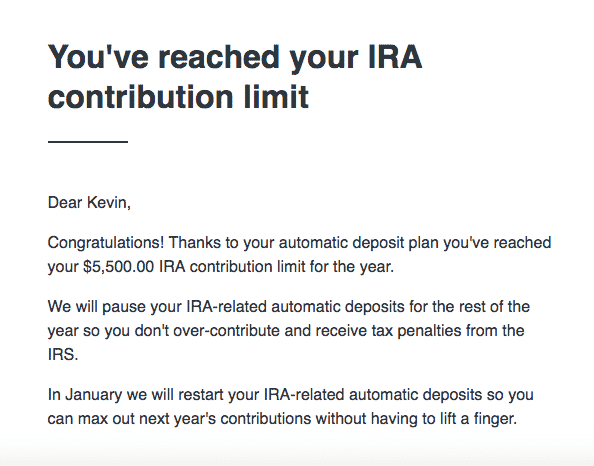

A few days ago, I received an email from Betterment notifying me that I had maxed out my Roth IRA for the year. It marks the third year in a row that I’ve maxed out my Roth IRA. Maxing out my Roth IRA might not seem like all that big a deal, but I think it is when you consider that three years ago, I didn’t even know what a Roth IRA was, let alone how to start or invest in one. At the time, the only investing I had done was a small, automatic contribution from my paycheck to my firm’s 401k – the default amount that my firm opted everyone into unless you specifically opted out.

Maxing out my Roth IRA might not seem like all that big a deal, but I think it is when you consider that three years ago, I didn’t even know what a Roth IRA was, let alone how to start or invest in one. At the time, the only investing I had done was a small, automatic contribution from my paycheck to my firm’s 401k – the default amount that my firm opted everyone into unless you specifically opted out.

When I did eventually get around to starting my Roth IRA, I went with the robo-advisor route. I chose to use Betterment since it had a low minimum contribution amount, the fees were reasonable and transparent, and the interface was straightforward and intuitive. Even though I had read that it was slightly more expensive to use a robo-advisor and every investing person online said I could do the same thing myself without the added fees, the ease of opening up a Roth IRA using a robo-advisor made it worth it. Plus, I found comfort in knowing that my contributions were being properly invested by a company that was also a fiduciary.

After three years and $16,500 in contributions, I’ve now outgrown my Betterment account (at least when it comes to my Roth IRA). While the 0.25% management fee that Betterment charges isn’t very high, I’ve learned enough about investing and have enough saved up that I don’t really need the robo-advisor element anymore. As a result, this year, I’ll be transferring all of my Roth IRA funds directly over to a Roth IRA with Vanguard. The move should cut my overall fees down from somewhere in the 0.35% range all the way down to 0.04%. It’s going to save me a lot of money over the long term.

Though I’ve outgrown my Betterment account, when new investors ask me where they should set up their Roth IRA, I still generally say to start with a robo-advisor – Betterment or Wealthfront, in particular. The way I see it, when it comes to a Roth IRA, start with Betterment or Wealthfront. Graduate to Vanguard later.

*Note: This post isn’t an advertisement for either Betterment or Wealthfront. Indeed, I haven’t even included any affiliate links in this post. I simply suggest these two because they’re both low cost, have low minimum deposit requirements, and allow you to transfer to another brokerage later down the line for free.

Start Your Roth IRA With A Robo-Advisor Like Betterment or Wealthfront

For a lot of us in the personal finance/financial independence community, investing seems pretty simple – invest in low-cost index funds that aim to match the market, save a huge percentage of our income, and let that money grow over time.

As easy as we like to think it is, the actual process of investing isn’t all that easy for the new investor. I know this because I was in that position once too. It took me a while to learn this stuff. And even now, a lot of you take for granted that you understood what I wrote in the previous paragraph. For someone like me three years ago, that previous paragraph might as well have been gibberish.

It’s this lack of knowledge that I think slows people down with investing. Just telling someone that they should open a Roth IRA or other retirement account isn’t enough. A retirement account isn’t like opening up a savings account, where you can simply open it and put money into it. There’s much more that can trip someone up along the way – questions like:

- Where do you open a Roth IRA?

- How do you put money into it?

- What happens once that money goes in?

- How do you invest it?

- How much do you need to invest?

- What does it cost?

Throw that list of questions in someone’s face and most likely, they’ll opt for the path of least resistance and do nothing at all. That’s why I’ve always been a huge fan of robo-advisors and why I started my investing life with one. They answer those questions for you. All I had to do was open an account, deposit money into it, and then the robo-advisor – Betterment in my case – did the rest for me.

Move Your Roth IRA Directly Into Vanguard After A Few Years

What makes the robo-advisor route so helpful for new investors is that it can get you started without a lot of costs.

Let’s look at management fees. Management fees are the main problem most people have with going the robo-advisor route. Betterment and Wealthfront both charge a 0.25% management fee, which isn’t that big of a deal if it means you can get started investing sooner and have comfort in knowing that you’re investing correctly.

The other fees to consider are closing or transfer fees. One issue with opening a brokerage account and then moving to another account is that you’ll often get charged fees to transfer your funds to another brokerage. That makes picking the right brokerage fairly important.

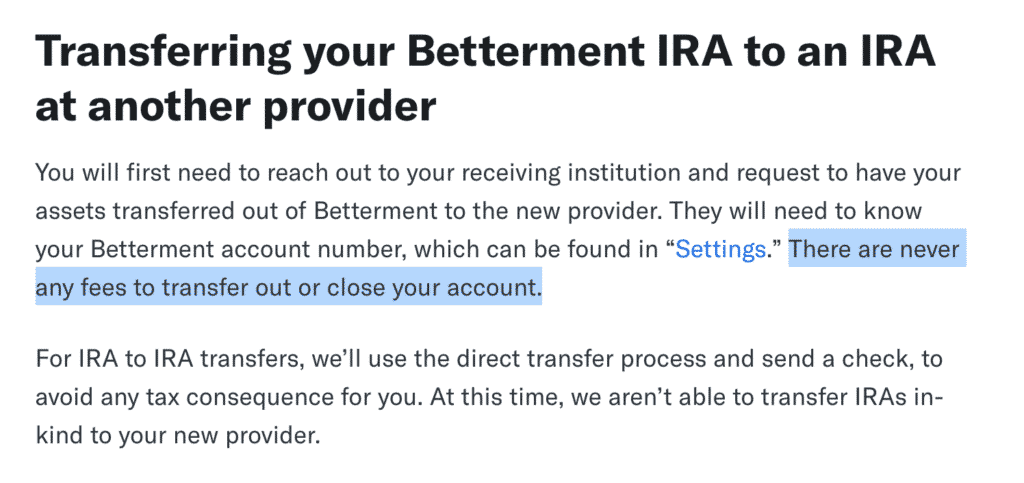

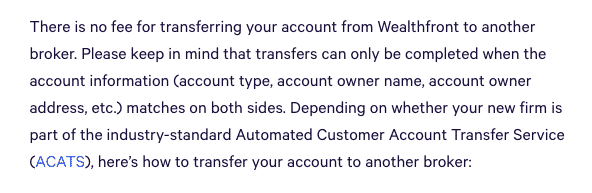

Robo-advisors, on the other hand, seem to be different. When I was looking to move my Roth IRA out of Betterment, I did a little research to see if I’d have to pay any fees to do so and was pleasantly surprised to see that there were absolutely no fees to move my money over to another company (see the below excerpt from Betterment’s FAQ):

Wealthfront has the same policy as well – no fees to transfer your account from Wealthfront over to another broker.

What this means for you is that it’s easy enough to start your Roth IRA with a robo-advisor first, just like I did. You’ll pay minimal management fees on a small amount of money. After a few years, you’ll have $10,000 or more saved up in your Roth IRA. At that point, you can just transfer it out and go with investing directly with Vanguard, if you want to do so.

Suggested Robo-Advisors To Start With

I’ve talked about Betterment and Wealthfront in this post and those two are both great robo-advisors that give you the flexibility to get started investing and move over to cheaper options later if it makes sense for you.

When I started my first Roth IRA, I opted to use Betterment because it was the robo-advisor that I was more familiar with and I preferred their interface more. I used Betterment for three years before moving my Roth IRA directly to Vanguard. Yes, I paid a 0.25% management fee for Betterment to manage my account. But it was worth it to me since I didn’t know much about what I was doing and it gave me comfort in knowing that I was investing correctly.

There are some other robo-advisors that are very good as well. One other option that’s worth talking about is M1 Finance. What makes M1 Finance particularly interesting is that it has robo-advisor features and charges no management fee at all. When you set up your Roth IRA, you can answer a few questions and pick a low-cost portfolio that’s appropriate for your situation. Basically, you can get the best of all worlds with an app like M1 Finance – a no-fee robo-advisor service and low-cost investing with no additional cost.

M1 Finance didn’t exist when I first set up my Roth IRA. If it had, maybe I would have opted to go with them over Betterment or Wealthfront. Note that, unlike Betterment or Wealthfront, M1 Finance does charge a fee if you want to transfer your account to another brokerage, so it loses a little bit of flexibility if you decide that you’d rather go directly to a company like Vanguard.

Robo-Advisor Fees Aren’t Forever

You’ll hear from a lot of experts who tell you that you can do all of the stuff that a robo-advisor does on your own for free – and they’re absolutely right. But doing it yourself naturally increases friction, which makes it harder to get started.

Instead, I think it’s better to get started right away with a robo-advisor, then move those funds to Vanguard once you’ve figured out what you’re doing and have a little bit of money saved up. Even if you pay some management fees to a robo-advisor on your Roth IRA, it doesn’t have to be forever. Sure, I paid three years’ worth of management fees to Betterment – three years where I could have figured out how to invest on my own and paid no fees at all. Three years, though, isn’t a ton of time in the grand scheme of things.

So, I’ll be doing two things this year when it comes to my Roth IRA. First, I’ll be moving my Roth IRA contributions directly into Vanguard. With three years of contributions and a long bull market, my Roth IRA is now standing at a little over $21,000 at the time I write this. I’ll likely be dumping it all into a Vanguard Total Stock Market Fund (VTSAX) just to keep things simple. Transferring my funds into Vanguard shouldn’t be difficult either – companies are always willing to help you get money to them, so it’ll just be a matter of opening up my Roth IRA and figuring out some directions.

The second thing I’ll be doing is opening up a Roth IRA for my wife and getting as much as we can into her Roth IRA for this upcoming year.

In a few years (possibly even this year), our income will be too high to directly contribute to a Roth IRA, at which point, we’ll have to start utilizing a backdoor Roth (a topic for another post).

Anyway, that’s the strategy I recommend for anyone starting their Roth IRA investing journey – go with a robo-advisor like Betterment or Wealthfront first, then move those funds into Vanguard later. It’s an easy way to get your investing life off to a good and easy start.

This post may contain affiliate links.

More Recommended Ebike/Scooters

Check out these other ebikes and scooters I've reviewed:

- Urban Arrow Ebike – Last year, I made one of the largest purchases I’ve ever made – I bought a $9,000 electric cargo bike from Urban Arrow. In my Urban Arrow review, I will discuss what it is and why I decided to buy this bike, as well as discuss how impactful a bike like this can be on your journey to financial independence.

- Troxus Explorer Step-Thru Ebike – The Troxus Explorer Step-Thru is a fat-tire ebike that I’ve had the pleasure of riding for a while now. It has amazing power, great looks, and awesome range. If you’re looking for a great fat-tire ebike that offers a lot for the price, the Troxus Explorer Step-Thru is definitely one for you to consider. Check out my Troxus Explorer Step-Thru Review.

- Hovsco HovBeta Ebike – The HovBeta is a folding ebike with great specs and a lot of interesting features, and importantly, it’s sold at a good price point. I’ve had a blast commuting with it and using it to do deliveries with DoorDash, Uber Eats, and Grubhub. Check out my Hovsco HovBeta Ebike Review.

- Vanpowers Manidae Ebike – The Vanpowers Manidae is a fat tire ebike that I’ve been riding as my primary winter commuting bike and have also been using it to do food delivery with apps like DoorDash, Uber Eats, and Grubhub. After clocking in a decent number of miles with this ebike, I wanted to write a post sharing what my experience with the Vanpowers Manidae ebike has been like. Check out my Vanpowers Manidae Review.

- Sohamo S3 Step-Thru Folding EBike Review – A Great Value Folding Ebike – The Sohamo S3 Step-Thru Folding Ebike is an entry-level folding ebike that offers a lot of value for the price point. I’ve been riding the Sohamo S3 for a while now, putting the bike through its paces, and I have to say, this bike has exceeded all of my expectations. Check out my Sohamo Review.

- KBO Flip Ebike – The KBO Flip is an excellent bike. I’ve had a great time riding it and think it’s a versatile bike that can be used for a lot of purposes and can fit a variety of lifestyles. It’s worked out great for me as a general commuter bike and as a food delivery bike. Check out my KBO Flip Review.

- Hiboy P7 Commuter Ebike – The Hiboy P7 is an excellent electric commuter bike that’s offered at an affordable price point. The range and speed of this bike are both very good, so you won’t have any trouble getting anywhere you need to go with it. As a food delivery vehicle, this is also good – with how much range it offers, you’ll be able to work all day on a single charge. Check out my Hiboy P7 Commuter Electric Bike Review.

- Himiway Escape Ebike – The Himiway Escape is an interesting bike for anyone looking for a moped-style ebike. If you’re a gig economy worker, the Himiway Escape is particularly interesting and it’s possible to think of it as an investment, especially if you can opt to do deliveries with the Himiway versus using a car. It’s not cheap, but you can definitely make your money back when you compare the mileage you’ll put on your car versus using an ebike. Check out my Himiway Escape Bike Review.

- Espin Sport Ebike – The Espin Sport is a good ebike for someone who is looking for an ebike that feels and rides more like a regular bike. There are many ebikes that are really only bikes in name. In reality, they’re basically electric mopeds. The Espin Sport, by contrast, is a bike you could probably ride without the battery and you’d feel like you’re just riding a regular bike. Check out my Espin Sport Review.

- Varla Eagle One Scooter – The Varla Eagle One is an excellent scooter that can make sense for a lot of people. It can work as a primary mode of transportation. You can use it to work on gig economy apps like DoorDash, Uber Eats, and Grubhub. And it can also be a recreational vehicle if you’d prefer to use it for that. Check out my Varla Eagle One Review.

- Varla Falcon Scooter – The Varla Falcon is an excellent scooter that offers a good amount of power at a lower price point compared to more powerful scooters. It’s not exactly an entry-level scooter, nor is it a high-powered scooter. I think it fits somewhere in-between those two categories – an intermediate scooter if I had to give it a category. Check out my Varla Falcon Review.

- Hiboy S2 Scooter – The Hiboy S2 is an excellent entry-level commuter scooter that's perfect for someone looking to save some money in transportation costs and improve their commute. Check out my Hiboy S2 Review.

- Hiboy S2R Scooter – The Hiboy S2R is one of the more interesting electric scooters I’ve been able to test out. It’s not a high-powered scooter, but for an everyday transport option, it’s very useful, especially given some of the unique features that it has. Indeed, for the price, the Hiboy S2R might be the best value scooter I’ve used. Check out my Hiboy S2R Review.

- Fucare H3 Scooter – The Fucare H3 is a fun scooter and I’ve enjoyed testing it out. For a daily commuter or quick trips or errands, the Fucare H3 is probably the scooter I’ll use. It’s portable and easy to maneuver, so it’s just easier to take on the road when I need it. Check out my Fucare H3 Scooter Review.

More Recommended Investing App Bonuses

For additional investing app bonuses, be sure to check out the ones below:

- M1 Finance ($75) – This is a great robo-advisor that has no fees and allows you to create a customized portfolio based on your risk tolerance. You also get $75 for opening an account. Check out my M1 Finance Referral Bonus – Step-By-Step Guide.

- SoFi Invest ($25) – SoFi Invest is an easy brokerage account bonus that you can earn with just a few minutes of work. Use my SoFi Invest referral link, fund your SoFi Invest brokerage account with just $10 and you’ll get $25 of free stock. I also have a step-by-step guide for the SoFi Invest referral bonus.

- Robinhood (1 free stock) – Robinhood gives you a free stock valued between $2.50-$225 if you open an account using my referral link.

- Public (1 free stock) - Public gives you a free stock valued between $3-$70 if you open an account using my referral link.

More Recommended Bank Account Bonuses

If you’re looking for more easy bank bonuses, check out the below options. These bonuses are all easy to earn and have no fees or minimum balance requirements to worry about.

- Ally Bank ($100) – Of all the banks out there, Ally is, without a doubt, my favorite. At the moment, Ally is offering $100 to customers who open an eligible Ally account and meet the requirements. Here are the step-by-step directions to earn your Ally Bank referral bonus.

- Chime ($100) - Chime is a free bank account that offers a referral bonus if you use a referral link and complete a direct deposit of $200 or more. In practice, any ACH transfer into this account triggers the bonus. This bonus is easy to earn and posts instantly, so you’ll know if you met the requirements as soon as you move money into the account. I wrote a step-by-step guide on how to earn your Chime referral bonus that I recommend you check out.

- US Bank Business ($400/$1200) – This is a fairly easy bank bonus to earn, since there are no direct deposit requirements. In addition, you can open the Silver Business Checking account, which comes with no monthly fees. Check out how to earn this big bonus here.

- Current ($50) – Current is a free fintech bank that’s offering new users a $50 referral bonus after signing up for an account using a referral link. Current is an easy bonus to earn and also gives you access to three savings accounts that pay you 4% interest on up to $2,000. That means you can put away up to $6,000 earning 4% interest. That’s very good and makes Current an account I recommend to everyone. Check out my step-by-step guide on how to earn your Current Bank bonus.

- Novo Bank ($40) - Novo bank is a free business checking account that’s currently offering a $40 bonus if you open a Novo business checking account using a referral link. In addition to being a good bank bonus, Novo is also a good business checking account. It has no monthly fees or minimum balance requirements and operates a good app and website. Indeed, it’s the business checking account I currently use for this blog. Check out my post on how to easily open a Novo account.

- Varo ($25) – Varo is a free fintech banking app similar to Chime or Current. It’s currently offering a $25 bonus to new users that open a new Varo account with a referral link. The bonus for this bank is very easy to meet, all you need to do is spend $20 within 30 days of opening your Varo account. Check out my step-by-step guide to learn how to earn this bonus.

Kevin is an attorney and the blogger behind Financial Panther, a blog about personal finance, travel hacking, and side hustling using the gig economy. He paid off $87,000 worth of student loans in just 2.5 years by choosing not to live like a big shot lawyer.

Kevin is passionate about earning money using the gig economy and you can see all the ways he makes extra income every month in his side hustle reports.

Kevin is also big on using the latest fintech apps to improve his finances. Some of Kevin's favorite fintech apps include:

- SoFi Money. A really good checking account with absolutely no fees. You'll get a $25 referral bonus if you open a SoFi Money account with a referral link, and an additional $300 if you complete a direct deposit.

- 5% Savings Accounts. I'm currently getting 5.24% interest on my savings through a company called Raisin. Opening a Raisin account takes minutes to complete, it's free, and all of your funds are FDIC-insured. I explain how it works, why I'm now using it to store my emergency fund and any other cash savings I have, and why I recommend everyone check it out in this review.

- US Bank Business. US Bank is currently offering new business customers a $400/$1200 signup bonus after opening a new account and meeting certain requirements.

- M1 Finance. This is a great robo-advisor that has no fees and allows you to create a customized portfolio based on your risk tolerance. You also get $75 for opening an account.

- Empower. One of best free apps you can use to monitor your portfolio and track your net worth. This is one of the apps I use to track my financial accounts.

Feel free to send Kevin a message here.

I want to transfer my Roth IRA from Wealthfront to Vanguard but the Wealthfront website says:

“Keep in mind that if you’re moving an IRA, Wealthfront will automatically liquidate all of your holdings.”

So does this mean that they need to see and then the cash gets moved over to Vanguard to be reinvested?

If so, is this how it aways is? Why can’t the shares just transfer over. I hate the idea of selling and then repurchasing these funds at current prices. I don’t like that. Any suggestions? Thanks.

If you’re moving a Roth IRA, then it doesn’t matter if you sell it and then rebuy it again. There’ll only be a few days of lag.

Remember, even though you’re buying at today’s prices, you’re selling at today’s prices too. There’s no difference.

Example = If you bought it at $50 and sold today at $100, you have $50 of profit. Then if you buy at $100, you’re exactly at the same place you were before, assuming you’re doing this in a tax-advantaged account.

This was a great article. Another source that helped me start investing was Julie Jason’s book ‘Retire Securely.’ She really breaks down hot to set up your own buying and selling rules, and goes over how to go over down markets. I encourage you all to check it out!

https://juliejason.com/books/retire-securely

For almost a year now, I’ve been debating on whether to just use Schwab or Vanguard, instead of Wealthfront and Betterment. Thanks for you guidance, I finally ended my analysis-paralysis. I signed up with Wealthfront and my account is officially deposited today.

PS. I used your brother’s link so he should have gotten the reward too.

Congrats! Glad you got yourself started. Really, you can’t go wrong at least starting with one of these roboadvisors, then figuring things out later.

I’m planning to start investing with Wealthfront after the holidays. I couldn’t quite tell from the comments. Does you still have the referral link option for the first $5000 managed?

Hey Liz, to be honest, I’m not sure if my Wealthfront still gives the 5k managed for free. They changed things up a while ago.

Wealthfront does still offer the $5k via email invite for both the inviter and invitee. If you’d like an invite code, just let me know 🙂 Or Financial Panther can provide it.

My brother’s Wealthfront link is here if anyone wants to use it.

https://www.wealthfront.com/invited/AFFA-GVQU-MALI-SFUI

So I think this is no longer true for wealthfront?

The management fee is 0.25% but is waived for the first $10,000, which makes it pretty perfect for starting out your Roth IRA.

Yeah, I wrote this post in 2018 and I think right when I wrote this post, they changed it up. Still, wealthfront is fine for starting your Roth IRA with because fees are low and you can transfer direct to vanguard for free still.

By no fees with Vanguard, do you mean after the initial trade fees for each fund? I mean it does cost you something right? And then if you ever make a change, you’ll pay per trade for that too. Or am I confused? Thanks for your reply.

Vanguard charges expense ratio, which is the annual fee you pay each year. I think the current fee on a total market index fund like VTSAX is 0.4%. They don’t charge any fees to buy or sell.

I’ve got a question that I cannot find on the web.

Can a Roth be worth it if you can only invest the max for three years and let it ride for ten years. Due to no earned income (retirement)

it wouldn’t be contributed to after three years.

What could be expected for a return after ten years.

Thank you for your time.

Hey Jim. The question really is, what are your alternatives. If you’re not doing anything with it, then yeah, you should invest it. 18k over 10 years at 7% rate of return is 35k. It’s not a lot, but it’s double what you put in. Growth comes from big numbers though, not from small numbers.

Also, why not just earn some income so you can keep contributing? 6k per year is $500 per month. That requires you to make about $16 or $17 per day. I’m fairly certain anyone can figure out a way to make 16 or 17 bucks per day.

Be mindful of wash sales when not doing all your (and your spouse’s) investments at one single robo advisor!

Good point. Luckily, if you’re just starting out investing and using it for a tax-advantaged account, no need to worry about any of that.

PoF featured one of your posts and after reading it I came to your blog to peruse your thoughts. So, this response is a few months time late, but I have to say your approach here makes little sense to me. It probably won’t hurt anything to start a Roth this way, but why introduce the complexity? Open a Roth at Vanguard, set up automatic payments to invest in one of the low cost target retirement funds (that take care of asset allocation over time) and forget about it. Hard to make investing any easier than that. I’m curious, what advantage do you see to starting with one of the wealth advisors? I get that you can do it, I just don’t get why anyone would want to, especially if the end game is to get to Vanguard within a few years anyway.

Hey Larry, it’s a fair question – I had a debate in a lawyer chatroom with my buddy BigLaw Investor (and others in the room) about this exact topic. Some agreed with my approach. Others thought going straight to Vanguard and doing a Target Date fund made sense.

Here’s my rationale. I think roboinvestors are great places to start off with a Roth because the vast majority of people have absolutely no idea how to start investing. We’re all in this investing world so much that we take it for granted just how much of an understanding we have. Go to 99% of people out there (and go to 100% of college kids probably) and none of them will know what a mutual fund is or anything really).

Here’s my own history. 10 years ago when I was in college, roboinvestors didn’t exist. I had read about Roth IRAs from reading automatic millionaire, so I thought, I’ll start one of those up since I was saving some money and I thought it made sense to try to save for retirement like the book said. I ended up opening an account with etrade, and then…I had no idea what to do after that. Since I didn’t know what to do, I did like what most people do, I gave up, then didn’t start investing until 8 years later!

One thing I could do though was save money in a bank account. And the advantage of roboadvisors is that its basically the closest thing you can get to a bank like savings account experience with investments – move money into a Betterment or Wealthfront account and then that’s all you have to do.

If you go and tell most people (even smart, educated people) to go start up a Roth IRA and invest it all into VTSAX or a Vanguard Target Date fund – that’s basically assuming people understand those words.

I don’t hang around dumb people. But if you told my wife to go open a Roth IRA right now, she would not be able to do it. I would literally have to sit there with her and do it for her. And she’s a dentist that’s gone through 5 years of college and 8 years of post-college schooling. She knows a lot about teeth, but she doesn’t know anything about investing. But if I tell her to go to Wealthfront and open a Roth IRA there, she knows exactly how to do that.

My brother was the same way. With no idea how to do a Roth IRA (or how to invest for that matter), you know what he did – he walked into his bank branch and had them open up a Roth IRA for him. Yeah, that’s not doing so good…

Obviously, this approach isn’t for someone who knows what they are doing. It’s why I wrote this post. It’s for someone like me to get started, then reassess down the line later. Because, they can stay with the roboadvisor too. What’s important is that they got started until they’ve either learned more about investing (like me) or they don’t know anything and just stay the course where they are.

I started off my Roth IRA with Betterment because I didn’t know how to invest and couldn’t understand how to even do anything. Even my Solo 401k, which at that point I did know what I was doing, took work to figure out how to buy something (it’s not intuitive at all). If I had trouble understanding how to use it, how would a regular person be able to figure it out?

These roboadvisors charge 25 basis points for their service. We all pay extra for services, that’s why we would be okay with some people paying extra for target date funds, even though you could do the same thing at a lower cost yourself. In my opinion, 25 basis points is not going to be the reason someone doesn’t hit FI.

Anyway, that’s my thought. There are fair criticisms. I think that a lot of us just underestimate that, while investing is simple, it really isn’t for most people. So the more “bank like” you can make investing seem, the better. If Vanguard or Fidelity would literally let you open up a Roth IRA, put in money, and then automatically put it into the right spot for you, that would change this whole thing up.

Yo Financial Panther! I definitely see the advantage in “retiring” from the robo-advisor and going straight to the Vanguard account. It is really hard to beat that .04%! Did you look into any of these now free robo-advisor apps? Like M1 or Robinhood? I like M1, and I honestly haven’t done much research into Robinhood so I’m not sure if you can even buy Vanguard ETFs with it. Anyway, for someone like yourself, you can definitely do better getting round that fee since you are a sophisticated investor.

I’ve never looked at M1 before, so not sure how they work. Robinhood is not a roboadvisor – it’s a brokerage basically that lets you buy and sell for free. You could, if you wanted to, buy Vanguard ETFs through Robinhood, but I’m actually not sure if Robinhood lets you set up tax-advantaged accounts or not.

Kevin, do you think you could do a blog post detailing step-by-step on how to use the Vanguard website to invest in their mutual funds and/or ETFs? I think that’d be incredibly beneficial.

That’s a great idea. I have a post planned on the process of rolling over my Betterment account to Vanguard, so I could probably just add that as well.

Great post!

I took your sage advice and opened up a Roth IRA with Wealthfront. However, I didn’t know until recently that since it’s before April 15, I could put in the $5,500 max contribution for 2017, and then $5,500 more for 2018. If I do them simultaneously, it puts me over the $10K limit almost immediately, so am I better off transferring these funds to a Vanguard and nixing the Robo-Advisor completely? If not, how long should I plan on leaving the ~$11,000 in Wealthfront for?

If you’ve got the cash already to do that, then you could just ignore the robo-advisor route and just go straight to Vanguard. It’s not a big deal either way. Just get started is the most important thing.

I think Wealthfront is doing away with the first $5,000 managed free (grandfathering existing accounts), but keeping the 5k free for each referral. I love WF – yes, I could do it myself, but I wouldn’t. And the thousands I’ve banked in tax loss harvesting feels like free money.

Yep, I saw that email too noting that Wealthfront was getting rid of the first 5k for free. Luckily, we got grandfathered in for my wife, so she’s got something like $20k managed for free, which should take her about 4 years to get to that point for a Roth IRA.

I love this strategy, and it’s worth noting that it should only cost ~$62 over the first three years if you’re steadily contributing towards maxing a Roth IRA each year

For math nerds: this is calculated based on avg balance of 5500/2= 2750 year one, 5500+2750=8250 year two, 11000+2750=13750, and a 25bps fee

Thanks for doing that math Graham! $62 bucks for 3 years just so you can get your Roth IRA started, then switching over to Vanguard. That is well worth it. Seriously, if robo-advisors had existed for me back when I was 20 years old, things would have been SO MUCH different.

I did this exact same thing. Started out at Betterment and moved it over to Vanguard as I learned more!

I’ve done a few rollovers with Vanguard and they are amazing. I took an old 401K and rolled it into a roth IRA and they not only helped me through the whole thing, but they told me to pay the tax out of pocket to avoid the penalties. Good luck, but you most likely won’t have any problems moving your money.

Yep, not expecting any issues at all! Any reason you rolled over the 401k into a Roth? I’m guessing you were in a low tax-bracket and it wasn’t a huge 401k?

At the time, I only had a Roth IRA account and the old 401K was less than $5K. I just wanted it all in one account and the taxes weren’t going to break the bank. I ended up just taking a smaller refund that year and I simplified everything by having it in one account.

That makes sense! I likely would have done the same thing, especially since you were getting a tax refund too.

Wow, this was exactly my plan. I am new to the investment game so I opened up my first Roth account with Betterment two months ago!

Thats perfect man! Now just keep doing regular contributions and in a few years, reassess if you still want or need the robo-service/interface. It’ll take you some time before you have significant money in there anyway. And don’t get scared off by the market fluctuations!

I’m also considering doing the reverse. Have a long standing account w/ Vanguard, but I’m so happy with the Wealthfront service that I might be moving a chunk of that over to Wealthfront. I’m not crazy about some of Vanguard’s user interface and reporting on their website. I had ended a long standing account I had with American Century because their technology offerings, in the form of their site, simply was not keeping up with the times. That’s a BIG selling point with me, and Wealthfront seems to be doing it right and tweaking it all the time. Good post. Congrats on maxing out your contribution!

I know – the tech thing is what these robos are doing so well. My buddy initially set up a Roth IRA with Vanguard and couldn’t figure out what the heck he was doing (smart, tech-savvy, brand new investor, didn’t know how to invest his money). I ended up just telling him to open a Wealthfront account so he could just put it in and walk away. The robo interface made it much easier for him.

Are you able to use Vanguard with Chrome? I constantly get the blank gray screen of death and have to remember to use FireFox just for Vanguard — ugh.

Thanks Kevin. I actually did the opposite, I started my IRA with Vanguard and so far so good. I did; however, set my taxable account at Betterment and I’ve been happy with their service. When I started their fee was 0.15 basis points and they’ve increased to 0.25 which isn’t terrible but still hurts compared to a 0.04% of a Vanguard fund. Tax loss harvesting as a service has added value to my situation but I can appreciate how inmaterial this can be depending on the invested amount. I’ve been recently thinking about moving my taxable accounts to Vanguard but I was unsure about the tax implications. Per your post it appears it was something that could be done without triggering a tax event but I’m not sure about that. I have funds that are not only Vanguard funds at Betterment so if they were to transfer my money to Vanguard I assume they would have to sell the non-Vanguard assets hand me a check and then transfer the Vanguard funds. This is something that I plan to invertiste for sure. Thanks for the post and overall agree with you… the most important thing is to get started and If going with Vanguard seems intimidating then start with a robo. The two you have mentioned are pretty good and I would be tempted to say that Wealthfront might have a slight advantage because they manage the first $15K of your money for free (if they still have this promo)

I do see a value with robos for taxable accounts with the tax-loss harvesting, although, as you mentioned, you need to have a real amount of money invested before it makes a difference.

Having it in taxable does make it problematic since you’ve got to worry about taxable events. It looks like Vanguard funds could be transfered in-kind to Vanguard in full shares, but then you’ll have to use ETFs for your Vanguard account, which you might or might not want to do (more of a hassle to use ETFs unless it lets you buy partial shares of ETFs).

Let me know what you end up doing with that taxable account. I’d personally probably just leave it at Betterment. Maybe take advantage of that financial advisor service that they offer to get some more return on your fee too?

I do think that when doing this Roth IRA to Vanguard strategy, Wealthfront is probably the way to go. You can basically start out doing Wealthfront for free, then make your decision down the line, then move onto directly with Vanguard later if you want. That’s the nice thing about the tax-advantaged account – don’t have to worry about the taxable event issue, which makes the robo-advisor route to start even better.

When you started your IRA with Vanguard, did you buy ETFs or did you wait until you had enough saved so you could invest into a fund?

I started a mutual fund with the investor version of VTSAX and then my 2nd year I had enough to switch to VTSAX. I think for the investor the minimum is $3000 and admiral is $10K. If you don’t have the money yeah I would suggest starting with an ETF like VTI … I think this is the equivalent to VTSAX

I, too, started my Roth IRA using a robo advisor (Wealthfront) and will be switching it over to Vanguard in a year or two. Yay for easy-to-use robo advisors with the first $15k free. I will continue to use Wealthfront for my just-for-fun taxable account w/ tax loss harvesting and also opened a Small Business 401k in Vanguard. Investing is fun the more you learn. Thanks for your article. 🙂

I’m early retired and I still let three robo’s manage my accounts because I don’t like to do it. That is in spite of my helping manage a $60mm endowment fund for a charity I volunteer at. When it comes to my own money it is worth the management fees to not have to think about it and it is an affordable cost in my budget just like my CPA. I feel like at some point I might take over the management of my portfolio but right now it is a luxury I choose to pay for.

Very interesting! It always seems like the Bogleheads and other people who know what they’re doing with investing recommend against robo-advisors simply because of the fees, so it’s good to see someone knowledgeable using them too. I’ve personally always thought the fees were perfectly reasonable and that they’re perfect for someone just starting out investing (college student, recent grad, etc).

I remember when I tried to start investing back in college (around 2007 or so). I set up an E-trade account and had no idea what I was doing – then gave up and stopped investing for 8 years. Honestly, my investing life might be totally different today if robo-advisors had existed back when I was in college. I might have started investing when I was 20, instead of 28. My whole thing with robos is they just help people get started, which is way better than doing nothing.

Do you use your robo-advisors just for taxable accounts or tax-advantaged accounts? (I’m guessing probably taxable accounts?). I can definitely see a benefit with robos for taxable accounts with the tax-loss harvesting.

Interested in this post though it’s a bit old – thanks for keeping comments open.

I’ve seen this kind of advice elsewhere – start robo and move on “when you figure things out.” For me that is the gap. What exactly should I be figuring out during my “robo years” and how do I go about doing that?

My robo balances are approaching higher fee balances, but I haven’t learned the secret lessons I was apparently supposed to. 😉

An interesting addendum for some may be blooom.com (and perhaps others) that lay investment automation similar to robo-advising on top of regular investment accounts, like Vanguard.

Interested in your thoughts.

The great thing is, you don’t need to move out of the robo so long as you’re using a robo that is charging relatively low fees (0.25% or less is what I aim for). The truth is, the people that that tell you that you need to move out of the robo are the type that are interested in investing and doing this stuff. If that’s not you, then going robo for your entire life is totally fine. Paying a 0.25% management fee is NOT going to be the reason someone doesn’t retire or hit their target numbers. The most important thing is just doing things relatively correctly -which is what robos do.

I used Blooom before as well for my 401k. I got no beef with them although back when I used them, they only charged $1 per month (now they’re charging $10 per month, which I think is pretty high – but again, that $10 per month won’t be the reason someone can’t retire, so go for Blooom if that’s what you need to invest and invest for the long term).