When I was in college, I picked up a copy of The Automatic Millionaire by David Bach. His book is still one of my favorite money books and probably the first book I recommend to anyone beginning to learn about personal finance.

When I first read Bach’s book, I too, wanted to become an Automatic Millionaire! One chapter in his book talked about setting up an IRA or a Roth IRA. I was a 19-year-old kid at the time, so I didn’t have a clue what that meant. All I knew was that it was something good! After reading The Automatic Millionaire, I hopped onto E*Trade, opened up a Roth IRA, and transferred $100 into my Roth IRA account.

And then, I was stuck. I remember The Automatic Millionaire talking about investing in mutual funds, but I didn’t really know what that meant or how to put my money into that type of investment.

After tinkering around on E*Trade and trying to figure out how to put my 100 bucks to work, I ended up finding a cheap stock for a bookstore company you might remember called Borders. Back then, Border’s share price was around $3 per share. I thought for sure that Borders was too big to fail! Well, we all know what happened there.

I never did figure out the Roth IRA thing while I was in college. Eventually, I even forgot that I had opened one. And I didn’t put another dime into any sort of investment vehicle until I was around 27 years old.

When I tried my hand at opening a retirement account, I thought it would be like opening a bank account. The way I visualized it, you put money into your retirement account and then left it to grow over time.

But that’s not at all what it was like! You couldn’t just put money into a retirement account. You also had to know where to put your money once it was in the account.

This is where robo advisors come into play. I’m a huge fan of robo advisors because of how easy they are to set up and how much they open up the world of investing to your average joe who knows nothing about investing.

For those of you that don’t know, robo advisors are automated investment platforms that invest your money for you in an appropriate allocation based on your age and risk tolerance. Examples of popular robo advisors include services like Betterment, Wealthfront, or M1 Finance.

All of these services are great and do one thing very well. They take away the biggest problem facing any new investor – simply getting started.

Not Everyone Is Into Money

I know, I find it hard to believe! But it’s true. Not everyone is a money nerd.

If you’re into personal finance, then investing seems really simple. Open up a retirement account, pick a Total Stock Market Index Fund with low expense ratios, and consistently invest money over time.

But the actual process of getting started isn’t all that simple if you have no idea what you’re doing! Tell a regular person to do the above and they’ll have no idea what you’re talking about or how to go about doing that.

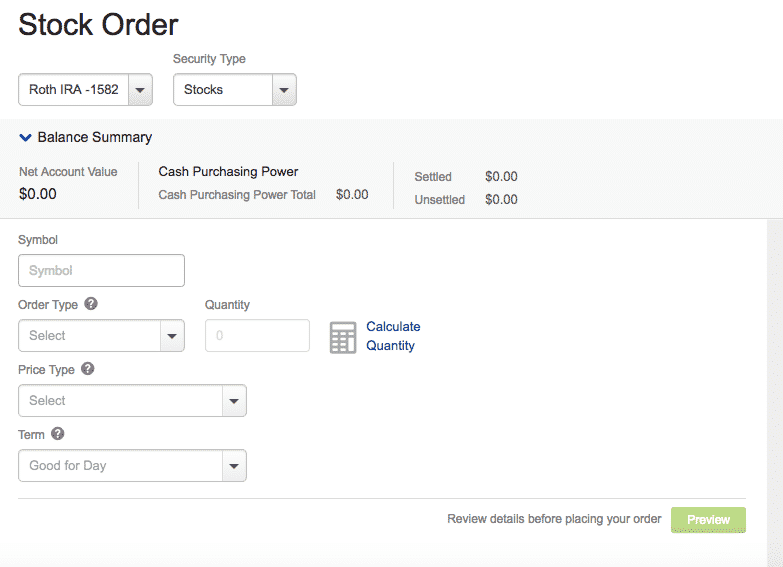

Here’s what I mean. Let’s look at your typical E*Trade brokerage order screen:

This entire thing looks pretty intimidating if you have no background in investing. Look at all the drop-down boxes! And I have to enter in all sorts of weird information that I don’t understand. To a newbie starting out – and we were all newbies once – this might as well be a different language.

If you make something too complicated, many people will quit before they get started. That’s exactly what happened to me when I was in college and trying to start up my first retirement account. I never got started because the entire process was too complicated.

The Impact Of Friction

The main thing stopping most people from doing any particular task is the amount of friction between doing nothing vs. getting started. The more perceived work it takes to do something, the less likely we are to start doing it, and the more likely we’ll look for easier alternatives.

An example I always use to demonstrate the problem of “friction” is the ridership of city bus systems vs. train or subway systems. Compare the two modes of mass transit. A train is much easier for a regular person to use when compared to a bus. Trains have easily recognizable stations. Their schedules are more obvious. You can pay for the ride before you board. Most importantly, trains are on tracks. You know exactly where you’re going when you hop on a train. These are all things that are comforting to a new rider.

In contrast, look at your average bus system. Buses take a bit more work to figure out. Stops sometimes appear to be randomly placed (often just a pole at an intersection). You don’t always know the bus schedule. And unless you have a bus pass, you need to plan on how you’ll pay for the ride before you hop on the bus. But the most frightening thing is not knowing where a particular bus is going. Buses aren’t on tracks. To a new bus rider, hopping on a bus can be a scary experience.

I’d wager that every person who rides a bus is also willing to ride a train or subway. But not everyone that rides a train is willing to use a bus. A train will attract more people simply because it’s easier to use. There’s less friction for your average joe to overcome.

Robo Advisors Remove A Ton Of Friction From The Investing Process

The biggest benefit of a robo advisor is their ability to remove friction from the investing process. You don’t have to know what you’re doing. All you need to do is open up an account and put money in.

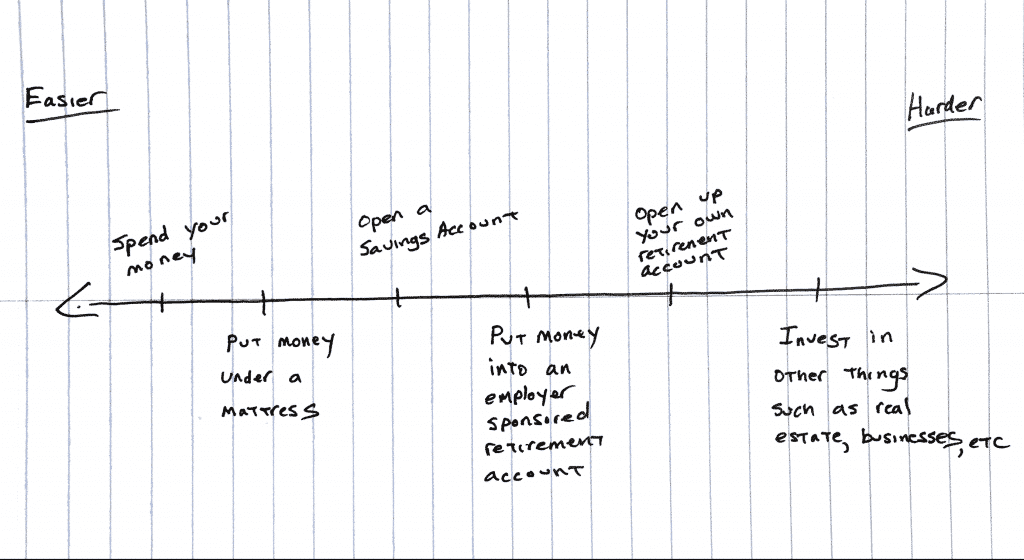

If we had a spectrum of the easiest ways to use your money, it’d probably look something like this:

Some takeaways:

- Spending your money falls to the left of the spectrum and is the easiest way to use your money. The friction in using your money in this manner is low. Anyone can do it!

- Putting money away takes a little bit more work. But opening up a savings account isn’t particularly difficult. All you need to do is set one up at basically any bank and throw some money into it. You don’t have to do much thinking beyond that.

- Putting money into an employer-sponsored retirement plan, such as a 401(k), also isn’t too difficult. A lot of employers automatically take a certain percentage of your paycheck and invest it into a default investment option unless you opt-out. This is exactly what happened to me in my first year of work.

Investing outside of work is when the friction really ramps up. You can see how confusing investing can look if you know absolutely nothing about it. Robo advisors remove this friction.

And this is the ultimate benefit that makes robo advisors worthwhile. For the person who knows nothing about investing, it suddenly becomes as easy as putting money into a savings account. Investing suddenly slides to the left of the difficulty spectrum. It’s the equivalent of taking a train versus taking a bus. Fewer barriers to entry mean more people take that initial first step of investing their money. That’s worthwhile in my book.

This post may contain affiliate links.

More Recommended Ebike/Scooters

Check out these other ebikes and scooters I've reviewed:

- Urban Arrow Ebike – Last year, I made one of the largest purchases I’ve ever made – I bought a $9,000 electric cargo bike from Urban Arrow. In my Urban Arrow review, I will discuss what it is and why I decided to buy this bike, as well as discuss how impactful a bike like this can be on your journey to financial independence.

- Troxus Explorer Step-Thru Ebike – The Troxus Explorer Step-Thru is a fat-tire ebike that I’ve had the pleasure of riding for a while now. It has amazing power, great looks, and awesome range. If you’re looking for a great fat-tire ebike that offers a lot for the price, the Troxus Explorer Step-Thru is definitely one for you to consider. Check out my Troxus Explorer Step-Thru Review.

- Hovsco HovBeta Ebike – The HovBeta is a folding ebike with great specs and a lot of interesting features, and importantly, it’s sold at a good price point. I’ve had a blast commuting with it and using it to do deliveries with DoorDash, Uber Eats, and Grubhub. Check out my Hovsco HovBeta Ebike Review.

- Vanpowers Manidae Ebike – The Vanpowers Manidae is a fat tire ebike that I’ve been riding as my primary winter commuting bike and have also been using it to do food delivery with apps like DoorDash, Uber Eats, and Grubhub. After clocking in a decent number of miles with this ebike, I wanted to write a post sharing what my experience with the Vanpowers Manidae ebike has been like. Check out my Vanpowers Manidae Review.

- Sohamo S3 Step-Thru Folding EBike Review – A Great Value Folding Ebike – The Sohamo S3 Step-Thru Folding Ebike is an entry-level folding ebike that offers a lot of value for the price point. I’ve been riding the Sohamo S3 for a while now, putting the bike through its paces, and I have to say, this bike has exceeded all of my expectations. Check out my Sohamo Review.

- KBO Flip Ebike – The KBO Flip is an excellent bike. I’ve had a great time riding it and think it’s a versatile bike that can be used for a lot of purposes and can fit a variety of lifestyles. It’s worked out great for me as a general commuter bike and as a food delivery bike. Check out my KBO Flip Review.

- Hiboy P7 Commuter Ebike – The Hiboy P7 is an excellent electric commuter bike that’s offered at an affordable price point. The range and speed of this bike are both very good, so you won’t have any trouble getting anywhere you need to go with it. As a food delivery vehicle, this is also good – with how much range it offers, you’ll be able to work all day on a single charge. Check out my Hiboy P7 Commuter Electric Bike Review.

- Himiway Escape Ebike – The Himiway Escape is an interesting bike for anyone looking for a moped-style ebike. If you’re a gig economy worker, the Himiway Escape is particularly interesting and it’s possible to think of it as an investment, especially if you can opt to do deliveries with the Himiway versus using a car. It’s not cheap, but you can definitely make your money back when you compare the mileage you’ll put on your car versus using an ebike. Check out my Himiway Escape Bike Review.

- Espin Sport Ebike – The Espin Sport is a good ebike for someone who is looking for an ebike that feels and rides more like a regular bike. There are many ebikes that are really only bikes in name. In reality, they’re basically electric mopeds. The Espin Sport, by contrast, is a bike you could probably ride without the battery and you’d feel like you’re just riding a regular bike. Check out my Espin Sport Review.

- Varla Eagle One Scooter – The Varla Eagle One is an excellent scooter that can make sense for a lot of people. It can work as a primary mode of transportation. You can use it to work on gig economy apps like DoorDash, Uber Eats, and Grubhub. And it can also be a recreational vehicle if you’d prefer to use it for that. Check out my Varla Eagle One Review.

- Varla Falcon Scooter – The Varla Falcon is an excellent scooter that offers a good amount of power at a lower price point compared to more powerful scooters. It’s not exactly an entry-level scooter, nor is it a high-powered scooter. I think it fits somewhere in-between those two categories – an intermediate scooter if I had to give it a category. Check out my Varla Falcon Review.

- Hiboy S2 Scooter – The Hiboy S2 is an excellent entry-level commuter scooter that's perfect for someone looking to save some money in transportation costs and improve their commute. Check out my Hiboy S2 Review.

- Hiboy S2R Scooter – The Hiboy S2R is one of the more interesting electric scooters I’ve been able to test out. It’s not a high-powered scooter, but for an everyday transport option, it’s very useful, especially given some of the unique features that it has. Indeed, for the price, the Hiboy S2R might be the best value scooter I’ve used. Check out my Hiboy S2R Review.

- Fucare H3 Scooter – The Fucare H3 is a fun scooter and I’ve enjoyed testing it out. For a daily commuter or quick trips or errands, the Fucare H3 is probably the scooter I’ll use. It’s portable and easy to maneuver, so it’s just easier to take on the road when I need it. Check out my Fucare H3 Scooter Review.

More Recommended Investing App Bonuses

For additional investing app bonuses, be sure to check out the ones below:

- M1 Finance ($75) – This is a great robo-advisor that has no fees and allows you to create a customized portfolio based on your risk tolerance. You also get $75 for opening an account. Check out my M1 Finance Referral Bonus – Step-By-Step Guide.

- SoFi Invest ($25) – SoFi Invest is an easy brokerage account bonus that you can earn with just a few minutes of work. Use my SoFi Invest referral link, fund your SoFi Invest brokerage account with just $10 and you’ll get $25 of free stock. I also have a step-by-step guide for the SoFi Invest referral bonus.

- Robinhood (1 free stock) – Robinhood gives you a free stock valued between $2.50-$225 if you open an account using my referral link.

- Public (1 free stock) - Public gives you a free stock valued between $3-$70 if you open an account using my referral link.

More Recommended Bank Account Bonuses

If you’re looking for more easy bank bonuses, check out the below options. These bonuses are all easy to earn and have no fees or minimum balance requirements to worry about.

- Ally Bank ($100) – Of all the banks out there, Ally is, without a doubt, my favorite. At the moment, Ally is offering $100 to customers who open an eligible Ally account and meet the requirements. Here are the step-by-step directions to earn your Ally Bank referral bonus.

- Chime ($100) - Chime is a free bank account that offers a referral bonus if you use a referral link and complete a direct deposit of $200 or more. In practice, any ACH transfer into this account triggers the bonus. This bonus is easy to earn and posts instantly, so you’ll know if you met the requirements as soon as you move money into the account. I wrote a step-by-step guide on how to earn your Chime referral bonus that I recommend you check out.

- US Bank Business ($400/$1200) – This is a fairly easy bank bonus to earn, since there are no direct deposit requirements. In addition, you can open the Silver Business Checking account, which comes with no monthly fees. Check out how to earn this big bonus here.

- Current ($50) – Current is a free fintech bank that’s offering new users a $50 referral bonus after signing up for an account using a referral link. Current is an easy bonus to earn and also gives you access to three savings accounts that pay you 4% interest on up to $2,000. That means you can put away up to $6,000 earning 4% interest. That’s very good and makes Current an account I recommend to everyone. Check out my step-by-step guide on how to earn your Current Bank bonus.

- Novo Bank ($40) - Novo bank is a free business checking account that’s currently offering a $40 bonus if you open a Novo business checking account using a referral link. In addition to being a good bank bonus, Novo is also a good business checking account. It has no monthly fees or minimum balance requirements and operates a good app and website. Indeed, it’s the business checking account I currently use for this blog. Check out my post on how to easily open a Novo account.

- Varo ($25) – Varo is a free fintech banking app similar to Chime or Current. It’s currently offering a $25 bonus to new users that open a new Varo account with a referral link. The bonus for this bank is very easy to meet, all you need to do is spend $20 within 30 days of opening your Varo account. Check out my step-by-step guide to learn how to earn this bonus.

Kevin is an attorney and the blogger behind Financial Panther, a blog about personal finance, travel hacking, and side hustling using the gig economy. He paid off $87,000 worth of student loans in just 2.5 years by choosing not to live like a big shot lawyer.

Kevin is passionate about earning money using the gig economy and you can see all the ways he makes extra income every month in his side hustle reports.

Kevin is also big on using the latest fintech apps to improve his finances. Some of Kevin's favorite fintech apps include:

- SoFi Money. A really good checking account with absolutely no fees. You'll get a $25 referral bonus if you open a SoFi Money account with a referral link, and an additional $300 if you complete a direct deposit.

- 5% Savings Accounts. I'm currently getting 5.24% interest on my savings through a company called Raisin. Opening a Raisin account takes minutes to complete, it's free, and all of your funds are FDIC-insured. I explain how it works, why I'm now using it to store my emergency fund and any other cash savings I have, and why I recommend everyone check it out in this review.

- US Bank Business. US Bank is currently offering new business customers a $400/$1200 signup bonus after opening a new account and meeting certain requirements.

- M1 Finance. This is a great robo-advisor that has no fees and allows you to create a customized portfolio based on your risk tolerance. You also get $75 for opening an account.

- Empower. One of best free apps you can use to monitor your portfolio and track your net worth. This is one of the apps I use to track my financial accounts.

Feel free to send Kevin a message here.

Great post. I have been using Betterment for about a year and love their interface and ease of use. It’s been a great way to get my Wife comfortable with investing as well. For the less financially savvy, staying at the robo-advisor level will serve them just fine. For those who want to eventually be more hands-on, robo-advisors may still have their place, if for no other reason than to have something to compare their own ETF or Index fund picking performance against once they’re comfortable with more “friction” (Great example!). I’ll be taking that next step myself within the next year. We’ll see if my own hand selected portfolio can outperform robo-advisors over the next 10+ years.

Part of the reason I started an account with Betterment was because I wasn’t too savvy about how to invest. Now that I’m a bit better with it, I might just move it all to Vanguard, but for now, the small fee isn’t too bad for me. At 0.25% management fee, plus 0.05% expense ratios (give or take), I’m basically paying 30 basis points for the ease and knowing that I have a fiduciary giving me a nice, diversified portfolio.

I think robo advising is probably the wave of the future and I’m sure some of the bread and butter financial advisors are going to get swept up. I’m pretty sure that high net worth people will always try to beat the market with a financial advisor that may or may not earn their keep.

But I do think they’ll continue to take massive market share.

Thanks for sharing!!!

I agree that Robo-Advisors will continue to grow over the years. They just make it so much easier to start investing. Getting over that initial start phase is really key.

Great points about friction, and how a little bit of resistance can delay you taking action for years. And as you rightly know, in personal finance time really is money.

So I totally agree with you that robo-advisors are a very effective way to get started i the stock (and bond) markets. It’s a wonderful tool for people who just want to set it and forget it.

Exactly right! Friction is what stops most people from taking that first step. I know it did that for me. I had an idea of what a Roth IRA was back in 2006 or 2007, yet I did nothing because I couldn’t figure out what I was doing and did’t really have anyone to teach me.

I think Robo Advisors are great because they make it so easy and a lot of them have great user experiences. I was a Betterment user for 2 years, but eventually decided to manage my own finances once I learned more about investing. But while I was using it for 2 years I loved it and still recommend it to new investors who want to take a hands off approach. Investing is not easy and it’s really easy to make bad decisions unless you read a lot and pay attention. Robo advisors simply mitigate that risk for often very low fees. The ONE thing that I thought that Betterment was missing was the ability to select your own funds – they only let you select your % allocation between stocks and bonds. If I could have selected more investments then I might have stay just for the UX experience and re-balancing. The whole Tax Loss Harvesting didn’t really add up when I ran my own numbers, but for some investors it will save you at least the amount of money that Betterment charges. FYI I don’t work for Betterment – just a previous user. I do not currently use a robo adviors but really think they are great for newer or hands off investors. Thanks for sharing FP.

Thanks Millennial Money! That’s really the main benefit with them, it just makes it much easier for your regular person to figure out investing. There’s no doubt, you can easily just recreate the asset allocations yourself, if you understand it. But if you have no idea what the word asset even means – like I was like not so long ago – then it’s just a completely foreign language. Tell someone to go invest in VTSMX or something and 99% of people won’t know what any of those words mean or how to do it. But tell someone to go open up an account at Betterment, Wealthfront, or Wisebanyan, and it’s basically as easy as opening up a bank account. If it costs a few basis points to do that, I think it’s worthwhile. I know it would have helped me out 10 years ago if something like Betterment had been around.

What!? Not everyone’s into money? We have a small taxable account open with a robo adviser – it’s so simple and easy to set up and forget. For those who are new to investing, or just don’t want to deal with it, this is a great option.

I know, I’m shocked too, but we are in a totally weird subculture that is really into this stuff. Most people don’t care at all about this stuff. I’d say 99% of the population can open up a bank account pretty easily. But that same percentage of people won’t know how to open up an investment account. That’s the big benefit of robos. Get people out there opening up investment accounts!

This is so great to go over. When we studied investing in school we would look at specific stocks, study their history, chart them, etc. In my classes, index funds never came up! I didn’t discover them until years later. Not just is this type of research and analysis not practical for most busy people, but there are so many stocks to choose from that it can be overwhelming. I agree that robos are a great option, not just because they tend to be low cost and easy, but are perfect for people that prefer not to interact with others or feel intimidated when having to ask for help on getting going with investing.

The fact that you studied investing in school is really out of the ordinary! I didn’t learn anything about investing during any of my time in school – and I was an econ major in undergrad…

Intimidating is a good word. Think about going to the gym. A lot people – myself included – hate going to the gym because it’s an intimidating place to be. You’ve got some big guy next to you who knows all the exercise moves lifting tons of weight. Then I’m there looking like a weakling. So rather than go to the gym, I’d just stay home.

It’s the same thing with investing. As easy as we make it sound, it really isn’t if you have no background in it, just like doing a bunch of exercises at the gym isn’t that easy if you have no background in lifting. It’s all about reducing those barriers to entry. The easier and less intimidating it is, the more likely people will do it!

Great post- I think robo’s are definitely great especially for people who are just starting to invest. Loved the spectrum chart!

Thanks Amber! That’s why I’m a big fan of robos. I think we forget that investing is easy for some of us because this is just what we think about all the time. It’s like someone else who’s good at cooking or running or anything else. They’re good at it because they do it alot.

But for some people, investing just isn’t all that easy. Anything we can do to make things easier and as simple as possible is a big benefit for anyone just starting out.

Glad you liked that chart. I had to hand write it, so my apologies for the crappy handwriting!

The Automatic Millionaire is one of my favorites as well! It was given to me right after I graduated college and set me off on the right foot financially.

I’m a big fan of robo advisors. I currently use Wealthfront, and have been really happy with it thus far. Even if you have some personal finance and investing knowledge, I don’t want to spend a lot of time researching the best funds, and coming up with the proper asset allocation between all the funds. Wealthfront does all that for me. Plus, I was intrigued by tax loss harvesting.

For me, robo advisors are the easiest and most efficient way to put my money to work for me. The ability to automate deposits into my account and have them automatically deployed according to my investment plan is a huge plus.

It sounds like you like the robo-advisor for the time saving aspect, and that’s great! I also have a small SEP IRA set up with Wealthfront. I chose that just because it was really easy to set up and I was trying to save a couple bucks in taxes last year, so needed to set one up right away before the tax deadline. Again, reduced friction is what made me set that up. If I had to call in or fill out a bunch of forms, I might have opted to just forget trying to save on taxes. Making things easy is what makes more people do something, and that’s awesome in my book.

I do like the robo – investing. The logic seems simple. Computers are smarter than I am. Use the “computer machine” and “them internets” to make money more better than I can! Go team!

The downside of this theory is that then it should be true for Predictive Policing software too. I feel like an idiot standing inside a 10 meter box for 30 minutes at a precise time of day because the computer told me to…yet crime went down. Sigh.

Our robot overlords will soon control all our aspects of our lives! But seriously, technology has really made financial stuff so much more accessible. You’d be surprised at just how confusing it is to set up a retirement or investment account on your own. Even if you tell someone to set up a Roth IRA with Vanguard, they won’t know what that means or how to do it without some help and background information. But something like Betterment, Wealthfront, or Wisebanyan just makes it so much easier (fyi – Wisebanyan is literally a free Robo-Advisor. No management fee at all).

I can see why the robo’s are successful, but I continue to be a shamelessly no-robo guy – I think most people would be better off with the old fashioned balanced fund which essentially does the same thing with less complicated Tax forms. 😀

I know you’re a no robo-guy and that’s totally cool! The reason I’m a big fan of robos is just in its ability to help people get started investing. I know that my entire financial life might have been different if I had a robo to show me the way back in 2007. I think we’re just so into this personal finance world that we forget that 99% of people don’t know anything about this stuff and don’t want to spend their time trying to learn.

As an example, my buddy started up a Roth IRA a few years ago using Vanguard based on my recommendation. But he couldn’t figure out how to set it up. Putting money into a Vanguard Total Stock Market fund is second nature to us. But to a regular person, it doesn’t mean anything. This is the person that benefits from a robo. It makes it as easy as setting up a bank account basically.