These days, student loans are pretty much a given for most young professionals. When I graduated law school back in 2013, I had a hugely negative net worth thanks to $87,000 worth of student loans that I had taken out. That doesn’t seem like all that much when you consider that the average law student today graduates with almost double that amount of debt. I think it’s a testament to just how normalized student loans have become when $87,000 can seem like nothing.

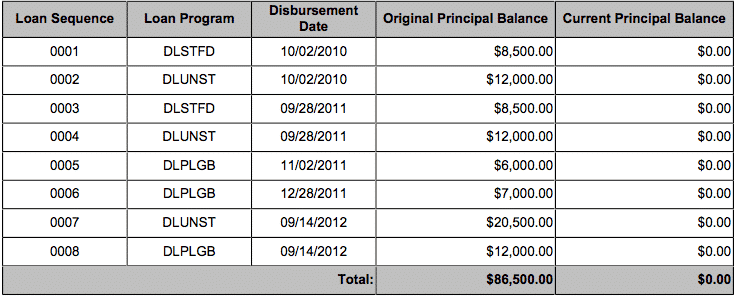

The thing that really stinks about student loans isn’t just the monthly payment. It’s the huge amount that you’re paying out each year towards interest. If you look at my own student loan history, you can see that I paid over $15,000 in interest over the life of the loan.

And that’s with me paying off the loan in just two years!

One of the reasons we’re paying so much in interest is because of the high-interest rates we’re given. Since anyone can get a student loan, the interest rates are higher than they should be for folks who are going into fields where they should hopefully make a decent income. Regular grad school loans clock in at a 6.8% interest rate these days. Grad plus loans come in at a whopping 7.9% interest rate.

Those kind of interest rates are no joke. Refinancing your loans takes into account your earning ability and gets you an interest rate that is more in line with your ability to repay your debt. In theory, most big law attorneys should be able to get their interest rate down to 5% or less.

My friend, the Big Law Investor, recently released a terrific student loan refinancing guide that I think anyone with student loans should check out. You can check out his student loan refinancing guide here. In that guide, he shares a ton of helpful information that’ll help anyone who’s trying to figure out how to refinance their student loans.

I thought I’d build upon what he wrote by talking a little bit about my own student loan refinancing experience. The great thing about the internet is that you can learn from people who’ve gone through this stuff before. And back in 2015, I went through a ton of student loan refinancing.

A Timeline Of My Student Loan Refinancing Experience

I’m a little bit weird. Instead of refinancing just once, I actually went ahead and refinanced my student loans three times with each of the big three student loan refinancing companies. In my mind, the big three are SoFi, CommonBond, and Earnest. There are definitely more out there, but I consider these three companies to be the big players in the student loan refinancing field.

I went through all of 2014 hustling to pay off my debt but doing so at 6.8% and 7.9% interest rates. At the time, I didn’t know that student loan refinancing was a thing. In retrospect, I basically wasted at least a few thousand dollars by not refinancing. By the end of 2014, I had paid off all of my 7.9% interest loans, leaving me with just the 6.8% interest ones remaining.

2015 was the first year I discovered that student loan refinancing was a thing. I waffled for a bit about what to do. Lawyers are naturally a conservative bunch, so it’s easy for us to get scared away from refinancing. Plus, the idea of refinancing sounds scary, these companies were new (at the time), and people on random forums kept mentioning that I would lose “federal protections” if I refinanced my student loans.

When you think about it, student loan refinancing is pretty simple in its most basic form. What you’re doing is taking out a loan with a new company and using that money to pay off your old loan. Once you do that, you have a new loan, except at a lower, more favorable interest rate.

Here’s a timeline detailing my student loan refinancing experience:

- February 2015: Applied for student loan refinancing with SoFi

- March 2015: SoFi student loan refinancing completed

- May 2015: Applied for student loan refinancing with CommonBond

- June 2015: CommonBond student loan refinancing completed; Paid all of SoFi student loan using CommonBond funds

- August 2015: Refinanced a portion of my student loans with Earnest. Paid off all of it in the same month.

- June 2016: Paid off CommonBond student loan.

Refinancing With SoFi

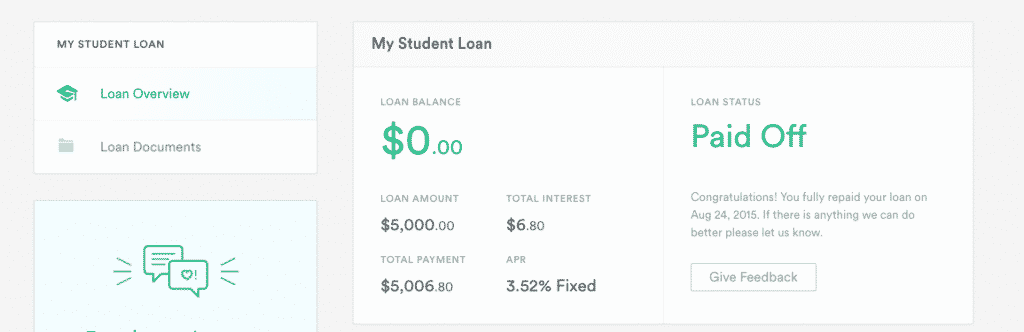

I first refinanced with SoFi, lowering my interest rate from 6.8% down to 4.3%. When I refinanced, I opted for a five-year, fixed rate term. I’m a risk adverse lawyer, so I never even thought about going for the variable rate term.

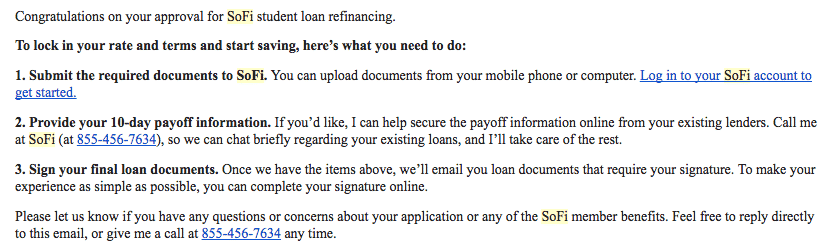

The process of getting approved was done entirely online. You basically enter in all the information about your job and what type of income you make. After I was pre-approved, I received the following email:

I then had to submit two paystubs in order to lock in the rate. I can’t really recall if I had to submit anything else. The main thing that companies like SoFi care about are that you have good credit and actually make enough money where you’ll be able to repay the loan.

Refinancing With CommonBond

Next on my refinancing journey was CommonBond. I’d been seeing their ads all over the place and figured I’d see what kind of rate I could get. The unique thing about CommonBond is their social mission. Much like Warby Parker or Toms shoes, CommonBond funds the education of a person in need for every loan that gets taken out with them. If you’re into companies with this kind of social mission, CommonBond is the way to go.

After noticing that they could offer me a variable rate of just 1.93%, I decided I’d be foolish not to take it. I opted to go with a five-year variable rate term. My rationale was that, by the time student loan interest rates rose, I’d be long done with my student loan. I ended up being right about that.

The process of setting up my refinance with CommonBond was largely the same as with SoFi. It took just a few weeks between my application and refinancing.

As a bonus, I also received a little bit of swag from CommonBond. And I used a referral link online, so I was able to get a little bit of cashback as well.

Refinancing With Earnest

Last on my refinancing stop was Earnest. I’d received an email offering me $100 if I refinanced my loan with them. I already had a super low-interest rate, but I sort of wanted that $100. And I wanted to see what the Earnest platform looked like.

Since I had a huge chunk of cash to use that month, I decided to refinance the minimum amount with Earnest – $5,000. It was probably a waste of time, but since I’m an experimenter, it let me see what the Earnest platform looks like.

Of all the big three companies, Earnest definitely has the best-looking payment platform. The other two companies outsource their payments to a third party servicing company, which generally means a crappier looking website.

Ultimately, I think refinancing with any of these companies is fine. I also don’t think there’s any problem with refinancing with multiple companies and snagging referral bonuses along the way.

But…if you can only choose one, SoFi might be the company you want to go with because of all the free stuff you can get (explained in more detail below).

Getting Free Food With SoFi

One thing that I haven’t seen a lot of people talk about is all the free stuff you can get when you refinance with these companies. There’s one particular company that really shines above all the others in the free stuff department – SoFi.

About four to six times per year, SoFi sponsors member events that are free to all SoFi members. You can check out a page of all their events here. They have a clever system to avoid people from signing up and then flaking out, though. When you sign up to attend an event, they charge you a fee, but they refund that fee when you actually go to the event.

In 2016, I attended four SoFi events, all of which were held at fancy restaurants that I’d probably never go to on my own. Some of the events are just regular happy hours, but with enough food that you can basically get a meal for yourself. And they’re always open bar. I go for the expensive cocktails so that I can get my money’s worth. Any drink with an egg in it is always good for me.

SoFi has also held three fancy dinners in my city that would easily cost $100 per person if you include the drinks and tip you’d have to leave.

The good thing is that SoFi allows you to bring a guest with you, so you don’t have to go by yourself. My wife and I basically turn it into a date night. And the other amazing thing is that you can still go to these events even AFTER you’ve paid off your student loans.

I haven’t had a SoFi loan since 2015 and I’m still attending every single SoFi event that comes up. Since 2015, I’d estimate that my wife and I have probably snagged $1,000 worth of food and drink between the two of us.

That number is now probably closer to $3,000 worth of free food and drink since I also won a SoFi contest that allowed me to fly to New York for free (check out my recap of my SoFi trip here).

Just a tip though – these SoFi events fill up fast, so you’ve got to be ready and sign up for them as soon as you see them.

Things To Remember If You’re Going To Refinance

- It’s A Hard Credit Pull. If you’re just checking for a potential interest rate, that’ll be a soft pull that has no effect on your credit. The hard pull comes into play once you actually pull the trigger and submit an application to refinance your loans. For most people, this won’t matter too much. A couple of hard credit pulls won’t really mess with your credit very much and they only affect your credit score for a year. Still, worth thinking about if that matters to you.

- Remember To Pay Off Your Old Loan. Student loans accrue interest daily. As a result, it’s sort of hard to figure out exactly how much you need to borrow for your refinance. Remember that when you refinance your loan, you’re basically taking out a new loan and paying off your old loan with that new money. Every time I refinanced my student loans, I was always left with a few bucks outstanding on my own loan. Just make sure to pay that off so that your old account is actually down to zero.

- Don’t Keep Extending Out The Life Of Your Loan. A lot of people only look at the monthly payment. You could definitely keep refinancing your loans and make your monthly payment smaller and smaller. But that’s sort of missing the point. Student loans suck. Instead of extending out the life of your loan, just use the lower rate to make more of a dent on that principle.

- Be Careful If You’re Going For Any Sort Of Loan Forgiveness. If you’re going for some sort of loan forgiveness program, the answer is pretty simple. Don’t refinance your debt. If you’re a doctor with a ton of debt and doing a long residency, you may want to keep your federal student loans and go for public service loan forgiveness. For most other professions, public service loan forgiveness probably isn’t worth it. Admittedly, I haven’t done the math, but it seems like most lawyers would come out ahead by just sucking it up in big law for a few years and crushing the debt.

- Federal Protections Are Probably Overrated. One of the most common arguments I hear to not refinance your student loans is that you want to keep those “federal protections.” I suppose it’s true that, if something happens to you, federal loans will allow you to go into forbearance or deferment for a while. The thing is, since I think most people should pay off their debt quickly, you’re basically paying extra for something you might not really need. In addition, these student loan refinancing companies also offer benefits if something like a job loss were to happen. SoFi, for example, will suspend your payments for 3 months and help you find a new job if you lose your job through no fault of your own. For most people, that’s probably plenty of cushion.

- It Costs Nothing To Refinance. I think this is something that really confuses a lot of people. Refinancing a home mortgage costs money, so most people assume that it must cost money to refinance a student loan. This is what’s great about refinancing. It’s totally, 100% free to refinance your student loans. You don’t pay a cent to refinance your student loan to a lower rate.

What Should You Do If You’re Looking To Refinance Your Student Loans?

The way I see it, you have two options when it comes to refinancing your student loans.

Your first option is to do like I did and pick and choose your way through each individual student loan company. Each one has its benefits:

- Refinance with SoFi and you’ll receive a $100 signup bonus and get access to all of SoFi’s awesome member events (free food and drinks galore).

- Refinance with CommonBond if you’re looking for a student loan refinancing company with a noble social mission.

- Refinance with Earnest and you’ll receive a $200 signup bonus and have an amazing student loan repayment interface.

I think any of these companies will do the trick, although I’m partial to SoFi simply because of all the side benefits I’ve received from refinancing with them.

Your second option is to use a company that’s basically a search engine for student loan refinancing companies. The way these companies work is pretty simple. They’re basically like the Kayak or Priceline of student loan refinancing companies – you give them your info and then they show you all the rates from every student loan refinancing company. It’s like when you book your flight using Kayak, instead of booking directly through United, Delta, or whatever airline you’re actually flying with.

In this area, I recommend using Credible. If you use Credible, you’ll be able to see your interest rates for almost every student loan company out there. Even better, Credible will give you $200 if you refinance your student loans using the below link.

- Search for and refinance your student loans using Credible and you’ll receive a $200 signup bonus.

For sure, if you’ve got a good income and aren’t planning to go for any sort of student loan forgiveness program, then you NEED to refinance your student loans – it’s a no-brainer. Hopefully, my experience with refinancing my student loans can help you out along the way.

This post may contain affiliate links.

More Recommended Ebike/Scooters

Check out these other ebikes and scooters I've reviewed:

- Urban Arrow Ebike – Last year, I made one of the largest purchases I’ve ever made – I bought a $9,000 electric cargo bike from Urban Arrow. In my Urban Arrow review, I will discuss what it is and why I decided to buy this bike, as well as discuss how impactful a bike like this can be on your journey to financial independence.

- Troxus Explorer Step-Thru Ebike – The Troxus Explorer Step-Thru is a fat-tire ebike that I’ve had the pleasure of riding for a while now. It has amazing power, great looks, and awesome range. If you’re looking for a great fat-tire ebike that offers a lot for the price, the Troxus Explorer Step-Thru is definitely one for you to consider. Check out my Troxus Explorer Step-Thru Review.

- Hovsco HovBeta Ebike – The HovBeta is a folding ebike with great specs and a lot of interesting features, and importantly, it’s sold at a good price point. I’ve had a blast commuting with it and using it to do deliveries with DoorDash, Uber Eats, and Grubhub. Check out my Hovsco HovBeta Ebike Review.

- Vanpowers Manidae Ebike – The Vanpowers Manidae is a fat tire ebike that I’ve been riding as my primary winter commuting bike and have also been using it to do food delivery with apps like DoorDash, Uber Eats, and Grubhub. After clocking in a decent number of miles with this ebike, I wanted to write a post sharing what my experience with the Vanpowers Manidae ebike has been like. Check out my Vanpowers Manidae Review.

- Sohamo S3 Step-Thru Folding EBike Review – A Great Value Folding Ebike – The Sohamo S3 Step-Thru Folding Ebike is an entry-level folding ebike that offers a lot of value for the price point. I’ve been riding the Sohamo S3 for a while now, putting the bike through its paces, and I have to say, this bike has exceeded all of my expectations. Check out my Sohamo Review.

- KBO Flip Ebike – The KBO Flip is an excellent bike. I’ve had a great time riding it and think it’s a versatile bike that can be used for a lot of purposes and can fit a variety of lifestyles. It’s worked out great for me as a general commuter bike and as a food delivery bike. Check out my KBO Flip Review.

- Hiboy P7 Commuter Ebike – The Hiboy P7 is an excellent electric commuter bike that’s offered at an affordable price point. The range and speed of this bike are both very good, so you won’t have any trouble getting anywhere you need to go with it. As a food delivery vehicle, this is also good – with how much range it offers, you’ll be able to work all day on a single charge. Check out my Hiboy P7 Commuter Electric Bike Review.

- Himiway Escape Ebike – The Himiway Escape is an interesting bike for anyone looking for a moped-style ebike. If you’re a gig economy worker, the Himiway Escape is particularly interesting and it’s possible to think of it as an investment, especially if you can opt to do deliveries with the Himiway versus using a car. It’s not cheap, but you can definitely make your money back when you compare the mileage you’ll put on your car versus using an ebike. Check out my Himiway Escape Bike Review.

- Espin Sport Ebike – The Espin Sport is a good ebike for someone who is looking for an ebike that feels and rides more like a regular bike. There are many ebikes that are really only bikes in name. In reality, they’re basically electric mopeds. The Espin Sport, by contrast, is a bike you could probably ride without the battery and you’d feel like you’re just riding a regular bike. Check out my Espin Sport Review.

- Varla Eagle One Scooter – The Varla Eagle One is an excellent scooter that can make sense for a lot of people. It can work as a primary mode of transportation. You can use it to work on gig economy apps like DoorDash, Uber Eats, and Grubhub. And it can also be a recreational vehicle if you’d prefer to use it for that. Check out my Varla Eagle One Review.

- Varla Falcon Scooter – The Varla Falcon is an excellent scooter that offers a good amount of power at a lower price point compared to more powerful scooters. It’s not exactly an entry-level scooter, nor is it a high-powered scooter. I think it fits somewhere in-between those two categories – an intermediate scooter if I had to give it a category. Check out my Varla Falcon Review.

- Hiboy S2 Scooter – The Hiboy S2 is an excellent entry-level commuter scooter that's perfect for someone looking to save some money in transportation costs and improve their commute. Check out my Hiboy S2 Review.

- Hiboy S2R Scooter – The Hiboy S2R is one of the more interesting electric scooters I’ve been able to test out. It’s not a high-powered scooter, but for an everyday transport option, it’s very useful, especially given some of the unique features that it has. Indeed, for the price, the Hiboy S2R might be the best value scooter I’ve used. Check out my Hiboy S2R Review.

- Fucare H3 Scooter – The Fucare H3 is a fun scooter and I’ve enjoyed testing it out. For a daily commuter or quick trips or errands, the Fucare H3 is probably the scooter I’ll use. It’s portable and easy to maneuver, so it’s just easier to take on the road when I need it. Check out my Fucare H3 Scooter Review.

More Recommended Investing App Bonuses

For additional investing app bonuses, be sure to check out the ones below:

- M1 Finance ($75) – This is a great robo-advisor that has no fees and allows you to create a customized portfolio based on your risk tolerance. You also get $75 for opening an account. Check out my M1 Finance Referral Bonus – Step-By-Step Guide.

- SoFi Invest ($25) – SoFi Invest is an easy brokerage account bonus that you can earn with just a few minutes of work. Use my SoFi Invest referral link, fund your SoFi Invest brokerage account with just $10 and you’ll get $25 of free stock. I also have a step-by-step guide for the SoFi Invest referral bonus.

- Robinhood (1 free stock) – Robinhood gives you a free stock valued between $2.50-$225 if you open an account using my referral link.

- Public (1 free stock) - Public gives you a free stock valued between $3-$70 if you open an account using my referral link.

More Recommended Bank Account Bonuses

If you’re looking for more easy bank bonuses, check out the below options. These bonuses are all easy to earn and have no fees or minimum balance requirements to worry about.

- Ally Bank ($100) – Of all the banks out there, Ally is, without a doubt, my favorite. At the moment, Ally is offering $100 to customers who open an eligible Ally account and meet the requirements. Here are the step-by-step directions to earn your Ally Bank referral bonus.

- Chime ($100) - Chime is a free bank account that offers a referral bonus if you use a referral link and complete a direct deposit of $200 or more. In practice, any ACH transfer into this account triggers the bonus. This bonus is easy to earn and posts instantly, so you’ll know if you met the requirements as soon as you move money into the account. I wrote a step-by-step guide on how to earn your Chime referral bonus that I recommend you check out.

- US Bank Business ($400/$1200) – This is a fairly easy bank bonus to earn, since there are no direct deposit requirements. In addition, you can open the Silver Business Checking account, which comes with no monthly fees. Check out how to earn this big bonus here.

- Current ($50) – Current is a free fintech bank that’s offering new users a $50 referral bonus after signing up for an account using a referral link. Current is an easy bonus to earn and also gives you access to three savings accounts that pay you 4% interest on up to $2,000. That means you can put away up to $6,000 earning 4% interest. That’s very good and makes Current an account I recommend to everyone. Check out my step-by-step guide on how to earn your Current Bank bonus.

- Novo Bank ($40) - Novo bank is a free business checking account that’s currently offering a $40 bonus if you open a Novo business checking account using a referral link. In addition to being a good bank bonus, Novo is also a good business checking account. It has no monthly fees or minimum balance requirements and operates a good app and website. Indeed, it’s the business checking account I currently use for this blog. Check out my post on how to easily open a Novo account.

- Varo ($25) – Varo is a free fintech banking app similar to Chime or Current. It’s currently offering a $25 bonus to new users that open a new Varo account with a referral link. The bonus for this bank is very easy to meet, all you need to do is spend $20 within 30 days of opening your Varo account. Check out my step-by-step guide to learn how to earn this bonus.

Kevin is an attorney and the blogger behind Financial Panther, a blog about personal finance, travel hacking, and side hustling using the gig economy. He paid off $87,000 worth of student loans in just 2.5 years by choosing not to live like a big shot lawyer.

Kevin is passionate about earning money using the gig economy and you can see all the ways he makes extra income every month in his side hustle reports.

Kevin is also big on using the latest fintech apps to improve his finances. Some of Kevin's favorite fintech apps include:

- SoFi Money. A really good checking account with absolutely no fees. You'll get a $25 referral bonus if you open a SoFi Money account with a referral link, and an additional $300 if you complete a direct deposit.

- 5% Savings Accounts. I'm currently getting 5.24% interest on my savings through a company called Raisin. Opening a Raisin account takes minutes to complete, it's free, and all of your funds are FDIC-insured. I explain how it works, why I'm now using it to store my emergency fund and any other cash savings I have, and why I recommend everyone check it out in this review.

- US Bank Business. US Bank is currently offering new business customers a $400/$1200 signup bonus after opening a new account and meeting certain requirements.

- M1 Finance. This is a great robo-advisor that has no fees and allows you to create a customized portfolio based on your risk tolerance. You also get $75 for opening an account.

- Empower. One of best free apps you can use to monitor your portfolio and track your net worth. This is one of the apps I use to track my financial accounts.

Feel free to send Kevin a message here.

How much of a difference between a fixed and variable rate do you think makes a variable rate worth it? I’ve been getting quotes and the difference currently is .31%, however at least for the time being it sounds like the Feds are likely to drop rates or stay flat for the next 2 years so I’m leaning towards variable as well.

I’m lucky that I consolidated most of my federal loans at a time when the interest rate was ultra low. Refinancing is a great tool for those with a lot of student loan debt with higher rates. Is there anything to stop someone from refinancing just to get the bonuses? Kinda like how you can open and close bank accounts to get their bonuses?!

There’s nothing stopping you other than not wanting to get hard credit inquiries. I refinanced a bunch of times and snagged a bonus every single time! With Earnest, they actually lost money on me because I paid off the loan in one month just to snag that bonus.

Very nice write up, FP! I never heard of Common Bond, which is a bummer with that slamming low rate you received!! I could have saved myself quite a bit with that interest rate – water under the bridge now…

Yeah, that rate was crazy low!

Wow! I didn’t realize that SoFi had events to attend, and that you’d still be invited after repaying all of your loans!

I, unfortunately, wasn’t too savvy at the time of debt either, so I just repaid like there was no tomorrow. I did eventually pay it off. I’m not sure how much extra interest I paid in the process.

Yeah, these events are where it’s at. Another side benefit that a lot of people either don’t know about or don’t talk about very much.

You should totally pull all your student loan info and find out how much you ended up paying all together. It’s interesting to see.