When my brother first started making a decent amount of money, I told him that the smartest thing he could do was to save as much of his income as he could, live modestly, and invest his money in low-cost, passively managed index funds. I assured him that if he did all of this, I could pretty much guarantee that he’d be in better shape than the vast majority of the population.

Naturally, being my younger brother, he ignored everything I said and instead did things his own way. He ended up finding a financial advisor from a big-name company that many of us have probably heard of (and most likely, many of you have a low view of this company). This financial advisor then went ahead and invested all of my brother’s hard-earned money for him.

For years, I’ve been telling my brother that he needs to drop that financial advisor and move his money over to a good company like Vanguard, or even a robo-advisor like M1 Finance, Betterment, or Wealthfront. Even though I knew nothing about who his financial advisor was, I knew enough about the company that he worked for that I could pretty much guess that he was being scammed.

And sure enough, the other day, I actually took a look at my brother’s investments and was disgusted at what I saw. While his tax-advantaged accounts were decently invested (although invested in a much more complicated manner than needed), the rest of his portfolio was a disaster. I saw actively managed funds with 1% or more expense ratios and a 5.75% front-end load fee. He had a huge percentage of his investments in individual stocks that charged a 2% commission per transaction. And he had money invested in dozens of ETFs that seemed to make things much more complicated than they needed to be.

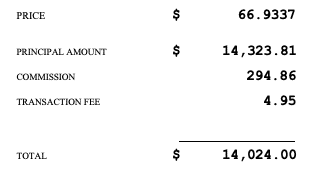

To get an idea of what was going on with my brother’s investments, take a look at this ridiculous commission he paid to buy $14,000 of some individual stock. And that was just for one stock. Over the course of the last several years, he’s paid thousands of dollars in commissions to his financial advisor (or his financial advisor’s company). And this same fee applies to buying and selling his ETFs as well.

This post isn’t meant to rag on people like my brother. Really, I think it’s just an interesting, real-life case study in how someone like my brother, a smart guy who isn’t all that stupid with his money, can end up giving away a lot of their money in unnecessary fees and expenses. This happens because a lot of people don’t really know how money and investing actually work.

Your Financial Advisor Isn’t Free

One of the things my brother was convinced of was that his financial advisor didn’t charge him anything. Even when I explained to him that his financial advisor obviously doesn’t work for free, he remained convinced that his advisor wasn’t getting paid by him.

I can see though why my brother thought his financial advisor was free. The problem with a lot of things in the financial industry is that fees are pretty mysterious. In other industries, you get a bill, so you know what you paid. But in the financial advisory world, you’ve already given your money to them. It’s easy enough for them to just take little bits of it off the top without you even noticing.

And this stuff can be complicated. Even now, I have no idea if his financial advisor charges him an asset under management (AUM) fee. I assume he must pay something, but I honestly can’t figure it out. My brother’s investing account doesn’t seem to show AUM fees being charged, so maybe he’s not paying anything. It doesn’t help though that the fee structure document I found was literally over 50 pages long. Maybe he’s not paying anything for his financial advisor to manage his account – but if that’s the case, then why have this huge fees document?

My digging did reveal the massive commissions he was paying to invest his own money. A 5.75% front-end load fee is ridiculous in today’s world when you can literally buy pretty much any good fund for free. I honestly can’t understand what benefit paying a 5.75% frontload provides other than that you could probably get away with it easier before we had the internet.

A 1% expense ratio is also nuts when you have funds charging 0.05% or less. To justify that expense, these funds would have to outperform by over 1% every year for decades. Thinking logically, we know that’s unlikely.

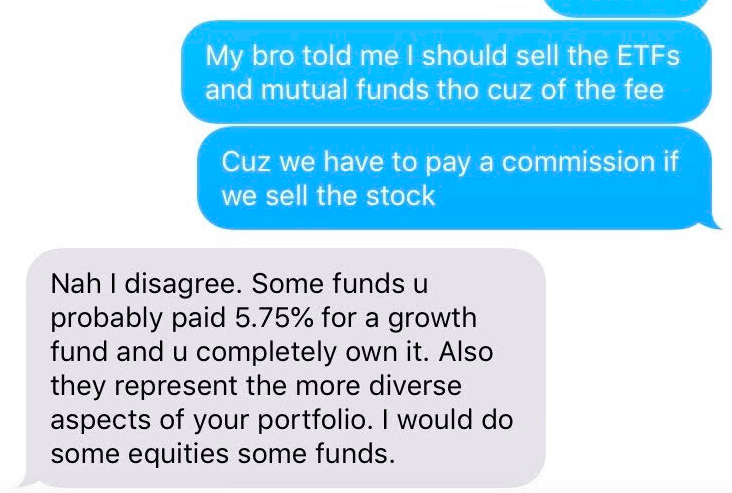

And perhaps what amazed me the most was the 2% commissions my brother was paying to buy and sell his individual stocks and ETFs. I initially thought that this 2% commission applied to his individual stocks only, but it turns out he was paying 2% commissions to sell ETFs as well. And of course, when I looked at his account, what had just happened? His financial advisor had just sold all of his ETFs so that he could cash out on his “profit.” And now he was putting his money back to work, reinvesting it in other stocks and ETFs – and generating more commissions in the process.

Admittedly, I have a pretty low view of the whole financial advisory industry. And maybe it’s not warranted. But when I look at the stuff my brother is invested in, I can’t really understand how this is anything but a scam. Indeed, when my brother asked about the 5.75% front-end load fees that he’d been paying, he received this strange non-sequitur response from his advisor.

I don’t even know what that means. All I do know is that it’s pretty clear his financial advisor isn’t free. He’s paying him something – likely thousands of dollars each year in unnecessary fees. Over a lifetime, it could be hundreds of thousands or even millions of dollars in lost gains.

Your Financial Advisor Probably Isn’t Warren Buffett

Another rationale my brother has been using to stick with his financial advisor over my objections is that his guy knows what stocks to invest in. As my brother explains, his financial advisor told him to invest in Facebook, and look how much money he made on it!

The interesting thing is that my brother’s belief that his financial advisor knows how to pick stocks assumes one of two things. He either thinks his financial advisor is an elite stock picker on the level of Warren Buffet. Or he must assume that his guy is doing insider trading.

The latter is obviously illegal. The former…well, that begs the question. If someone were so good at picking stocks, why are they spending their days picking stocks for other people and not just picking stocks for themselves?

The truth is, your financial advisor most likely isn’t Warren Buffet. If they were, they wouldn’t be out there picking stocks for you. Logically, they’d be out there picking stocks for themselves. The internet has pretty much leveled out the field of information for everyone. Most likely, any financial advisor who’s picking stocks is just guessing or working off the same information that everyone else has.

You Don’t Need To Hit Home Runs

There’s this strange thing with money (or really with almost anything in life). Most of us think that success comes from hitting home runs – that if you want to succeed, you have to do it on one thing.

But that’s not how it works. Like the story of the tortoise and the hare, you win when you do constant small actions, taken over a long period of time. You only have to do a few things decently right. And if you do just that, even without any home runs, you’ll get to where you need to be.

I’m not saying a financial advisor doesn’t make sense ever. I personally don’t see a lot of reason I’d ever use one, but I’m unique in the fact that I literally write about money and find this stuff fun to learn. For someone like my brother who doesn’t have a lot of interest in learning how to do all of this money stuff, maybe a financial advisor does make sense. But when I see things like huge frontloads on expensive, actively managed funds, commissions to buy and sell, and unclear fee structures, my spidey sense immediately starts tingling.

We’ll see what my brother does. I think he’s starting to understand that his financial advisor isn’t free since I literally showed him what he paid him. He still doesn’t quite understand that stock picking is pretty much guesswork and that logically, his financial advisor probably isn’t any better than anyone else at picking stocks. We’ll see what happens – because right now, this seems like an expensive mess to me.

This post may contain affiliate links.

More Recommended Ebike/Scooters

Check out these other ebikes and scooters I've reviewed:

- Urban Arrow Ebike – Last year, I made one of the largest purchases I’ve ever made – I bought a $9,000 electric cargo bike from Urban Arrow. In my Urban Arrow review, I will discuss what it is and why I decided to buy this bike, as well as discuss how impactful a bike like this can be on your journey to financial independence.

- Troxus Explorer Step-Thru Ebike – The Troxus Explorer Step-Thru is a fat-tire ebike that I’ve had the pleasure of riding for a while now. It has amazing power, great looks, and awesome range. If you’re looking for a great fat-tire ebike that offers a lot for the price, the Troxus Explorer Step-Thru is definitely one for you to consider. Check out my Troxus Explorer Step-Thru Review.

- Hovsco HovBeta Ebike – The HovBeta is a folding ebike with great specs and a lot of interesting features, and importantly, it’s sold at a good price point. I’ve had a blast commuting with it and using it to do deliveries with DoorDash, Uber Eats, and Grubhub. Check out my Hovsco HovBeta Ebike Review.

- Vanpowers Manidae Ebike – The Vanpowers Manidae is a fat tire ebike that I’ve been riding as my primary winter commuting bike and have also been using it to do food delivery with apps like DoorDash, Uber Eats, and Grubhub. After clocking in a decent number of miles with this ebike, I wanted to write a post sharing what my experience with the Vanpowers Manidae ebike has been like. Check out my Vanpowers Manidae Review.

- Sohamo S3 Step-Thru Folding EBike Review – A Great Value Folding Ebike – The Sohamo S3 Step-Thru Folding Ebike is an entry-level folding ebike that offers a lot of value for the price point. I’ve been riding the Sohamo S3 for a while now, putting the bike through its paces, and I have to say, this bike has exceeded all of my expectations. Check out my Sohamo Review.

- KBO Flip Ebike – The KBO Flip is an excellent bike. I’ve had a great time riding it and think it’s a versatile bike that can be used for a lot of purposes and can fit a variety of lifestyles. It’s worked out great for me as a general commuter bike and as a food delivery bike. Check out my KBO Flip Review.

- Hiboy P7 Commuter Ebike – The Hiboy P7 is an excellent electric commuter bike that’s offered at an affordable price point. The range and speed of this bike are both very good, so you won’t have any trouble getting anywhere you need to go with it. As a food delivery vehicle, this is also good – with how much range it offers, you’ll be able to work all day on a single charge. Check out my Hiboy P7 Commuter Electric Bike Review.

- Himiway Escape Ebike – The Himiway Escape is an interesting bike for anyone looking for a moped-style ebike. If you’re a gig economy worker, the Himiway Escape is particularly interesting and it’s possible to think of it as an investment, especially if you can opt to do deliveries with the Himiway versus using a car. It’s not cheap, but you can definitely make your money back when you compare the mileage you’ll put on your car versus using an ebike. Check out my Himiway Escape Bike Review.

- Espin Sport Ebike – The Espin Sport is a good ebike for someone who is looking for an ebike that feels and rides more like a regular bike. There are many ebikes that are really only bikes in name. In reality, they’re basically electric mopeds. The Espin Sport, by contrast, is a bike you could probably ride without the battery and you’d feel like you’re just riding a regular bike. Check out my Espin Sport Review.

- Varla Eagle One Scooter – The Varla Eagle One is an excellent scooter that can make sense for a lot of people. It can work as a primary mode of transportation. You can use it to work on gig economy apps like DoorDash, Uber Eats, and Grubhub. And it can also be a recreational vehicle if you’d prefer to use it for that. Check out my Varla Eagle One Review.

- Varla Falcon Scooter – The Varla Falcon is an excellent scooter that offers a good amount of power at a lower price point compared to more powerful scooters. It’s not exactly an entry-level scooter, nor is it a high-powered scooter. I think it fits somewhere in-between those two categories – an intermediate scooter if I had to give it a category. Check out my Varla Falcon Review.

- Hiboy S2 Scooter – The Hiboy S2 is an excellent entry-level commuter scooter that's perfect for someone looking to save some money in transportation costs and improve their commute. Check out my Hiboy S2 Review.

- Hiboy S2R Scooter – The Hiboy S2R is one of the more interesting electric scooters I’ve been able to test out. It’s not a high-powered scooter, but for an everyday transport option, it’s very useful, especially given some of the unique features that it has. Indeed, for the price, the Hiboy S2R might be the best value scooter I’ve used. Check out my Hiboy S2R Review.

- Fucare H3 Scooter – The Fucare H3 is a fun scooter and I’ve enjoyed testing it out. For a daily commuter or quick trips or errands, the Fucare H3 is probably the scooter I’ll use. It’s portable and easy to maneuver, so it’s just easier to take on the road when I need it. Check out my Fucare H3 Scooter Review.

More Recommended Investing App Bonuses

For additional investing app bonuses, be sure to check out the ones below:

- M1 Finance ($75) – This is a great robo-advisor that has no fees and allows you to create a customized portfolio based on your risk tolerance. You also get $75 for opening an account. Check out my M1 Finance Referral Bonus – Step-By-Step Guide.

- SoFi Invest ($25) – SoFi Invest is an easy brokerage account bonus that you can earn with just a few minutes of work. Use my SoFi Invest referral link, fund your SoFi Invest brokerage account with just $10 and you’ll get $25 of free stock. I also have a step-by-step guide for the SoFi Invest referral bonus.

- Robinhood (1 free stock) – Robinhood gives you a free stock valued between $2.50-$225 if you open an account using my referral link.

- Public (1 free stock) - Public gives you a free stock valued between $3-$70 if you open an account using my referral link.

More Recommended Bank Account Bonuses

If you’re looking for more easy bank bonuses, check out the below options. These bonuses are all easy to earn and have no fees or minimum balance requirements to worry about.

- Ally Bank ($100) – Of all the banks out there, Ally is, without a doubt, my favorite. At the moment, Ally is offering $100 to customers who open an eligible Ally account and meet the requirements. Here are the step-by-step directions to earn your Ally Bank referral bonus.

- Chime ($100) - Chime is a free bank account that offers a referral bonus if you use a referral link and complete a direct deposit of $200 or more. In practice, any ACH transfer into this account triggers the bonus. This bonus is easy to earn and posts instantly, so you’ll know if you met the requirements as soon as you move money into the account. I wrote a step-by-step guide on how to earn your Chime referral bonus that I recommend you check out.

- US Bank Business ($400/$1200) – This is a fairly easy bank bonus to earn, since there are no direct deposit requirements. In addition, you can open the Silver Business Checking account, which comes with no monthly fees. Check out how to earn this big bonus here.

- Current ($50) – Current is a free fintech bank that’s offering new users a $50 referral bonus after signing up for an account using a referral link. Current is an easy bonus to earn and also gives you access to three savings accounts that pay you 4% interest on up to $2,000. That means you can put away up to $6,000 earning 4% interest. That’s very good and makes Current an account I recommend to everyone. Check out my step-by-step guide on how to earn your Current Bank bonus.

- Novo Bank ($40) - Novo bank is a free business checking account that’s currently offering a $40 bonus if you open a Novo business checking account using a referral link. In addition to being a good bank bonus, Novo is also a good business checking account. It has no monthly fees or minimum balance requirements and operates a good app and website. Indeed, it’s the business checking account I currently use for this blog. Check out my post on how to easily open a Novo account.

- Varo ($25) – Varo is a free fintech banking app similar to Chime or Current. It’s currently offering a $25 bonus to new users that open a new Varo account with a referral link. The bonus for this bank is very easy to meet, all you need to do is spend $20 within 30 days of opening your Varo account. Check out my step-by-step guide to learn how to earn this bonus.

Kevin is an attorney and the blogger behind Financial Panther, a blog about personal finance, travel hacking, and side hustling using the gig economy. He paid off $87,000 worth of student loans in just 2.5 years by choosing not to live like a big shot lawyer.

Kevin is passionate about earning money using the gig economy and you can see all the ways he makes extra income every month in his side hustle reports.

Kevin is also big on using the latest fintech apps to improve his finances. Some of Kevin's favorite fintech apps include:

- SoFi Money. A really good checking account with absolutely no fees. You'll get a $25 referral bonus if you open a SoFi Money account with a referral link, and an additional $300 if you complete a direct deposit.

- 5% Savings Accounts. I'm currently getting 5.24% interest on my savings through a company called Raisin. Opening a Raisin account takes minutes to complete, it's free, and all of your funds are FDIC-insured. I explain how it works, why I'm now using it to store my emergency fund and any other cash savings I have, and why I recommend everyone check it out in this review.

- US Bank Business. US Bank is currently offering new business customers a $400/$1200 signup bonus after opening a new account and meeting certain requirements.

- M1 Finance. This is a great robo-advisor that has no fees and allows you to create a customized portfolio based on your risk tolerance. You also get $75 for opening an account.

- Empower. One of best free apps you can use to monitor your portfolio and track your net worth. This is one of the apps I use to track my financial accounts.

Feel free to send Kevin a message here.

I just recently discovered your site and starting to dig around your posts. I have to say that I LOVE this one!

It’s really sad the our education system doesn’t focus on teaching financial management as a requirement to get a high school diploma/GED. Self financial management can be done by anyone who’s willing to do a little research and read some books and blogs. We live in a society obsessed with money, yet has no knowledge on how to manage it.

You nailed it with a lot of your information. More people need to know the absurd amount of money many financial professionals are getting paid to manage someone’s finances. Many times an advisor is not even managing an investor’s money they are just selling products.

The truth is over 80% of the financial advisors working in the industry do not beat market averages. This is the same result for even most actual mutual fund managers. For a lot of people, they would be better off just investing in an index fund.

I worked for over a decade for a large brokerage firm and assisted 100’s if not 1000’s of advisors in moving from their current employer to the brokerage firm I was employed with. Most of them are very good salespeople. I think what most investors fail to realize is that it does not take a financial genius to manage someone’s money. Most financial professionals are good relationship builders and a lot of them truly do not know much about investing.

When it comes to the insane commissions and paychecks an advisor makes, I think what one advisor once told me put it best. He said being a financial advisor is the best part-time job for full-time pay that a person could have. This is the reality for many successful financial professionals. Once they build a good book of business and accumulate enough assets under them, things start to almost run by itself. Many advisors in this scenario charge a fee for an account they manage and have one or two reviews a year with a client. A client that has 500k to invest might get charged a 1% fee paid out quarterly. The advisor would pocket $5000 for the equivalent of spending a few hours per year with a client.

Although most people do not need an advisor, some more affluent investors can benefit. This is if the advisor can offer additional services like tax planning and not just selling investments. Wealthy people have a real need for more diversification and ensuring they pay the least amount in taxes.

Thanks for a great article.

That message from the advisor… I had to read it three times and I’m bamboozled. Yikes. It’s too bad your bro won’t let you help him out getting the account set up. I would pull my hair out if my sister was doing this!

We’re working on it. He’s afraid of hurting his financial advisor’s feelings.

Just tell the advisor he needs the money back for an emergency vasectomy.

The “hurt feelings” gimmick seems to be a common ploy among financial advisors.

lol, yep.

It would not surprise me if your brother is getting churned meaning his advisor is buying and selling stock to get the commission.

There are a ton of articles on the advantages of passive, low cost ETFs vs. actively managed funds with high expense ratios. Why don’t you send those to your brother? A lot of times, if family says something, they don’t believe it. If a third party tells them the same thing, they believe it.

For the tax advantaged account, is it a 401k? 401k have limited holding options which makes them somewhat immune to churning and commission based fees. Look up a company called Blooom.com (three o’s) . They have a flat fee of $120 per year or $10 per month to manage your 401k. Just show him the savings from Blooom vs. what his current financial advisor is charging him.

Oh, I have no doubt the dude churns for his benefit – he’s gotta get paid too after all.

Trust me, I’ve harped on this for years now. He’s not listening to anything I’m sending his way.

His tax-advantaged is a SEP-IRA. He’s self-employed and makes a lot, so is able to max out his SEP every year. Of course, with his income, he shouldn’t be using a SEP anyway because the way he has things set up right now means he can’t do a backdoor Roth. I’m working on getting him to move to a Solo 401k.

Are you telling him or showing him? Are you showing him articles WSJ, Kiplingers, Forbes, etc? NY Times did an article on churning.

https://www.nytimes.com/2018/08/24/business/brokers-excessive-trading-retirement.html

I notice your brother’s text mentioned your advice instead of just stating the facts. Even your brother’s side of the text is confusing. He says you told him to sell because you have to pay a commission to sell. Why sell? Just transfer the holding to another brokerage with lower commissions. 99 cents per trader or whatever.

Whenever I bump up against a stubborn relative, I say “You are the stupidest human on the face of that planet. I’m not wasting my breath on you anymore.” It’s not very effective but it ends the arguments.

I’ve told and showed him. But remember, we take a lot of the knowledge we have for granted. Just the words ETFs, mutual funds, and lots of other investing things we say assume a lot of knowledge. I’m working on hand holding him through the process.

Does it rhyme with Bells Largo?

I can’t say…don’t want to risk getting sued!