Editors Note: Some offers mentioned below are no longer available. View the current offers here.

I’ve always been wary when it comes to credit cards. Even though I’ve never been shy about trying out new fintech apps or opening up new bank accounts, for some reason, credit cards have always scared me. Maybe it’s the fact that a credit card goes on your credit report. Signing up for a new card just seems so … permanent.

My fear of opening up new credit cards probably comes from the fact that my history with credit cards isn’t very robust. I got my first card back in 2006 during my sophomore year of college – a Citi mtvU Visa Card which gave me extra points when I used it at bars and restaurants. The card seemed pretty good and it served as my daily use card throughout my 20s. In 2012, Citi changed the card over to a Citi Forward Card, which was the card that I was using all the way through the beginning of this year. The only other card I’ve gotten during that time is a Target Red Card that I accidentally got when I was actually trying to get the Target Debit Card.

Because of this fear of credit cards, I’ve pretty much missed out on the whole travel hacking craze. If this is a new concept to you, basically, a lot of credit card companies offer lucrative signup bonuses if you open up certain credit cards. People who are knowledgeable about travel hacking can pretty much fly around the world for free just by strategically opening up new cards every year. That’s often thousands of dollars a year that people can make just by opening up new credit cards. Headlines like the one below aren’t that uncommon to see.

For the last 10 years, I’ve adamantly refused to do any travel hacking. Looking back, it seems a bit strange that I was so afraid to get into this world. I make money in a ton of weird ways. Travel hacking seems like it would be a natural fit, so why would I be so against it?

A part of it has to do with a simple lack of knowledge. I just didn’t know that travel hacking was a thing until recently. The other part was fear. Travel hacking seemed confusing to me. For example:

- It wasn’t quite clear to me how new cards affected my credit score. Wouldn’t my credit score drop if I kept opening up new cards?

- There are a ton of cards out there. Which ones was I supposed to open?

- How am I supposed to meet the minimum spend on all of these cards?

- What about those annual fees?

- What do I do with the card once I’m done with it?

- And seriously, won’t opening up all of these new cards wreck my credit score?

Even though a lot of people make travel hacking seem really simple, it’s actually not that straightforward. There’s a lot that you need to know if you want to do it right.

The great thing about the internet is that you can become an expert in pretty much anything if you’re willing to take the time to learn how to do it. Before this year, I knew absolutely nothing about travel hacking. Today, I’d like to think that I’ve graduated to something beyond amateur travel hacker status.

I’m planning to talk a little bit more about what I’ve learned about travel hacking as I continue to get into this world, but for now, here’s the story of my first foray into travel hacking. My goal here is to help you figure out travel hacking, not from the point of view of some super travel hacker expert, but from the point of view of a regular dude just trying to figure out how all of this works.

And take it from this amateur travel hacker – you can become an expert travel hacker too if you’re willing to put in the work.

Missing Out On A Lot Of Points

For the most part, travel hacking is a bit of a niche area, but sometimes, cards get so big that even regular people get into the travel hacking game. In late 2016, Chase offered 100,000 ultimate rewards points for folks that opened up a Chase Sapphire Reserve card. Even my less savvy friends jumped on this offer – most likely because it was advertised all over Facebook by big bloggers. My friends urged me to sign up for it too and I refused. The whole thing seemed too weird to me. I didn’t understand what the whole travel hacking thing was about and didn’t want to risk messing with my credit score.

In retrospect, I should have signed up for the card. Now, I’m kicking myself! But oh well. Live and learn.

My biggest missed opportunity was definitely in the form of my wedding. I’ve learned a lot from planning a wedding, and one thing I know is that weddings are expensive! If you’re going to be paying for all of that stuff, it makes sense to get a little bit of return on your spend. With an average wedding costing in the neighborhood of $30,000, many people could open up 7 or more new credit cards and get thousands of dollars back in the form of hotels and travel.

My wife’s engagement ring was another missed opportunity. I bought it at the beginning of 2016 and threw the whole cost of it on my Citi Forward Card, which I then promptly paid in full. Sure, my card gave me 1% back on my purchase. But had I taken advantage of credit card signup offers, I probably could’ve easily gotten back $1,000 or $2,000 worth of travel.

So if you’re getting married anytime soon, you need to be signing up for multiple credit cards! Don’t let all that spent money go to waste!

My First Experience With Travel Hacking

In February of 2017, I decided to take the plunge and try my hand at travel hacking my first flights. Since I was new to this world, I had a few things I was worried about. First, I wanted something pretty simple and easy to figure out. Second, I didn’t want to pay any annual fees. (I’ve since learned that annual fees shouldn’t be a dealbreaker).

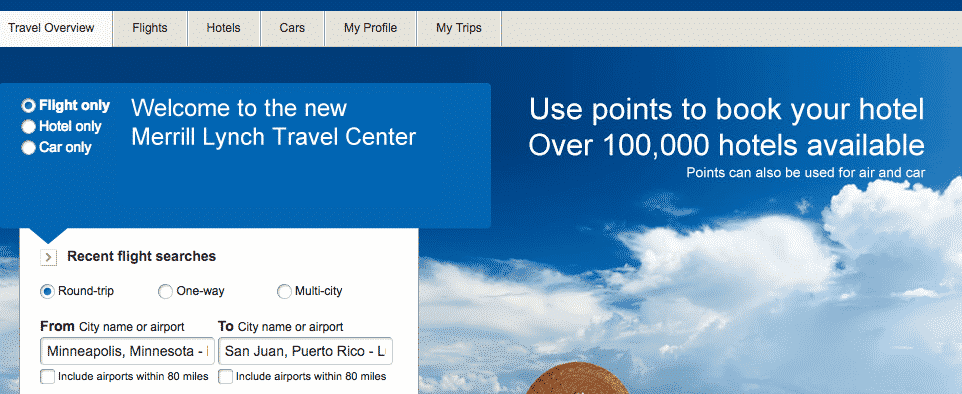

The card that hit all of these points was the Merrill+ Visa Signature Credit Card. At the time, that card offered 50,000 bonus points if you spent $3,000 within the first three months, which translated to about $1,000 worth of plane tickets. And the best part was that the card had no annual fee, making it seem low risk in my eyes. Since I already had to pay for a bunch of wedding expenses, the card seemed like a no-brainer to me.

In terms of redeeming the points, the process was super easy. I spent the $3,000 pretty much immediately by paying a couple of wedding bills with the card. A few days later, the 50,000 bonus points appeared in my account – even before my statement period had ended.

Using the points was a pretty simple process. One thing to note is that the Merrill Lynch travel center has a few quirky rules. Basically, any flight that’s $500 or less costs a flat 25,000 points. My goal was to get as close to a $500 ticket as possib le. Since my wife and I were looking to go to Puerto Rico for our honeymoon, this worked out perfectly for us. Flights to Puerto Rico from Minneapolis clocked in at about $497 roundtrip. We basically were getting the maximum return on our points.

A few clicks of the mouse and that was it. Our honeymoon flights were booked -totally free! It seemed like the perfect beginner card for a new travel hacker like me. And since there was no annual fee, I didn’t have to worry about what I was going to do with the card later.

One thing to note – I didn’t optimize my travel hacking strategy to the fullest. Most people would say that if you’re starting out as a brand new travel hacker, your first five cards should ideally be from Chase. The reason for this has to do with a special rule known as the 5/24 rule. Basically, Chase won’t let you open up new cards if you’ve opened up 5 or more credit cards from any company in the past 24 months. Since Chase is well known for having some of the best signup bonuses, it’s often recommended to go for Chase Cards first before going for other cards. If I could go back in time, I’d probably have done that instead – but that’s a lesson for another day.

Things To Know If You’re Skeptical About Travel Hacking

I think most people who are responsible with their credit cards stand to benefit from travel hacking. Even just a few cards per year would lead to thousands of dollars in free travel.

Here are some things that I’ve learned as I’ve started getting into the world of travel hacking:

1. Meeting Minimum Spends

The key with any new card is meeting the minimum spend requirements. Before you open up a new card, make sure that the minimum spend is something that you can realistically hit.

Of course, you don’t want to be opening up new cards only to spend more than you normally do. That’s why weddings are a great spot to really go all out with travel hacking. Your engagement ring or wedding dress is going to be expensive no matter how you slice it. And paying for everything else that comes with a wedding will be expensive too. You might as well get something in return for spending all of that money.

Most of the time, it’s thousands of dollars you’re getting back in travel and hotels. Don’t miss out on it!

2. Don’t Fear The Annual Fee

Annual fees have always seemed crazy to me. Why would I pay for the benefit of spending money on a credit card?

The key with fees is to remember that you should be getting more back than what the card costs. If you’re getting back $500 or $1,000 in travel and paying $95 for the card, it’s like you’re paying $95 to get $500 or $1,000. That’s a good deal for you.

3. Travel Hacking Won’t Mess Up Your Credit Score

I always figured that travel hacking would screw up my credit score a ton. Turns out that opening up new cards might lead to minor dips, but only in the short term. Even though I’ve opened up 4 new credit cards in the past 5 months, my credit score still hovers at around 800.

Sure, opening up new cards will lower the average age of your credit. But opening up new cards also leads to more available credit, which means a lower credit utilization rate (a lower utilization rate is good for your credit score). It sort of balances out over the long run.

Closing cards was the one thing I was worried about. But I realized one thing:

4. You Don’t Necessarily Have To Cancel Annual Fee Cards

I used to think that if I got a card with an annual fee, my only option was to either keep the card or close it. However, many cards also let you downgrade them to no-annual-fee cards, which means you don’t have to worry about the decision to keep or close the card if you no longer want it.

Travel Hacking Doesn’t Have To Be Scary

Travel hacking can be intimidating if you’re new to it. I know it was for me and it’s the reason why I held off on doing it for so long. But it doesn’t have to be scary. If you know what you’re doing, you’re going to come out ahead – you just need to take a little bit of time to understand how it all works.

I’ve had a ton of fun figuring out this whole travel hacking thing and I’m going to be sharing what I’ve learned with all of you as I figure it out. It’s pretty addictive figuring out ways to optimize your spend in order to get free flights and I can definitely see why people spend so much time thinking about it.

Related: If you like travel hacking, you’ll definitely want to think about optimizing the interest rates on your emergency fund with 5% interest savings accounts. I let fear hold me back from getting into travel hacking and it’s something I regret. Don’t let fear hold you back from maximizing the return on your cash.

This post may contain affiliate links.

More Recommended Ebike/Scooters

Check out these other ebikes and scooters I've reviewed:

- Urban Arrow Ebike – Last year, I made one of the largest purchases I’ve ever made – I bought a $9,000 electric cargo bike from Urban Arrow. In my Urban Arrow review, I will discuss what it is and why I decided to buy this bike, as well as discuss how impactful a bike like this can be on your journey to financial independence.

- Troxus Explorer Step-Thru Ebike – The Troxus Explorer Step-Thru is a fat-tire ebike that I’ve had the pleasure of riding for a while now. It has amazing power, great looks, and awesome range. If you’re looking for a great fat-tire ebike that offers a lot for the price, the Troxus Explorer Step-Thru is definitely one for you to consider. Check out my Troxus Explorer Step-Thru Review.

- Hovsco HovBeta Ebike – The HovBeta is a folding ebike with great specs and a lot of interesting features, and importantly, it’s sold at a good price point. I’ve had a blast commuting with it and using it to do deliveries with DoorDash, Uber Eats, and Grubhub. Check out my Hovsco HovBeta Ebike Review.

- Vanpowers Manidae Ebike – The Vanpowers Manidae is a fat tire ebike that I’ve been riding as my primary winter commuting bike and have also been using it to do food delivery with apps like DoorDash, Uber Eats, and Grubhub. After clocking in a decent number of miles with this ebike, I wanted to write a post sharing what my experience with the Vanpowers Manidae ebike has been like. Check out my Vanpowers Manidae Review.

- Sohamo S3 Step-Thru Folding EBike Review – A Great Value Folding Ebike – The Sohamo S3 Step-Thru Folding Ebike is an entry-level folding ebike that offers a lot of value for the price point. I’ve been riding the Sohamo S3 for a while now, putting the bike through its paces, and I have to say, this bike has exceeded all of my expectations. Check out my Sohamo Review.

- KBO Flip Ebike – The KBO Flip is an excellent bike. I’ve had a great time riding it and think it’s a versatile bike that can be used for a lot of purposes and can fit a variety of lifestyles. It’s worked out great for me as a general commuter bike and as a food delivery bike. Check out my KBO Flip Review.

- Hiboy P7 Commuter Ebike – The Hiboy P7 is an excellent electric commuter bike that’s offered at an affordable price point. The range and speed of this bike are both very good, so you won’t have any trouble getting anywhere you need to go with it. As a food delivery vehicle, this is also good – with how much range it offers, you’ll be able to work all day on a single charge. Check out my Hiboy P7 Commuter Electric Bike Review.

- Himiway Escape Ebike – The Himiway Escape is an interesting bike for anyone looking for a moped-style ebike. If you’re a gig economy worker, the Himiway Escape is particularly interesting and it’s possible to think of it as an investment, especially if you can opt to do deliveries with the Himiway versus using a car. It’s not cheap, but you can definitely make your money back when you compare the mileage you’ll put on your car versus using an ebike. Check out my Himiway Escape Bike Review.

- Espin Sport Ebike – The Espin Sport is a good ebike for someone who is looking for an ebike that feels and rides more like a regular bike. There are many ebikes that are really only bikes in name. In reality, they’re basically electric mopeds. The Espin Sport, by contrast, is a bike you could probably ride without the battery and you’d feel like you’re just riding a regular bike. Check out my Espin Sport Review.

- Varla Eagle One Scooter – The Varla Eagle One is an excellent scooter that can make sense for a lot of people. It can work as a primary mode of transportation. You can use it to work on gig economy apps like DoorDash, Uber Eats, and Grubhub. And it can also be a recreational vehicle if you’d prefer to use it for that. Check out my Varla Eagle One Review.

- Varla Falcon Scooter – The Varla Falcon is an excellent scooter that offers a good amount of power at a lower price point compared to more powerful scooters. It’s not exactly an entry-level scooter, nor is it a high-powered scooter. I think it fits somewhere in-between those two categories – an intermediate scooter if I had to give it a category. Check out my Varla Falcon Review.

- Hiboy S2 Scooter – The Hiboy S2 is an excellent entry-level commuter scooter that's perfect for someone looking to save some money in transportation costs and improve their commute. Check out my Hiboy S2 Review.

- Hiboy S2R Scooter – The Hiboy S2R is one of the more interesting electric scooters I’ve been able to test out. It’s not a high-powered scooter, but for an everyday transport option, it’s very useful, especially given some of the unique features that it has. Indeed, for the price, the Hiboy S2R might be the best value scooter I’ve used. Check out my Hiboy S2R Review.

- Fucare H3 Scooter – The Fucare H3 is a fun scooter and I’ve enjoyed testing it out. For a daily commuter or quick trips or errands, the Fucare H3 is probably the scooter I’ll use. It’s portable and easy to maneuver, so it’s just easier to take on the road when I need it. Check out my Fucare H3 Scooter Review.

More Recommended Investing App Bonuses

For additional investing app bonuses, be sure to check out the ones below:

- M1 Finance ($75) – This is a great robo-advisor that has no fees and allows you to create a customized portfolio based on your risk tolerance. You also get $75 for opening an account. Check out my M1 Finance Referral Bonus – Step-By-Step Guide.

- SoFi Invest ($25) – SoFi Invest is an easy brokerage account bonus that you can earn with just a few minutes of work. Use my SoFi Invest referral link, fund your SoFi Invest brokerage account with just $10 and you’ll get $25 of free stock. I also have a step-by-step guide for the SoFi Invest referral bonus.

- Robinhood (1 free stock) – Robinhood gives you a free stock valued between $2.50-$225 if you open an account using my referral link.

- Public (1 free stock) - Public gives you a free stock valued between $3-$70 if you open an account using my referral link.

More Recommended Bank Account Bonuses

If you’re looking for more easy bank bonuses, check out the below options. These bonuses are all easy to earn and have no fees or minimum balance requirements to worry about.

- Ally Bank ($100) – Of all the banks out there, Ally is, without a doubt, my favorite. At the moment, Ally is offering $100 to customers who open an eligible Ally account and meet the requirements. Here are the step-by-step directions to earn your Ally Bank referral bonus.

- Chime ($100) - Chime is a free bank account that offers a referral bonus if you use a referral link and complete a direct deposit of $200 or more. In practice, any ACH transfer into this account triggers the bonus. This bonus is easy to earn and posts instantly, so you’ll know if you met the requirements as soon as you move money into the account. I wrote a step-by-step guide on how to earn your Chime referral bonus that I recommend you check out.

- US Bank Business ($400/$1200) – This is a fairly easy bank bonus to earn, since there are no direct deposit requirements. In addition, you can open the Silver Business Checking account, which comes with no monthly fees. Check out how to earn this big bonus here.

- Current ($50) – Current is a free fintech bank that’s offering new users a $50 referral bonus after signing up for an account using a referral link. Current is an easy bonus to earn and also gives you access to three savings accounts that pay you 4% interest on up to $2,000. That means you can put away up to $6,000 earning 4% interest. That’s very good and makes Current an account I recommend to everyone. Check out my step-by-step guide on how to earn your Current Bank bonus.

- Novo Bank ($40) - Novo bank is a free business checking account that’s currently offering a $40 bonus if you open a Novo business checking account using a referral link. In addition to being a good bank bonus, Novo is also a good business checking account. It has no monthly fees or minimum balance requirements and operates a good app and website. Indeed, it’s the business checking account I currently use for this blog. Check out my post on how to easily open a Novo account.

- Varo ($25) – Varo is a free fintech banking app similar to Chime or Current. It’s currently offering a $25 bonus to new users that open a new Varo account with a referral link. The bonus for this bank is very easy to meet, all you need to do is spend $20 within 30 days of opening your Varo account. Check out my step-by-step guide to learn how to earn this bonus.

Kevin is an attorney and the blogger behind Financial Panther, a blog about personal finance, travel hacking, and side hustling using the gig economy. He paid off $87,000 worth of student loans in just 2.5 years by choosing not to live like a big shot lawyer.

Kevin is passionate about earning money using the gig economy and you can see all the ways he makes extra income every month in his side hustle reports.

Kevin is also big on using the latest fintech apps to improve his finances. Some of Kevin's favorite fintech apps include:

- SoFi Money. A really good checking account with absolutely no fees. You'll get a $25 referral bonus if you open a SoFi Money account with a referral link, and an additional $300 if you complete a direct deposit.

- 5% Savings Accounts. I'm currently getting 5.24% interest on my savings through a company called Raisin. Opening a Raisin account takes minutes to complete, it's free, and all of your funds are FDIC-insured. I explain how it works, why I'm now using it to store my emergency fund and any other cash savings I have, and why I recommend everyone check it out in this review.

- US Bank Business. US Bank is currently offering new business customers a $400/$1200 signup bonus after opening a new account and meeting certain requirements.

- M1 Finance. This is a great robo-advisor that has no fees and allows you to create a customized portfolio based on your risk tolerance. You also get $75 for opening an account.

- Empower. One of best free apps you can use to monitor your portfolio and track your net worth. This is one of the apps I use to track my financial accounts.

Feel free to send Kevin a message here.

Nice article

Thanks!

I put it off for years, too, but jumped into the game just this week. I’m very excited! For me, what held me back was how complicated it seemed. Transferring all of my monthly payments to a new card, tracking to make sure I met the minimum spend, etc. but I’m going for it now! I have plans to get 5 cards in the first year with a potential 340,000+ point return! That’s already up 50,000 from the plan I had just a week ago, hahahaha.

That’s what held me off for so long as well – just how complicated it seemed. I just didn’t understand how it was possible until I actually jumped in.

Wow, what a great and useful post!

I’ve also ignored travel hacking as it sounded too good to be true and I was afraid of damaging my credit score by opening too many cards. I don’t have any debt and I’m obsessed with keeping my credit score over 800.

The other thing that kept me from taking advantage of travel hacking was the annual fees; however, as you point out, we have to look at it differently as a small fee to get bigger rewards.

Reading your post has changed my mind and I might give travel hacking a try. Thanks a bunch!

Thanks! I was also nervous about opening up new cards since I thought it’d mess up my credit score, but over the long term, your score will stay the same or go up. Yes, your average age of credit will drop, but you just keep adding more credit, which is a net gain long term. It’s intimidating getting started, but once you start doing it and understand how it all works, you’ll start wondering how you ever didn’t travel hack! It’s a fun little hobby.

I recently got into travel hacking and while i am confident that the deals can be had so far when i do sample tests on various airlines with points it doesnt seem to be as amazing as people talk about. From my searches, a person could save maybe $200 by using points versus cash.

I wonder how that Jamacia trip was totally free. I would take it myself if i knew how.

So this is definitely something that requires a little bit of learning. It involves transferring points to different airline partners and having flexibility with traveling.

For example, my friend recently booked a ticket to Hawaii for August using his Chase Ultimate Rewards Points. American Airlines (or maybe United – I can’t remember of the top of my head) has flights to anywhere in North America for 25,000 points. He transferred the points, and booked the ticket, which would otherwise cost close to $1,000 if he booked it with cash. And he still has 75,000 Chase Points left over from when he first snagged the bonus.

If you use just the Credit Cards portals, you’ll find that it’s not quite as much value.

For the Jamaica trip (which I haven’t done, but as Mr. Crazy Kicks pretty much explained), it involved this type of transferring. Plus opening up a few hotel cards and snagging the free nights.

I was totally skeptical about it too just a few months ago – the information is out there, but not always all that well organized. Once you understand how it works, there’s ways to get a ton of value from these points.

Happy travel hacking! When we first started I was very anti-fee too, but I’ve since learned the fee is worth it if the rewards are high enough. Another pleasant surprise was how little it affected our credit score.

Looking forward to reading about the trips you’ll be planning with all those points!

Oh I’ve got a bunch of ideas. My only problem is time! I need to save money and retire like you!

I got into Travel Hacking just over a year ago, and my credit score is still over 800 after opening 6 cards. I’m actually planning on opening my 7th card this week!

Highly recommend the TravelMiles101 free course to anyone interested in getting started.

That’s awesome! I’ve now opened up 4 cards this year and have plans to open up at least 3 more over the next few months. Another big benefit with side hustling – you can legitimately open up business cards and snag the bonuses.

Excellent write-up, FP. I have been listening to ChooseFI since you recommended it in a recent post. The guys over at ChooseFI had a podcast episode that explained travel hacking and it was great. I went with the Chase card they recommended to start my travel hacking journey. I’m interested and I will investigate the VISA you discussed.

Cheers!

Yep, I think Chase Sapphire Preferred is probably the first and easiest card to start with since it has no annual fee for the first year and is easy enough to just product change it down to a Chase Freedom or Chase Freedom Unlimited.

I’ve been resisting travel hacking too. Did you take one of those free courses on it or use an aggregator site that describes how many of those cards work? I’m looking forward to reading along as you learn more.

I sort of just dove all into it and have been figuring things out along the way. The subreddit “churning” board has a wealth of information. There are a ton of YouTube channels out there with a lot of good info as well. This Youtube channel/blog Ask Sebby has been really helpful in figuring stuff out too, and totally recommend checking them out if you’ve got the time to watch a few YouTube videos.

Thanks for the tips!

We’ve been travel hacking for about four years with no I’ll effects. In fact we are in Cancun today enjoying some of those points.

Oh man, that’s lucky! I wish I had figured this stuff out sooner.

Right on! Travel hacking has been a lot more lucrative than I expected. We just travel hacked an all inclusive vacation including flights to Jamaica for free – value $6,000. We also flew to Colorado and Costa Rica for free, and we are getting ready to go to Barcelona – all for free.

I have yet to find any downsides. After churning through more than half a dozen cards my credit score is still over 800 🙂

I can totally see why travel hacking is so addictive. I’m basically diving in headfirst into it and trying to understand it all. It’s complicated – there’s definitely a lot to it, no matter how simple anyone makes it seem. But man is it fun.