 free stock) - Public gives you a free stock valued between $3-$70 if you open an account using my referral link.

More Recommended Bank Account Bonuses

If you’re looking for more easy bank bonuses, check out the below options. These bonuses are all easy to earn and have no fees or minimum balance requirements to worry about.

- Ally Bank ($100) – Of all the banks out there, Ally is, without a doubt, my favorite. At the moment, Ally is offering $100 to customers who open an eligible Ally account and meet the requirements. Here are the step-by-step directions to earn your Ally Bank referral bonus.

- Chime ($100) - Chime is a free bank account that offers a referral bonus if you use a referral link and complete a direct deposit of $200 or more. In practice, any ACH transfer into this account triggers the bonus. This bonus is easy to earn and posts instantly, so you’ll know if you met the requirements as soon as you move money into the account. I wrote a step-by-step guide on how to earn your Chime referral bonus that I recommend you check out.

- US Bank Business ($400/$1200) – This is a fairly easy bank bonus to earn, since there are no direct deposit requirements. In addition, you can open the Silver Business Checking account, which comes with no monthly fees. Check out how to earn this big bonus here.

- Current ($50) – Current is a free fintech bank that’s offering new users a $50 referral bonus after signing up for an account using a referral link. Current is an easy bonus to earn and also gives you access to three savings accounts that pay you 4% interest on up to $2,000. That means you can put away up to $6,000 earning 4% interest. That’s very good and makes Current an account I recommend to everyone. Check out my step-by-step guide on how to earn your Current Bank bonus.

- Novo Bank ($40) - Novo bank is a free business checking account that’s currently offering a $40 bonus if you open a Novo business checking account using a referral link. In addition to being a good bank bonus, Novo is also a good business checking account. It has no monthly fees or minimum balance requirements and operates a good app and website. Indeed, it’s the business checking account I currently use for this blog. Check out my post on how to easily open a Novo account.

- Varo ($25) – Varo is a free fintech banking app similar to Chime or Current. It’s currently offering a $25 bonus to new users that open a new Varo account with a referral link. The bonus for this bank is very easy to meet, all you need to do is spend $20 within 30 days of opening your Varo account. Check out my step-by-step guide to learn how to earn this bonus.

Kevin is an attorney and the blogger behind Financial Panther, a blog about personal finance, travel hacking, and side hustling using the gig economy. He paid off $87,000 worth of student loans in just 2.5 years by choosing not to live like a big shot lawyer.

Kevin is passionate about earning money using the gig economy and you can see all the ways he makes extra income every month in his side hustle reports.

Kevin is also big on using the latest fintech apps to improve his finances. Some of Kevin's favorite fintech apps include:

- SoFi Money. A really good checking account with absolutely no fees. You'll get a $25 referral bonus if you open a SoFi Money account with a referral link, and an additional $300 if you complete a direct deposit.

- 5% Savings Accounts. I'm currently getting 5.24% interest on my savings through a company called Raisin. Opening a Raisin account takes minutes to complete, it's free, and all of your funds are FDIC-insured. I explain how it works, why I'm now using it to store my emergency fund and any other cash savings I have, and why I recommend everyone check it out in this review.

- US Bank Business. US Bank is currently offering new business customers a $400/$1200 signup bonus after opening a new account and meeting certain requirements.

- M1 Finance. This is a great robo-advisor that has no fees and allows you to create a customized portfolio based on your risk tolerance. You also get $75 for opening an account.

- Empower. One of best free apps you can use to monitor your portfolio and track your net worth. This is one of the apps I use to track my financial accounts.

Feel free to send Kevin a message here.

I am a lazy investor too! Index fund ETFs all the way. Over the past 6 years, they have out performed my ‘stock picking’ so now I don’t try and stock pick anymore

It’s just like Warren Buffett’s bet. A portfolio of 90% invested in s&p and 10% invested in bonds will beat out any hedge fund / activist investing portfolio. I believe in it, which is exactly how my 401k is structured!

Buffett’s bet is awesome, he’s always talking about index funds and he’s worth 60+ Billion, you think people would listen to him more lol. My 401K is the same, very asset heavy since I’m not planning on touching for another 30 years!

Thanks for reading

I’m a boring stock picker. I do have a 3 index funds and some mutual funds but I mainly stick to dividend paying stocks. If you stick to dividend paying stocks you almost can’t go wrong.

Do you have your dividend stocks in taxable accounts?

Great post!

“Honestly you don’t have to be a genius, wall street guru, or financial analyst to be a smart investor at any age.” I think this is such an important point to drive home. Many people are afraid to start investing because they don’t think they know enough, but just STARTING to invest is the most important thing they can do. We invest in mostly index funds with Vanguard. Easy peasy (and lazy), but it works.

That’s great! Really it doesn’t have to be hard. You really only need enough return to get you to your goals. So why take on added risk or use up more time for additional return if you don’t need it. If your starting young, you don’t need 20% a year to get there!

And when you’re young, the thing that really matters is savings rate. You need to accumulate money first before rate of return really matters a ton. So make it easy so you can accumulate money.

Thanks I appreciate it! I know that’s why I was so delayed in investing, I thought it was to hard to understand and didn’t want to lose money! Vanguard index funds make it simple for sure and you can always add stocks on in the future.

I understand the “easy peasy (and lazy)” approach, but investing without a protective stop loss in case the markets roll over like 2000, 2008 or godforbid the Great Depression where markets fell -80% and didn’t make new highs for 20 years just makes me too nervous.

Investing without some sort of exit plan for each investment can be a dangerous game, especially in an environment of a sluggish economy and low yields (meaning, you won’t be able to recoup your losses fast enough to maintain your standard of living).

Working as a 23yr old at Bear Stearns in 2008 during it’s collapse struck a chord with me. Since that time, I declared that losing a ton or all of my money in a bear market (or in any scenario) was never going to happen to me. Without a protective stop-loss on each investment, you’re susceptible to catastrophic losses whether you realize it or not.

I’ve got a friend who’s big on stock picking vs indexing and I’ve got the perfect post now to show him more reasons why I prefer indexing. Great post and I completely agree!

Definitely all about keeping it simply!

Thanks I appreciate it! As fun as it can be to pick a good stock and cash out at the right time it’s way to time consuming & risky for me. I dedicate all 401K/Roth to index …set it and forget it. Only thing I like being lazy at in life hah

Index investing is great for people who don’t want to do any work into investing and are happy with the market return. Stock picking requires a lot more work but it can provide substantially higher returns, not to mention it makes you aware of what you are buying or investing in. As an example, S&P 500 have had a return of merely 5 or 6% for the past year whereas my individual stock portfolio of 40 or so stocks have returned nearly 20% for the same period. Yes, it takes a lot of work to pick stocks and then monitor them, but again I enjoy doing the work as I find learning about businesses very interesting and overtime I would only get better at it.

Do you plan to do individual stock picking forever or is it just a fun thing you do? In other words, do you pick stocks with retirement money or just fun money?

It’s not a fun money, it’s the money I have earned and saved over the course of 20 some years and invested over time in individual dividend paying stocks so that it can provide income when I leave my job which I did recently.

I look at managing a stock portfolio as running a business, if you want it to do well, you have to put work into it. There is just no easy money at least not the one that would stick around.

Would I do individual stock picking forever? Forever is a long time, but I do plan to continue doing this as long as I can. I am only 43, so I could do this for many more years before I get tired and completely retire and may be then I switch over to Index Funds. I do invest in Index Funds but only in my traditional retirement accounts where individual stocks are allowed.

Correction: I do invest in Index Funds but only in my traditional retirement accounts where individual stocks are NOT allowed. Besides, the very long term horizon of those accounts make Index investing more appealing.

Completely agree! In the future I’ll be adding individual stocks with money not associated with retirement hoping for greater returns. For beginner – intermediate I think index is always the way to go since the research is minimal (just find funds w/low fees), set it, and forget it. The other downside w/individual stocks is how expensive it is to get a diversified portfolio compared to index.

As long as you’re doing your hw I love it, way to go w/the 20% returns that super impressive! Do you index for your 401K/IRA?

Thanks, yes, I index in my 401k and it has been that way for a long time, it’s like being on an auto-pilot and I don’t worry about it much.

My taxable brokerage account is where I keep my individual stock portfolio. Starting out, it is expensive but once the portfolio is up and running, can take few years, the turnover rate can be quite low, especially if you are buying good dividend paying stocks. I hardly ever sell any of my stocks, so most of my transactions are to buy shares in existing or new stocks that are at or below fair value. It is very satisfying to see the portfolio grow and generate dependable income.

Set and forget typically works better when your investments appreciate in value. When they don’t, you tend you “remember” and look at your investments a lot more often even if you know your strategy is to leave them alone – to let em ride up and down.

To improve your ability to stick to your system through major ups and downs, you may consider implementing a stop-loss rule to exit your investments in case a major bear market develops. A stop loss protects profits and principal during downtrends, but it can subject you to whipsaws where you stop out at/near the bottom only to watch the recovery. If this happens, you need some rule to get back in.

Resting on the belief that markets always go up over the “long run” can be dangerous for your investing results. One big downtrend and your financial situation can take a major hit.