One of the things I enjoy about the current state of the side hustling world is just how easy it is to fit various side hustles into your day-to-day life. We live in a really unique time in history where it’s actually possible to piecemeal a few bucks here and there whenever you want.

When you think about it, even just 10 years ago, things were vastly different. All of these gig economy and sharing economy apps didn’t exist yet and if you wanted to make extra money, you basically had to find a part-time job or create your own side hustle. A part-time job meant that you had to work shifts with no flexibility or ability to incorporate whatever you were doing into your day-to-day life. And creating a side hustle often required capital and time to actually build it up so that it earned income.

The big thing was that you couldn’t just go out and make 5 or 10 bucks randomly when you felt like it. Contrast that with today’s world, where I can literally turn on my phone, step out of my front door, and make 5 or 10 bucks with a few minutes of work using any of the sharing or gig apps I have on my phone.

There’s a lot of power in being able to earn income in small, piecemeal chunks like this. Not all of us have the time to go out and work several hours a day on some side project in the hopes that it generates an income eventually. But I bet most of us can spare thirty minutes or an hour each day doing something from one of the many sharing economy and gig economy apps out there. In fact, many of us can probably fit these different gigs into the things we’re already doing.

And if you’re willing to do this, you can literally become a millionaire and financially independent without doing anything else. You just have to take advantage of something you could call, the Reverse Latte Factor.

The Latte Factor Versus The Reverse Latte Factor

The Latte Factor is something that many of us in the personal finance community have heard about. Initially coined by David Bach in his book The Automatic Millionaire, it basically tells you to cut out small, frivolous expenses in your day-to-day life, invest the savings, and over time, you’ll have a lot more money simply due to the power of compound interest.

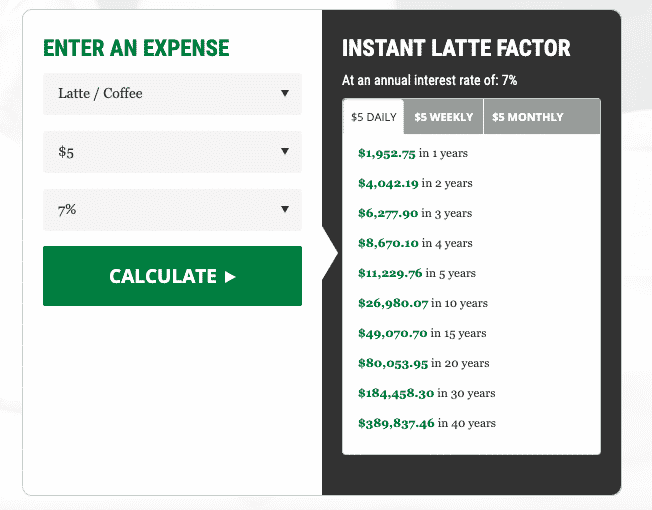

Bach has a calculator on his website that shows you just how powerful saving small amounts on a daily basis can be. For example, according to his Latte Factor Calculator, saving $5 per day at an annual return of 7% adds up to over $180,000 over the course of 30 years.

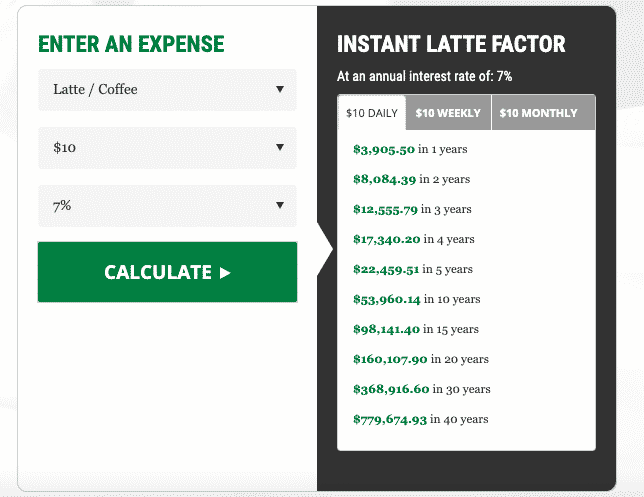

Double that to just $10 per day and naturally, you double what you’ll have in 30 years – to over $360,000.

The latte factor is a bit of a contentious topic because, for many, it’s not these small expenses that are hindering financial progress, but rather larger issues, such as stagnant wages and the high costs of education, housing, and healthcare.

I totally agree with that assessment, but I think a lot of the latte factor hate misses the point that it’s really making – that consistency matters. Small things by themselves don’t mean much. But small things, done consistently over time, well, that means something.

The thing that always confused me about the latte factor was how it emphasized all of the lost opportunity that comes with daily frivolous spending, but never seemed to consider the opposite – that is, the lost opportunity that comes with not going out and earning extra income on a consistent, daily basis.

This is a much more interesting way to think about the latte factor. Because if saving small amounts of money each day adds up over time, what happens if we go out and earn small amounts of money each day?

There’s an opportunity cost with not going out and earning extra income on a consistent basis. And all of us have the ability to do this. When we choose not to, we’re really missing out on something.

We can call this the Reverse Latte Factor. And here’s how impactful it really is.

The Reverse Latte Factor And What It Means

Below is a chart showing what you could have in 30 years if you consistently make an extra couple of bucks every single day and invest all of it (the chart assumes a 7% average annual rate of return, which I think is a reasonable assumption).

| Amount Earned Per Day | Total in 30 Years |

|---|---|

| $5 | $184,458.30 |

| $10 | $368,916.60 |

| $15 | $553,374.90 |

| $20 | $737,833.20 |

| $25 | $922,291.50 |

| $30 | $1,106,749.80 |

The math is pretty amazing because if I’m looking at this right, what it means is that a mere $10 per day of extra income comes out to over $300,000 over a 30-year period. If you double that to $20 per day, you’re looking at over $700,000. Triple it to $30 per day, and you’ll be a millionaire literally from doing random, low-level gigs that most people will think are pretty stupid.

This is pretty incredible to think about. Depending on where you live and what’s around you, an extra $30 per day is completely possible. Most people, with a little bit of practice, can make that in an hour or a little over an hour just by taking advantage of gig economy apps.

Just looking at how I typically make an extra $30 or more per day:

- Earn $16-$25 by grabbing four to six Lime scooters in the evening, charging them up overnight, then dropping them off in the morning on my way to work. This is easy for me to do because there are usually dozens of scooters all around my neighborhood at the end of the day.

- Earn $10-$20 delivering food on my bike on my way home from work. And since I’m doing my deliveries on a bike, I’m getting the added benefit of exercising too – which is something I have to do anyway.

- Earn $11 to $16 walking some dogs with Wag during lunch. This isn’t difficult for me to do since my coworking space is downtown and there are a lot of apartments within blocks of me. And like with biking, it gives me exercise, which I have to do anyway.

To understand what an extra $30 per day means, that equals just $913 of extra income per month. This is totally doable for most people given the current landscape of the sharing and gig economy. Indeed, over the past three years, I’ve regularly earned between $1,000 and $3,000 per month just by doing these different, sometimes silly sounding, gigs.

Heck, even just an extra $10 per day adds up to a significant sum over time – and I don’t think it’s unreasonable to think that anyone can do that with 30 minutes or less of work each day. If we believe that our daily latte can cost us hundreds of thousands of dollars over our lifetime, the same is true for those of us simply unwilling to go figure out ways to earn a few extra bucks each day. In other words, the Reverse Latte Factor really means something.

Takeaways

The Reverse Latte Factor is an important thought experiment about how impactful small amounts of extra money added up consistently over time can be to your finances. And the beauty of the Reverse Latte Factor is that it doesn’t require you to give up all of the little pleasures in your life.

I have so much fun doing all of these different gigs. And my guess is most of you reading this can probably find something that makes you money that you also find fun to do. Cutting stuff from our budget though, where’s the fun in that?

To sum it all up, earning an extra $5 each day might not seem like a big deal. But keep doing that every single day, and suddenly, it means something. It costs us much more than we think to sit around and not take advantage of all of the ways to earn extra income each day.

If you understand this, it might make the Reverse Latte Factor something that you really need to think about more.

This post may contain affiliate links.

More Recommended Ebike/Scooters

Check out these other ebikes and scooters I've reviewed:

- Urban Arrow Ebike – Last year, I made one of the largest purchases I’ve ever made – I bought a $9,000 electric cargo bike from Urban Arrow. In my Urban Arrow review, I will discuss what it is and why I decided to buy this bike, as well as discuss how impactful a bike like this can be on your journey to financial independence.

- Troxus Explorer Step-Thru Ebike – The Troxus Explorer Step-Thru is a fat-tire ebike that I’ve had the pleasure of riding for a while now. It has amazing power, great looks, and awesome range. If you’re looking for a great fat-tire ebike that offers a lot for the price, the Troxus Explorer Step-Thru is definitely one for you to consider. Check out my Troxus Explorer Step-Thru Review.

- Hovsco HovBeta Ebike – The HovBeta is a folding ebike with great specs and a lot of interesting features, and importantly, it’s sold at a good price point. I’ve had a blast commuting with it and using it to do deliveries with DoorDash, Uber Eats, and Grubhub. Check out my Hovsco HovBeta Ebike Review.

- Vanpowers Manidae Ebike – The Vanpowers Manidae is a fat tire ebike that I’ve been riding as my primary winter commuting bike and have also been using it to do food delivery with apps like DoorDash, Uber Eats, and Grubhub. After clocking in a decent number of miles with this ebike, I wanted to write a post sharing what my experience with the Vanpowers Manidae ebike has been like. Check out my Vanpowers Manidae Review.

- Sohamo S3 Step-Thru Folding EBike Review – A Great Value Folding Ebike – The Sohamo S3 Step-Thru Folding Ebike is an entry-level folding ebike that offers a lot of value for the price point. I’ve been riding the Sohamo S3 for a while now, putting the bike through its paces, and I have to say, this bike has exceeded all of my expectations. Check out my Sohamo Review.

- KBO Flip Ebike – The KBO Flip is an excellent bike. I’ve had a great time riding it and think it’s a versatile bike that can be used for a lot of purposes and can fit a variety of lifestyles. It’s worked out great for me as a general commuter bike and as a food delivery bike. Check out my KBO Flip Review.

- Hiboy P7 Commuter Ebike – The Hiboy P7 is an excellent electric commuter bike that’s offered at an affordable price point. The range and speed of this bike are both very good, so you won’t have any trouble getting anywhere you need to go with it. As a food delivery vehicle, this is also good – with how much range it offers, you’ll be able to work all day on a single charge. Check out my Hiboy P7 Commuter Electric Bike Review.

- Himiway Escape Ebike – The Himiway Escape is an interesting bike for anyone looking for a moped-style ebike. If you’re a gig economy worker, the Himiway Escape is particularly interesting and it’s possible to think of it as an investment, especially if you can opt to do deliveries with the Himiway versus using a car. It’s not cheap, but you can definitely make your money back when you compare the mileage you’ll put on your car versus using an ebike. Check out my Himiway Escape Bike Review.

- Espin Sport Ebike – The Espin Sport is a good ebike for someone who is looking for an ebike that feels and rides more like a regular bike. There are many ebikes that are really only bikes in name. In reality, they’re basically electric mopeds. The Espin Sport, by contrast, is a bike you could probably ride without the battery and you’d feel like you’re just riding a regular bike. Check out my Espin Sport Review.

- Varla Eagle One Scooter – The Varla Eagle One is an excellent scooter that can make sense for a lot of people. It can work as a primary mode of transportation. You can use it to work on gig economy apps like DoorDash, Uber Eats, and Grubhub. And it can also be a recreational vehicle if you’d prefer to use it for that. Check out my Varla Eagle One Review.

- Varla Falcon Scooter – The Varla Falcon is an excellent scooter that offers a good amount of power at a lower price point compared to more powerful scooters. It’s not exactly an entry-level scooter, nor is it a high-powered scooter. I think it fits somewhere in-between those two categories – an intermediate scooter if I had to give it a category. Check out my Varla Falcon Review.

- Hiboy S2 Scooter – The Hiboy S2 is an excellent entry-level commuter scooter that's perfect for someone looking to save some money in transportation costs and improve their commute. Check out my Hiboy S2 Review.

- Hiboy S2R Scooter – The Hiboy S2R is one of the more interesting electric scooters I’ve been able to test out. It’s not a high-powered scooter, but for an everyday transport option, it’s very useful, especially given some of the unique features that it has. Indeed, for the price, the Hiboy S2R might be the best value scooter I’ve used. Check out my Hiboy S2R Review.

- Fucare H3 Scooter – The Fucare H3 is a fun scooter and I’ve enjoyed testing it out. For a daily commuter or quick trips or errands, the Fucare H3 is probably the scooter I’ll use. It’s portable and easy to maneuver, so it’s just easier to take on the road when I need it. Check out my Fucare H3 Scooter Review.

More Recommended Investing App Bonuses

For additional investing app bonuses, be sure to check out the ones below:

- M1 Finance ($75) – This is a great robo-advisor that has no fees and allows you to create a customized portfolio based on your risk tolerance. You also get $75 for opening an account. Check out my M1 Finance Referral Bonus – Step-By-Step Guide.

- SoFi Invest ($25) – SoFi Invest is an easy brokerage account bonus that you can earn with just a few minutes of work. Use my SoFi Invest referral link, fund your SoFi Invest brokerage account with just $10 and you’ll get $25 of free stock. I also have a step-by-step guide for the SoFi Invest referral bonus.

- Robinhood (1 free stock) – Robinhood gives you a free stock valued between $2.50-$225 if you open an account using my referral link.

- Public (1 free stock) - Public gives you a free stock valued between $3-$70 if you open an account using my referral link.

More Recommended Bank Account Bonuses

If you’re looking for more easy bank bonuses, check out the below options. These bonuses are all easy to earn and have no fees or minimum balance requirements to worry about.

- Ally Bank ($100) – Of all the banks out there, Ally is, without a doubt, my favorite. At the moment, Ally is offering $100 to customers who open an eligible Ally account and meet the requirements. Here are the step-by-step directions to earn your Ally Bank referral bonus.

- Chime ($100) - Chime is a free bank account that offers a referral bonus if you use a referral link and complete a direct deposit of $200 or more. In practice, any ACH transfer into this account triggers the bonus. This bonus is easy to earn and posts instantly, so you’ll know if you met the requirements as soon as you move money into the account. I wrote a step-by-step guide on how to earn your Chime referral bonus that I recommend you check out.

- US Bank Business ($400/$1200) – This is a fairly easy bank bonus to earn, since there are no direct deposit requirements. In addition, you can open the Silver Business Checking account, which comes with no monthly fees. Check out how to earn this big bonus here.

- Current ($50) – Current is a free fintech bank that’s offering new users a $50 referral bonus after signing up for an account using a referral link. Current is an easy bonus to earn and also gives you access to three savings accounts that pay you 4% interest on up to $2,000. That means you can put away up to $6,000 earning 4% interest. That’s very good and makes Current an account I recommend to everyone. Check out my step-by-step guide on how to earn your Current Bank bonus.

- Novo Bank ($40) - Novo bank is a free business checking account that’s currently offering a $40 bonus if you open a Novo business checking account using a referral link. In addition to being a good bank bonus, Novo is also a good business checking account. It has no monthly fees or minimum balance requirements and operates a good app and website. Indeed, it’s the business checking account I currently use for this blog. Check out my post on how to easily open a Novo account.

- Varo ($25) – Varo is a free fintech banking app similar to Chime or Current. It’s currently offering a $25 bonus to new users that open a new Varo account with a referral link. The bonus for this bank is very easy to meet, all you need to do is spend $20 within 30 days of opening your Varo account. Check out my step-by-step guide to learn how to earn this bonus.

Kevin is an attorney and the blogger behind Financial Panther, a blog about personal finance, travel hacking, and side hustling using the gig economy. He paid off $87,000 worth of student loans in just 2.5 years by choosing not to live like a big shot lawyer.

Kevin is passionate about earning money using the gig economy and you can see all the ways he makes extra income every month in his side hustle reports.

Kevin is also big on using the latest fintech apps to improve his finances. Some of Kevin's favorite fintech apps include:

- SoFi Money. A really good checking account with absolutely no fees. You'll get a $25 referral bonus if you open a SoFi Money account with a referral link, and an additional $300 if you complete a direct deposit.

- 5% Savings Accounts. I'm currently getting 5.24% interest on my savings through a company called Raisin. Opening a Raisin account takes minutes to complete, it's free, and all of your funds are FDIC-insured. I explain how it works, why I'm now using it to store my emergency fund and any other cash savings I have, and why I recommend everyone check it out in this review.

- US Bank Business. US Bank is currently offering new business customers a $400/$1200 signup bonus after opening a new account and meeting certain requirements.

- M1 Finance. This is a great robo-advisor that has no fees and allows you to create a customized portfolio based on your risk tolerance. You also get $75 for opening an account.

- Empower. One of best free apps you can use to monitor your portfolio and track your net worth. This is one of the apps I use to track my financial accounts.

Feel free to send Kevin a message here.

Are there any examples of sharing or gig economy apps that you have used or would recommend to earn extra income through the Reverse Latte Factor?

Recently, I’ve been trying to land gigs on freelancer websites, but to no avail. What do you think is happening please?

I read you have a saving account with 2.1% return? If I read correctly, please let me know how to sign up for this account at 2.1% return! Thanks

“The thing that always confused me about the latte factor was how it emphasized all of the lost opportunity that comes with daily frivolous spending, but never seemed to consider the opposite – that is, the lost opportunity that comes with not going out and earning extra income on a consistent, daily basis.”

Yessss!

I’m planning to use one stream of side income for investing 🙂

I agree with your assessment of doing more side hustles. One of the funniest side hustles I’ve seen during the pandemic is a guy working another full-time job from home, just because he can and has a lot more time and productivity.

I worked on Financial Samurai for 2 years 9 months, then I broke free in 2012. You never know!

Sam

I have only been reading the panther report for a few weeks. As an older, retired adult, I am very impressed at what I have read this far. The whole concept behind the side gig economy just really points towards entrepreneurship and a willingness to work beyond what others expectations might think you’re capable of.

It’s interesting – I’ve always thought of this gig economy world as a young person’s world, but I’ve found that a lot of older, retired folks take advantage of the gig economy as a way to generate some income and really for the fun factor of it. The more I think about it, the more it makes sense.

Impressive side hustling! I have chronic fatigue, so I don’t do side gigs as my main job and blogging take up all of my energies. But I do throw any blog income at my SEP-IRA now that I finally have one. It’s not $5 a day (alas), but it’s something, right?

Is it possible to do any of these side gig apps in London, or anywhere else overseas?

Yes, these gigs exist in London and overseas as well, but I have no idea how flexible they are over there. I know when I was in Paris over Christmas, I saw a lot of people biking around doing deliveries for Deliveroo and Uber Eats. I also saw people charging Lime scooters. No clue what the rules are over there though.

Check your 401k plan to see if they allow after-tax contributions. My plan allows me to withdraw after-tax 401k contributions without restrictions such as not being able to participate in the pre-tax portion of 401k plan. Convert the after-tax 401k contribution to a traditional IRA and convert that to a Roth using the back door methodology. This process is commonly known as a Mega Backdoor Roth IRA Conversion.

Social Security & Medicare contributions are capped. Depending on how much you make at you “full-time” job, you probably max out the contributions.

Do you have Health Reimbursement Accounts at work? If not, can’t you set one up as self-employed.

I love your blog and so many of your posts really resonate with me, particularly the ones that touch on the legal profession (fellow lawyer here). I’m so excited to follow along your self employment journey! Your side hustle reports really sold me on the ‘reverse latte factor’ before I even had a name for it, but the issue I’ve had is finding a way to minimize taxes on gig-economy type income. My marginal tax rate is really high at about 43% (love/hate relationship with living in California), maybe even higher (I think I need to double my social security and medicare taxes on 1099 income, right?), so earning an extra $10 in the gig economy is actually only pocketing me $5.70, which is kind of discouraging as sometimes my hourly earnings after taxes fall below minimum wage. I can’t do the Solo 401k because I already max out my 401k at work and I can’t do a SEP IRA because as I understand it, that would preclude me from being able to do the backdoor roth IRA due to the aggregation rule around IRAs. Do you have any other suggestions besides aggressive deductions?

Right, so that is exactly the problem with side hustle income because it’s essentially being taxed at your highest marginal tax rate. This is why it’s really important to take advantage of tax-advantaged accounts when you’re side hustling. Remember, you can still make an employer contribution to your solo 401k. There are calculators out there that show you how much you can contribute as an employer contribution. It should be about 20% of your profits, which can be significant depending on what you make.

The other thing is, remember that you can pay taxes using a credit card (I’ll write a post about that soon, because I need to pay some taxes soon). If you open up some cards for signup bonuses and then hit the minimum spends with credit cards, you are at least getting something back for your tax payments (an example is the Chase Ink Preferred currently gives you $1,000 worth of points – so if you make a tax payment of $5,000, you’re getting back $1,000 tax-free).

Finally, my last thought is simply that I don’t let the tax dog wag the income tail. If you got a raise at work, you wouldn’t decline it just because you’ll now owe more taxes on those last marginal dollars. It’s the same thing with side hustling.

My main problem with the latte factor is applying an annual return much less an annual return of 7%. That assume that you are taking your $5 saving and investing it into the stock market (market indice ETF?) daily. Since there is often (but not always) a commission when buying an ETF, it is inefficient to buy $5 of an ETF every day a week. More likely, you would aggregate the $5 in zero interest checking account until you got to $25 or for me $100. That’s 20 days.

However, that misses the nature of one’s day-to-day cash flow. In reality, the $5 I save from the latte is spent elsewhere or allows me to avoid moving money into my checking account (which is where most of my expenses are paid from). At best, the $5 would have a 0% annual return. $5 x 365 = $1,825 per year. Let’s look at the 30 year return. $1,825 x 30 years = $54,750 compared to $368,916.60 in your table. $54 K is still significant but the “savings” is reduced by nearly a factor 7. Of course, the price of lattes will go up so $54 K is understated but that also means $368,916.60 is also understated.

Realistically (for me) the rate of return is 2.1% max. When my checking account runs low, I pull from saving account earning 2.1%. When my checking account balance is high, I transfer some of it to the same saving account. However most months, I don’t make a transfer in either direction.

I would ask you to track your side gig money closely. Are you transferring it to an ETF ASAP or are you letting it sit in your checking account for awhile?

The interesting thing is with fintech today, you can actually buy ETFs every single day with no fee. So you can literally invest the $5 or $10 daily if you want. I wrote about how I do that with my guide to longer-term savings goals. I use WiseBanyan, which is 100% free, but you could also do the same thing with M1 Finance or SoFi Invest (both allow you to invest on daily or weekly basis with no fees and buy fractional shares of ETFs – and they’re robo advisors so they do all of this automatically).

In any event, even if you let it sit and invest it all as a lump sum once per year, it doesn’t change the long-term rate of return. I fund my Solo 401k once per year after I’ve done my taxes. Many people do the same with Roth IRAs. The daily investing factor doesn’t change the long term rate of return. What changes the rate of return really is how much you mess with it.

Investing $1,825 once per year vs. investing $5 daily – my guess is that the difference long term is going to be pretty negligible.