One of the mistakes a lot of people make when they first start side hustling is mixing their side hustle income and their day job income into their main checking account. Aside from the obvious administrative hassles that come with doing this, the biggest problem really has to do with the fact that your main checking account just really isn’t designed to handle things beyond your typical paychecks.

It bears repeating because I think a lot of people forget this, but the money you earn from your side hustle isn’t the same thing as a paycheck. No matter what it is you’re doing – even if it’s just the simple gigs I do like dog walking and delivering food – you need to think of your side hustle earnings as business income. You can’t just treat your side hustle income like it’s a paycheck. Rather, your paycheck is ultimately what you decide to pay yourself after you’ve taken care of expenses and taxes.

Because of how side hustle income works, it’s important to create systems so that the money we earn from our side hustles can flow to the appropriate places.

I tend to think of side hustle income as flowing into three places:

- Business Expenses

- Taxes

- The Money You Pay Yourself As Your “Paycheck”

So, if you make $100 side hustling, you need to divide that up. Some of it needs to go to taxes. Some of it goes to business expenses. And once those two things are taken care of, the rest can be paid out to you like it’s your paycheck. Most people forget about those first two things and instead, skip right to the paycheck part, treating the entire amount they earn from side hustling as their own money. And this can lead to issues later down the line.

For a long time, I had a really simple system in place since I didn’t actually spend any of my side hustle income. In my simple system, all of my side hustle income simply went into a sub-savings account that I created with Capital One 360. At the end of each year, I paid my taxes using that account, then put the rest of it into a Solo 401k that I opened with Fidelity.

Things have recently changed however since I quit my job to go all-in on this blog. Instead of being bonus money, my side hustle income is now money that I might actually need to use in order to cover my living expenses. As a result, I’ve had to create a new system to appropriately handle this flow of money.

In today’s post, I want to go over the system I’ve set up to handle my side hustle income and explain how it works. If you’re a side hustler, I highly recommend that you either use my system or set up a system similar to this. The important thing is you need something in place to manage your side hustle income and make sure it’s all going to the appropriate places.

How To Manage Your Side Hustle Income

At the outset, there are three main things you need in order to properly manage your side hustle income.

The first is a bank account dedicated solely for your side hustle income. All of the money that you make from side hustling should go directly into this bank account first. Think of this bank account as your side hustle inbox. All of your side hustle money goes in there and then you need to figure out what to do with it. Does it stay in there? Does it move somewhere else? That’s up to you to decide. This bank account should only be used to pay for business expenses (you’ll pay your personal expenses from your normal, personal checking account, discussed below).

The second thing you’ll need is a separate bank account for your taxes. A lot of people that start side hustling forget this, but in general, when you’re side hustling, you are your own business and you are the one responsible for paying taxes. The big mistake a lot of people make is spending all of the money they make, then finding out that they owe a bunch of taxes at the end of the year with no way to pay for it. Don’t let that happen to you. Whenever any money goes into your side hustle bank account, some of it needs to go into your tax bank account.

The final thing you need – and this is probably obvious – is a checking account that you use for your personal expenses. This is basically your primary personal bank account and the one that your paychecks go into and that you pay your personal bills from (rent, mortgage, utilities, food, etc). When you “pay” yourself from your side hustle, you should be paying yourself into this bank account, just as if you were paying yourself a paycheck.

A bonus thing that isn’t required, but that you should consider utilizing, is the Solo 401k. This is essentially a retirement account that you create for yourself. I’ve written about this “side hustler’s bonus retirement account” before and I’ve also walked through how to set up a Solo 401k with Fidelity in this post.

An example might help to clarify the above:

- If you make $100 from side hustling, it should first go directly into your side hustle bank account (i.e. your side hustle inbox). Any business expenses should be paid directly from that bank account.

- At least 1/3 of that $100 should then go into a separate bank account designated just for your taxes. You’ll use this bank account to pay taxes either quarterly or at the end of the year.

- Finally, whatever is left over can then be transferred to your personal checking account as a sort of paycheck to yourself. From that paycheck, some percentage of it should be set aside to fund your Solo 401k.

With all that said, there are two primary apps that I use in my money system that I want to share with you today:

- Chime: A free checking account that I use for my side hustle income.

- Catch: A free savings and benefits app for independent contractors that I use to automate my taxes.

Below is an explanation of what these apps are and how I utilize them.

Chime: My Primary Side Hustle Checking Account

My current primary checking account that all of my gig economy stuff goes into is Chime. I initially opened this account purely because it offered a $50 account opening bonus, and initially, I had no plans to actually use this account for anything. (As a side note, just like with credit cards, banks will often offer signup bonuses if you open a new account with them and meet certain requirements. You can make a good chunk of money by taking advantage of these offers, as I’ve written about in my ultimate guide to bank account bonuses.)

Of course, this is why bank accounts offer these signup bonuses, because their hope is that you’ll like their stuff enough that you end up becoming a customer. That’s exactly what happened with me – I ended up liking Chime’s interface, and since I needed a dedicated checking account for my side hustle income, I decided to give them a shot. Chime had a couple of things that appealed to me:

- No fees of any sort;

- A very good app and web interface; and

- Money posts into the account 2 days early, making it so that when I got paid, the money would often be there by the next day or even the same day I was paid.

As explained previously, all of the side hustle income I make goes directly into this bank account. The money then either stays in that account, gets sent to my tax account, or is sent to my personal checking account as a paycheck to myself.

You don’t have to use Chime, of course. I just wanted to share the system I use, but you can use any checking account you want so long as it makes sense for you. The important thing is to use a separate bank account for your side hustle income and to make sure that it’s totally free with no account minimums (in fact, I think the free part is basically non-negotiable).

If you don’t like Chime, there are other options you can use. I’ve listed a few below that I think are also good options for a side hustle bank account. They’re all 100% free with no fees and no account minimums.

- Varo (offers a $75 signup bonus if you do a direct deposit of $200 – this can typically be met by doing an ACH transfer from any other bank)

- SoFi Money (offers a $25-$50 signup bonus if you fund the account with $100)

- Lili (a new bank I just found that is created for freelancers and gig workers)

- Ally (probably the best overall bank out there)

- Discover (a good bank account that I use for my Airbnb income)

- Simple (the bank account I use for my personal checking account, but you could use for side hustle income too)

There are way more banks out there that you can use – far too many for me to list them all here. Just pick what works for you so long as it’s a free bank account that does what you need it to do. (Chime is still offering a $50 bonus if you open an account and do a direct deposit of $200 or more. This requirement can be met by doing an ACH transfer from pretty much any bank.)

Catch: The App I Use To Save For Taxes

The secret weapon in this money system is Catch, which is definitely one of the best new fintech apps I’ve found in the past year. I’m not even sure how I found this app, but without a doubt, if you are side hustling, this is something you definitely need to use.

Here’s how Catch works. One of the things you have to remember is that unlike a paycheck, your side hustle income comes to you with no taxes taken out of it. Generally, you need to take at least 1/3 of the side hustle income you make and set it aside so you can pay taxes later down the line.

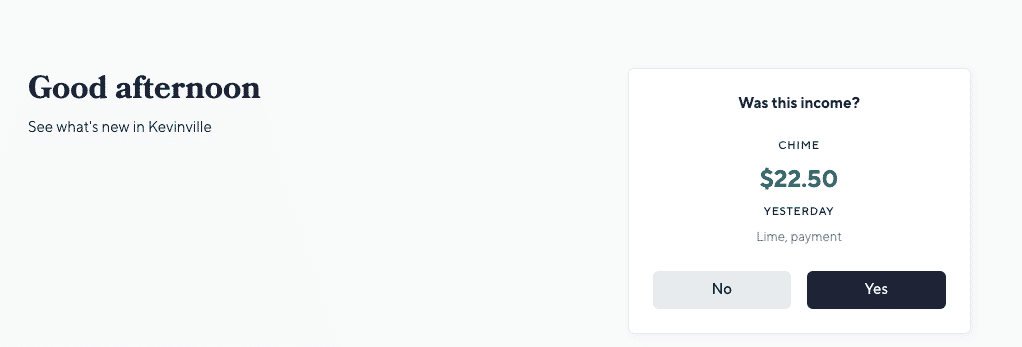

Catch does this automatically for you. To do this, you give Catch some info about how much money you make annually. Catch will then suggest how much it should save for taxes (you can adjust this number as needed). You then link Catch to your checking account and the app will monitor your transactions for you. Every time Catch sees new money come into your bank account, it’ll ask you to confirm if that was or wasn’t income. If you confirm that it was income, Catch automatically pulls money from your checking account and puts it into a separate FDIC insured bank account.

Here’s what it looks like when you get a new transaction into your bank account. As you can see, I recently received payment for one of my gigs and Catch is asking me if this is income.

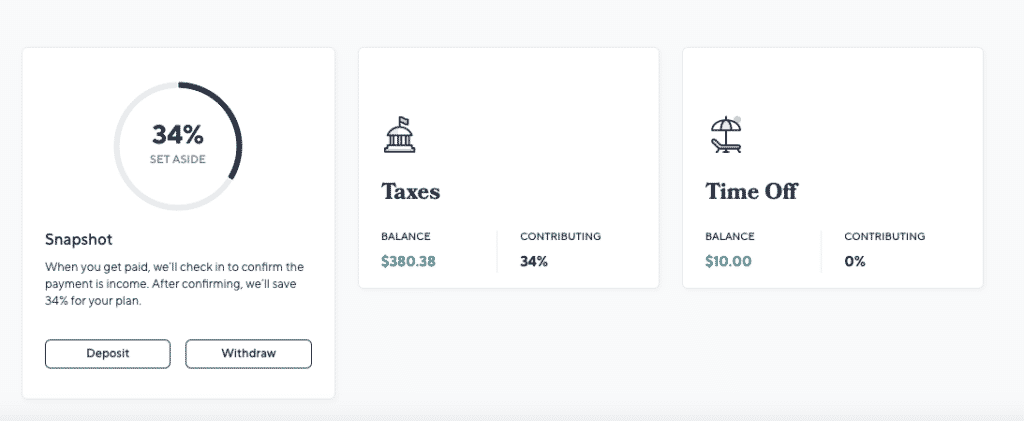

Since this was income, I click yes. It then brings me to this screen where it breaks down my taxes and any other savings I want to do.

Since this was income, I click yes. It then brings me to this screen where it breaks down my taxes and any other savings I want to do.

Once I confirm it, my money is then moved to a separate FDIC insured savings account, as shown in the screenshot below. One thing to note is that this Catch savings account doesn’t earn any interest, but there’s an easy way to remedy this problem (which I’ll go into later in this post).

Once I confirm it, my money is then moved to a separate FDIC insured savings account, as shown in the screenshot below. One thing to note is that this Catch savings account doesn’t earn any interest, but there’s an easy way to remedy this problem (which I’ll go into later in this post).

The big thing is that Catch is free, which is why I started using it (regular readers of this blog know that I’m not a big fan of paying for any fintech products and especially paying for any product that is designed to help you save money). This app is seriously worth using and it makes it much easier for me to save for taxes since I no longer have to manually remember to set aside money for taxes each month.

Putting It All Together To Make The Perfect Side Hustle Money System

I’ve been side hustling for a while now, and this current system of combining Chime and Catch has worked out perfectly for me. All of my side hustle income goes into my Chime account. From there money goes to where it needs to go each day. Catch monitors my income and saves money for my taxes. I pay myself a paycheck from my Chime account to my personal bank account. And then I save as much as I can to a Solo 401k that I’ve created for my side hustle income.

One thing to remember is that the money Catch sets aside for taxes is saved in a saving account that doesn’t earn you any interest. This might not be that big a deal depending on how often you pay your taxes and how much you are setting aside.

My solution to this problem is each month, I simply withdraw all of the money in my Catch savings account, then move it to a separate, high-yield savings account that I set up with Ally. That way, I get the tax automation with Catch, but also earn interest on the money I’m saving for taxes. It takes me only a few minutes to do this each month.

Note that this is the system I’m currently using for all of my sharing economy/gig economy stuff. I use a free business checking account for this blog from Azlo (which I can probably talk about in a future post) and that has its own system.

The key takeaway here is to have a system in place for your side hustle income. Money should be flowing without you having to think about it too much. Take some time to set this up once and it’ll all start working like clockwork.

This post may contain affiliate links.

More Recommended Ebike/Scooters

Check out these other ebikes and scooters I've reviewed:

- Urban Arrow Ebike – Last year, I made one of the largest purchases I’ve ever made – I bought a $9,000 electric cargo bike from Urban Arrow. In my Urban Arrow review, I will discuss what it is and why I decided to buy this bike, as well as discuss how impactful a bike like this can be on your journey to financial independence.

- Troxus Explorer Step-Thru Ebike – The Troxus Explorer Step-Thru is a fat-tire ebike that I’ve had the pleasure of riding for a while now. It has amazing power, great looks, and awesome range. If you’re looking for a great fat-tire ebike that offers a lot for the price, the Troxus Explorer Step-Thru is definitely one for you to consider. Check out my Troxus Explorer Step-Thru Review.

- Hovsco HovBeta Ebike – The HovBeta is a folding ebike with great specs and a lot of interesting features, and importantly, it’s sold at a good price point. I’ve had a blast commuting with it and using it to do deliveries with DoorDash, Uber Eats, and Grubhub. Check out my Hovsco HovBeta Ebike Review.

- Vanpowers Manidae Ebike – The Vanpowers Manidae is a fat tire ebike that I’ve been riding as my primary winter commuting bike and have also been using it to do food delivery with apps like DoorDash, Uber Eats, and Grubhub. After clocking in a decent number of miles with this ebike, I wanted to write a post sharing what my experience with the Vanpowers Manidae ebike has been like. Check out my Vanpowers Manidae Review.

- Sohamo S3 Step-Thru Folding EBike Review – A Great Value Folding Ebike – The Sohamo S3 Step-Thru Folding Ebike is an entry-level folding ebike that offers a lot of value for the price point. I’ve been riding the Sohamo S3 for a while now, putting the bike through its paces, and I have to say, this bike has exceeded all of my expectations. Check out my Sohamo Review.

- KBO Flip Ebike – The KBO Flip is an excellent bike. I’ve had a great time riding it and think it’s a versatile bike that can be used for a lot of purposes and can fit a variety of lifestyles. It’s worked out great for me as a general commuter bike and as a food delivery bike. Check out my KBO Flip Review.

- Hiboy P7 Commuter Ebike – The Hiboy P7 is an excellent electric commuter bike that’s offered at an affordable price point. The range and speed of this bike are both very good, so you won’t have any trouble getting anywhere you need to go with it. As a food delivery vehicle, this is also good – with how much range it offers, you’ll be able to work all day on a single charge. Check out my Hiboy P7 Commuter Electric Bike Review.

- Himiway Escape Ebike – The Himiway Escape is an interesting bike for anyone looking for a moped-style ebike. If you’re a gig economy worker, the Himiway Escape is particularly interesting and it’s possible to think of it as an investment, especially if you can opt to do deliveries with the Himiway versus using a car. It’s not cheap, but you can definitely make your money back when you compare the mileage you’ll put on your car versus using an ebike. Check out my Himiway Escape Bike Review.

- Espin Sport Ebike – The Espin Sport is a good ebike for someone who is looking for an ebike that feels and rides more like a regular bike. There are many ebikes that are really only bikes in name. In reality, they’re basically electric mopeds. The Espin Sport, by contrast, is a bike you could probably ride without the battery and you’d feel like you’re just riding a regular bike. Check out my Espin Sport Review.

- Varla Eagle One Scooter – The Varla Eagle One is an excellent scooter that can make sense for a lot of people. It can work as a primary mode of transportation. You can use it to work on gig economy apps like DoorDash, Uber Eats, and Grubhub. And it can also be a recreational vehicle if you’d prefer to use it for that. Check out my Varla Eagle One Review.

- Varla Falcon Scooter – The Varla Falcon is an excellent scooter that offers a good amount of power at a lower price point compared to more powerful scooters. It’s not exactly an entry-level scooter, nor is it a high-powered scooter. I think it fits somewhere in-between those two categories – an intermediate scooter if I had to give it a category. Check out my Varla Falcon Review.

- Hiboy S2 Scooter – The Hiboy S2 is an excellent entry-level commuter scooter that's perfect for someone looking to save some money in transportation costs and improve their commute. Check out my Hiboy S2 Review.

- Hiboy S2R Scooter – The Hiboy S2R is one of the more interesting electric scooters I’ve been able to test out. It’s not a high-powered scooter, but for an everyday transport option, it’s very useful, especially given some of the unique features that it has. Indeed, for the price, the Hiboy S2R might be the best value scooter I’ve used. Check out my Hiboy S2R Review.

- Fucare H3 Scooter – The Fucare H3 is a fun scooter and I’ve enjoyed testing it out. For a daily commuter or quick trips or errands, the Fucare H3 is probably the scooter I’ll use. It’s portable and easy to maneuver, so it’s just easier to take on the road when I need it. Check out my Fucare H3 Scooter Review.

More Recommended Investing App Bonuses

For additional investing app bonuses, be sure to check out the ones below:

- M1 Finance ($75) – This is a great robo-advisor that has no fees and allows you to create a customized portfolio based on your risk tolerance. You also get $75 for opening an account. Check out my M1 Finance Referral Bonus – Step-By-Step Guide.

- SoFi Invest ($25) – SoFi Invest is an easy brokerage account bonus that you can earn with just a few minutes of work. Use my SoFi Invest referral link, fund your SoFi Invest brokerage account with just $10 and you’ll get $25 of free stock. I also have a step-by-step guide for the SoFi Invest referral bonus.

- Robinhood (1 free stock) – Robinhood gives you a free stock valued between $2.50-$225 if you open an account using my referral link.

- Public (1 free stock) - Public gives you a free stock valued between $3-$70 if you open an account using my referral link.

More Recommended Bank Account Bonuses

If you’re looking for more easy bank bonuses, check out the below options. These bonuses are all easy to earn and have no fees or minimum balance requirements to worry about.

- Ally Bank ($100) – Of all the banks out there, Ally is, without a doubt, my favorite. At the moment, Ally is offering $100 to customers who open an eligible Ally account and meet the requirements. Here are the step-by-step directions to earn your Ally Bank referral bonus.

- Chime ($100) - Chime is a free bank account that offers a referral bonus if you use a referral link and complete a direct deposit of $200 or more. In practice, any ACH transfer into this account triggers the bonus. This bonus is easy to earn and posts instantly, so you’ll know if you met the requirements as soon as you move money into the account. I wrote a step-by-step guide on how to earn your Chime referral bonus that I recommend you check out.

- US Bank Business ($400/$1200) – This is a fairly easy bank bonus to earn, since there are no direct deposit requirements. In addition, you can open the Silver Business Checking account, which comes with no monthly fees. Check out how to earn this big bonus here.

- Current ($50) – Current is a free fintech bank that’s offering new users a $50 referral bonus after signing up for an account using a referral link. Current is an easy bonus to earn and also gives you access to three savings accounts that pay you 4% interest on up to $2,000. That means you can put away up to $6,000 earning 4% interest. That’s very good and makes Current an account I recommend to everyone. Check out my step-by-step guide on how to earn your Current Bank bonus.

- Novo Bank ($40) - Novo bank is a free business checking account that’s currently offering a $40 bonus if you open a Novo business checking account using a referral link. In addition to being a good bank bonus, Novo is also a good business checking account. It has no monthly fees or minimum balance requirements and operates a good app and website. Indeed, it’s the business checking account I currently use for this blog. Check out my post on how to easily open a Novo account.

- Varo ($25) – Varo is a free fintech banking app similar to Chime or Current. It’s currently offering a $25 bonus to new users that open a new Varo account with a referral link. The bonus for this bank is very easy to meet, all you need to do is spend $20 within 30 days of opening your Varo account. Check out my step-by-step guide to learn how to earn this bonus.

Kevin is an attorney and the blogger behind Financial Panther, a blog about personal finance, travel hacking, and side hustling using the gig economy. He paid off $87,000 worth of student loans in just 2.5 years by choosing not to live like a big shot lawyer.

Kevin is passionate about earning money using the gig economy and you can see all the ways he makes extra income every month in his side hustle reports.

Kevin is also big on using the latest fintech apps to improve his finances. Some of Kevin's favorite fintech apps include:

- SoFi Money. A really good checking account with absolutely no fees. You'll get a $25 referral bonus if you open a SoFi Money account with a referral link, and an additional $300 if you complete a direct deposit.

- 5% Savings Accounts. I'm currently getting 5.24% interest on my savings through a company called Raisin. Opening a Raisin account takes minutes to complete, it's free, and all of your funds are FDIC-insured. I explain how it works, why I'm now using it to store my emergency fund and any other cash savings I have, and why I recommend everyone check it out in this review.

- US Bank Business. US Bank is currently offering new business customers a $400/$1200 signup bonus after opening a new account and meeting certain requirements.

- M1 Finance. This is a great robo-advisor that has no fees and allows you to create a customized portfolio based on your risk tolerance. You also get $75 for opening an account.

- Empower. One of best free apps you can use to monitor your portfolio and track your net worth. This is one of the apps I use to track my financial accounts.

Feel free to send Kevin a message here.

Interesting, but I feel this is only better for people who need the spending money everyday/week otherwise it’s a lot more work/clicks. Currently I just have all my side hustle income go into an Ally account, and then at the end of the month I check my Mint for how much I made that month from Side Hustles and then transfer the appropriate amount to my Side Hustle Taxes account and the rest to a different account(currently Student Loans)

Yep, it’s definitely more important if you’re actually using the income (which I will soon need to do). It sounds like you have your system in place already, which is very key – most people don’t have any system at all.

With that said, I think Catch is still pretty valuable just because of the automation aspect of it. It takes a few clicks, but you basically just get a notification whenever you’ve been paid, then click 1 button. So basically keeping up with everything as it goes, rather than having to remember each month.

Can you make some comments about being paid in Amazon Gift Card. Both my side hustle of Product Tube and Job Seeker pay in this fashion. Are there any tax implications. What about your general thoughts?

Thank you

Matt

Hey Matt. General rule is that any income – regardless of source – is taxable income. As a result, yes, being paid in gift cards is technically taxable income. You won’t get a 1099 from these apps though.

I had not heard of Chime or Catch so this is very useful. I came to entrepreeurship after a longtime corporate career and my husband was still in corporate when I started (he’s now a consultant like me). So we also kept our traditional brick and mortar bank accounts, and I used our HELOC to smooth out our monthly expenses and then funneled all my consulting income into repaying the HELOC. I paid quarterly estimated taxes so I would catch up on taxes on a regular basis, and before the last quarter I reconciled with my accountant what the actual tax number would be so there wouldn’t be a big surprise. That said, you can only use your HELOC if you have discipline not to overspend.

I’ve read about the HELOC strategy, but haven’t had the guts to try it. Definitely requires discipline, which most of us reading this probably have, but I’m still too much of a newb to understand how HELOCs work exactly. Might be something I need to research.

Hey MPLS downtown friend.

Started the Chime today $50 for you and me . Thank u.

Started Lime charge because I can walk to snd from drop offs as fun exercise game- and adds up. Teaches me the value of $4.50… I won’t buy items now because I know how many limes I have to charge. Good training.

My question is… can I use the Lime daily payment as a direct deposit to meet the $200 requirement and then change where Lime deposits every month??

Thanks!

Hey Pat. My wife seriously laughed out loud when she read your comment about the value of $4.50. Spoken like a true Lime scooter juicer, haha.

So don’t use Lime to meet the direct deposit requirement, because you need to deposit $200 in one transaction, which there’s no way to do that with Lime.

To meet the Chime requirement, just do an ACH transfer from your regular bank account. So whatever bank you use, go to their website and link it to Chime. Then transfer $200 to your Chime account from your bank account’s website. If it triggered as a direct deposit, then it’ll post your $50 immediately. If not, try again with a different bank.

I used Discover and that triggered it. My brother and my wife both used Ally and it triggered for them. The datapoints I’ve seen show that basically any bank transfer will trigger as a direct deposit. Hope that helps. Hit me up if you have questions. My bank account bonus post does a good job of explaining how these work if you need more info.

Yes. Will try again with my TCF and if that doesn’t work – will start the ally account now.

I thought the $200 could be multiple transactions that add up to $200.🤦🏼♀️

Glad your wife appreciates. It is how I explain it to my husband— it not about the $$ – it more about the good habits and having fun.

I look at lime as a game that pays. Saving in chime now so I can spend on gifts and one long term goal. Requires strategy. Keeps me from over spend at Target. It is fun way to see a scooter, reserve it, turn on my Apple Watch to track my walk. Gets me walking to a destination instead of to Trader Jose or Whole Foods… my previous destination walks.

Thx for response.

TCF should work – I think they finally added the ability to link external accounts!

The reserve feature is really big, especially for the casual charger like us. Last year, I basically had to go run to a scooter if I saw it. Now, if I see one nearby, I can just reserve it, then walk over there with my dog.