Something that often gets forgotten in the side hustling discussion is the impact of taxes. If you’re like most people, taxes are probably a thing that you don’t think about all that much. You get your paycheck, you file your taxes at the end of the year, and you probably end up with a tax refund most of the time.

In its base form, income that you earn from normal employment (W-2 income as its called) is pretty simple. You’re taxed on that income in essentially three ways:

- Federal Income Tax

- State Income Tax

- FICA Taxes (employee portion)

These taxes get taken directly out of your paycheck, which is helpful for you since it means that you don’t really have to do anything. You just get your money from your employer and you’re good to go.

Obviously, you’ll pay more or less in taxes depending on where you live. Some places have local taxes (I’m looking at you New York). Other places have no state income tax at all. But in general, federal, state, and the employee portion of FICA taxes are the three taxes that you’re going to be paying on your regular, W-2 income.

The landscape looks a bit different when you’re earning income from your side hustle, whether that’s from creating a business (like a blog) or working on a sharing economy/gig economy platform like Uber, Lyft, Postmates, Uber Eats, Rover, etc.

In this post, we’re going to take a closer look at the taxes you need to think about when you’re earning money from your side hustle. We’re also going to look at how these taxes can impact your earnings and what you can do to keep more of your side hustle earnings in your pocket.

How Independent Contractors Work

When you’re earning income on the side, you’re most likely going to be earning it in the form of 1099 income. Unlike W-2 income (where your employer takes out your taxes for you), 1099 income flows to you with no taxes taken out at all. That means you’re going to have to pay your taxes yourself.

I think the easiest way to think about your side hustle taxes is to imagine yourself as a little company. You’re both the CEO and the sole employee of your little business empire.

So, for example, my various side hustles look like this from an organizational standpoint:

- Owner/CEO/Boss = Financial Panther

- Employee/Minion/Janitor = Financial Panther

On the one hand, I’m the upper management in my little side hustle business – the C Suite executive, if you will. And I’m also the lowest rung worker in my business of me.

Take my Postmates gig as an example. When I’m out doing my lowly delivery man duties on Postmates, I’m both the CEO of my own little delivery business and the only employee of that same business. It’s kind of weird to think about it that way, but that’s basically how being an independent contractor works.

The Different Taxes You Pay When You’re Side Hustling

Now we come to the dreaded thing that everyone hates – taxes. When you’re side hustling on top of your day job, the taxes you pay on your side hustle income matter A LOT. That’s because your side hustle income will be your highest taxed income.

Let’s look at why that is. Below is a list of the different taxes you’ll pay on your typical side hustle income:

- Federal Income Tax (at your highest, marginal tax rate)

- State Income Tax (at your highest, marginal tax rate)

- FICA Taxes (employer portion)

- FICA Taxes (employee portion)

You might wonder why I say that your side hustle earnings are taxed at your highest marginal tax rate. The reason has to do with the fact that, if it’s a side hustle, then by definition, it should be money that you are earning outside of your day job and, importantly, that you don’t need in order to survive (hence, why it’s called a side hustle). If you actually need your side hustle income in order to survive, it’s not really a side hustle – it’s basically just a second job.

If we make the assumption that your side hustle income is money that you don’t actually need to live, that means we can consider it bonus money and can think of it as the last dollars you earn in any given year. Remember, if you don’t need that money to survive, you could have opted not to earn it and paid no taxes at all.

The other thing you’ll probably notice is the employer portion of your FICA taxes. Like I pointed out before, when you’re running your own little business, you’re both the CEO and the only employee of your little company. Since you’re playing both roles, you’re responsible for paying the other half of FICA that your employer normally pays for you.

How Much In Taxes Are You Paying?

With that background out of the way, let’s go through an example to help you understand how much tax you’re paying on your side hustle income.

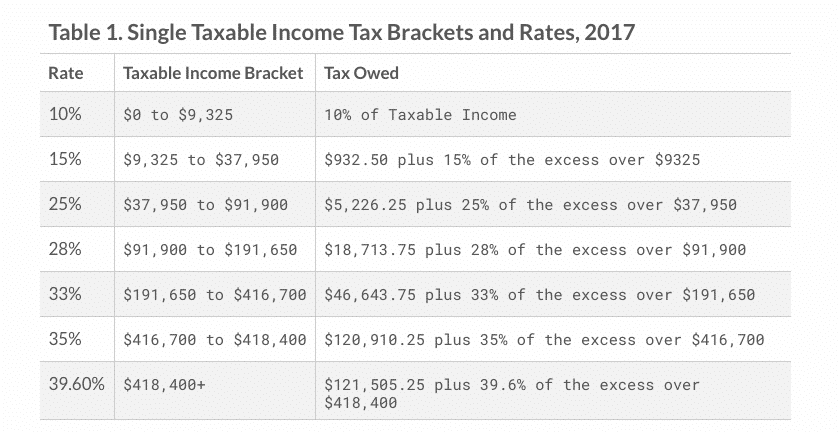

Let’s say you make a nice round, $100,000 in your day job. Here’s what the federal tax brackets look like as of 2017 for a single person:

Assuming you take a standard deduction, you’ll be firmly in the 28% tax bracket. That means that for every $100 you earn on the side, you’ll be paying 28% federal income tax on that money, along with your state income tax, and both portions of FICA.

Here in Minnesota, the $100 that you earned might look something like this:

- $28 goes to federal income tax (28% tax rate)

- $7.85 goes to state income tax (7.85% tax rate)

- $7.65 goes to the employer portion of FICA tax (7.65% tax rate)

- $7.65 goes to the employee portion of FICA tax (7.65% tax rate)

So for someone making $100,000 in Minnesota, that extra $100 of side hustle income comes out to $48.85 after you’ve finished paying taxes on all of it.

That’s a really big hit. And it’s why it’s so important to reduce your tax liability as much as possible.

Ways To Reduce Your Tax Liability On Your Side Hustle Income

Since we know that taxes are problematic for side hustlers, what can we do about it?

Thankfully, when you’re side hustling as an independent contractor, you’ve got a lot of ways to reduce your tax liability. Here are just a few ideas:

(1) Use A Solo 401k. The amazing thing about side hustling is that you get access to extra retirement accounts that normal people don’t get to have. In essence, you’re giving yourself a bonus retirement account.

Depending on your work retirement plan situation, it’s possible that you can save almost the entirety of your side hustle earnings. That’s what I was able to do in 2016 since my government job offered a pension and 457 plan, but no 401k.

At a minimum, you’ll be able to put away about 20% of your side hustle earnings (after deducting expenses), which can be big. And setting up a Solo 401k is really easy and costs nothing if you use a company like Fidelity.

(2) Deduct Expenses. The other unique factor with side hustling is the ability to deduct expenses. Remember that when you pay for anything normally, you’re using post-tax income. Buying a coffee doesn’t really cost 2 bucks. It costs more than that because you need to earn $2 of post-tax income.

Your side hustle earnings, on the other hand, give you the ability to pay for expenses related to your side hustle with completely untaxed money.

Take, for example, my upcoming trip to FinCon – probably the nerdiest, gathering around. It’s basically a bunch of personal finance bloggers hanging out and talking about money and blogging. This was a trip I was already going to take, but by paying for it with my blog earnings, I’m able to deduct those costs from my blog revenue, and essentially, every dollar I spend on my FinCon trip is spent, completely tax-free.

(3) Get Some Of Your Side Hustle Income On Schedule E.

Most of the income you earn from your side hustles will end up on Schedule C. This is the tax form that you use to report income from a business where you were a sole proprietor. When your income is on Schedule C, you also have to pay the employer and employee portion of FICA (i.e. an extra 15.3% in taxes).

However, not all side hustle income has to end up on Schedule C. The other big form is Schedule E, which is what you use to report income from real estate and partnerships. If you rent out a room in your house, for example, and don’t provide any “substantial services” as the IRS calls it, then it’s just regular, old, real estate income. That’s how my Airbnb income is treated. All I do is provide a room for people and that’s pretty much it.

What makes Schedule E income good is that you don’t have to pay FICA taxes on it. That’s a 15.3% savings if you can put your side hustle income on Schedule E.

Takeaways

There’s a lot that goes into the world of side hustle taxes and it’s definitely something that can surprise you if you go into it without realizing the tax burden. In the old days, people working for themselves tended to be more sophisticated actors that had access to lots of tax advice. Today, with the rise of the sharing economy, anyone of us can go out there and earn money for ourselves. It can be overwhelming if you don’t know what you’re doing.

What’s important to remember here is that your side hustle earnings will be taxed at your highest tax rates since it’s all money you’re earning on top of your day job. Your goal, then, is to reduce that income as much as possible in order to keep as much of your money as possible.

What do you think? How do you go about reducing your tax liability on your side hustle income?

This post may contain affiliate links.

More Recommended Ebike/Scooters

Check out these other ebikes and scooters I've reviewed:

- Urban Arrow Ebike – Last year, I made one of the largest purchases I’ve ever made – I bought a $9,000 electric cargo bike from Urban Arrow. In my Urban Arrow review, I will discuss what it is and why I decided to buy this bike, as well as discuss how impactful a bike like this can be on your journey to financial independence.

- Troxus Explorer Step-Thru Ebike – The Troxus Explorer Step-Thru is a fat-tire ebike that I’ve had the pleasure of riding for a while now. It has amazing power, great looks, and awesome range. If you’re looking for a great fat-tire ebike that offers a lot for the price, the Troxus Explorer Step-Thru is definitely one for you to consider. Check out my Troxus Explorer Step-Thru Review.

- Hovsco HovBeta Ebike – The HovBeta is a folding ebike with great specs and a lot of interesting features, and importantly, it’s sold at a good price point. I’ve had a blast commuting with it and using it to do deliveries with DoorDash, Uber Eats, and Grubhub. Check out my Hovsco HovBeta Ebike Review.

- Vanpowers Manidae Ebike – The Vanpowers Manidae is a fat tire ebike that I’ve been riding as my primary winter commuting bike and have also been using it to do food delivery with apps like DoorDash, Uber Eats, and Grubhub. After clocking in a decent number of miles with this ebike, I wanted to write a post sharing what my experience with the Vanpowers Manidae ebike has been like. Check out my Vanpowers Manidae Review.

- Sohamo S3 Step-Thru Folding EBike Review – A Great Value Folding Ebike – The Sohamo S3 Step-Thru Folding Ebike is an entry-level folding ebike that offers a lot of value for the price point. I’ve been riding the Sohamo S3 for a while now, putting the bike through its paces, and I have to say, this bike has exceeded all of my expectations. Check out my Sohamo Review.

- KBO Flip Ebike – The KBO Flip is an excellent bike. I’ve had a great time riding it and think it’s a versatile bike that can be used for a lot of purposes and can fit a variety of lifestyles. It’s worked out great for me as a general commuter bike and as a food delivery bike. Check out my KBO Flip Review.

- Hiboy P7 Commuter Ebike – The Hiboy P7 is an excellent electric commuter bike that’s offered at an affordable price point. The range and speed of this bike are both very good, so you won’t have any trouble getting anywhere you need to go with it. As a food delivery vehicle, this is also good – with how much range it offers, you’ll be able to work all day on a single charge. Check out my Hiboy P7 Commuter Electric Bike Review.

- Himiway Escape Ebike – The Himiway Escape is an interesting bike for anyone looking for a moped-style ebike. If you’re a gig economy worker, the Himiway Escape is particularly interesting and it’s possible to think of it as an investment, especially if you can opt to do deliveries with the Himiway versus using a car. It’s not cheap, but you can definitely make your money back when you compare the mileage you’ll put on your car versus using an ebike. Check out my Himiway Escape Bike Review.

- Espin Sport Ebike – The Espin Sport is a good ebike for someone who is looking for an ebike that feels and rides more like a regular bike. There are many ebikes that are really only bikes in name. In reality, they’re basically electric mopeds. The Espin Sport, by contrast, is a bike you could probably ride without the battery and you’d feel like you’re just riding a regular bike. Check out my Espin Sport Review.

- Varla Eagle One Scooter – The Varla Eagle One is an excellent scooter that can make sense for a lot of people. It can work as a primary mode of transportation. You can use it to work on gig economy apps like DoorDash, Uber Eats, and Grubhub. And it can also be a recreational vehicle if you’d prefer to use it for that. Check out my Varla Eagle One Review.

- Varla Falcon Scooter – The Varla Falcon is an excellent scooter that offers a good amount of power at a lower price point compared to more powerful scooters. It’s not exactly an entry-level scooter, nor is it a high-powered scooter. I think it fits somewhere in-between those two categories – an intermediate scooter if I had to give it a category. Check out my Varla Falcon Review.

- Hiboy S2 Scooter – The Hiboy S2 is an excellent entry-level commuter scooter that's perfect for someone looking to save some money in transportation costs and improve their commute. Check out my Hiboy S2 Review.

- Hiboy S2R Scooter – The Hiboy S2R is one of the more interesting electric scooters I’ve been able to test out. It’s not a high-powered scooter, but for an everyday transport option, it’s very useful, especially given some of the unique features that it has. Indeed, for the price, the Hiboy S2R might be the best value scooter I’ve used. Check out my Hiboy S2R Review.

- Fucare H3 Scooter – The Fucare H3 is a fun scooter and I’ve enjoyed testing it out. For a daily commuter or quick trips or errands, the Fucare H3 is probably the scooter I’ll use. It’s portable and easy to maneuver, so it’s just easier to take on the road when I need it. Check out my Fucare H3 Scooter Review.

More Recommended Investing App Bonuses

For additional investing app bonuses, be sure to check out the ones below:

- M1 Finance ($75) – This is a great robo-advisor that has no fees and allows you to create a customized portfolio based on your risk tolerance. You also get $75 for opening an account. Check out my M1 Finance Referral Bonus – Step-By-Step Guide.

- SoFi Invest ($25) – SoFi Invest is an easy brokerage account bonus that you can earn with just a few minutes of work. Use my SoFi Invest referral link, fund your SoFi Invest brokerage account with just $10 and you’ll get $25 of free stock. I also have a step-by-step guide for the SoFi Invest referral bonus.

- Robinhood (1 free stock) – Robinhood gives you a free stock valued between $2.50-$225 if you open an account using my referral link.

- Public (1 free stock) - Public gives you a free stock valued between $3-$70 if you open an account using my referral link.

More Recommended Bank Account Bonuses

If you’re looking for more easy bank bonuses, check out the below options. These bonuses are all easy to earn and have no fees or minimum balance requirements to worry about.

- Ally Bank ($100) – Of all the banks out there, Ally is, without a doubt, my favorite. At the moment, Ally is offering $100 to customers who open an eligible Ally account and meet the requirements. Here are the step-by-step directions to earn your Ally Bank referral bonus.

- Chime ($100) - Chime is a free bank account that offers a referral bonus if you use a referral link and complete a direct deposit of $200 or more. In practice, any ACH transfer into this account triggers the bonus. This bonus is easy to earn and posts instantly, so you’ll know if you met the requirements as soon as you move money into the account. I wrote a step-by-step guide on how to earn your Chime referral bonus that I recommend you check out.

- US Bank Business ($400/$1200) – This is a fairly easy bank bonus to earn, since there are no direct deposit requirements. In addition, you can open the Silver Business Checking account, which comes with no monthly fees. Check out how to earn this big bonus here.

- Current ($50) – Current is a free fintech bank that’s offering new users a $50 referral bonus after signing up for an account using a referral link. Current is an easy bonus to earn and also gives you access to three savings accounts that pay you 4% interest on up to $2,000. That means you can put away up to $6,000 earning 4% interest. That’s very good and makes Current an account I recommend to everyone. Check out my step-by-step guide on how to earn your Current Bank bonus.

- Novo Bank ($40) - Novo bank is a free business checking account that’s currently offering a $40 bonus if you open a Novo business checking account using a referral link. In addition to being a good bank bonus, Novo is also a good business checking account. It has no monthly fees or minimum balance requirements and operates a good app and website. Indeed, it’s the business checking account I currently use for this blog. Check out my post on how to easily open a Novo account.

- Varo ($25) – Varo is a free fintech banking app similar to Chime or Current. It’s currently offering a $25 bonus to new users that open a new Varo account with a referral link. The bonus for this bank is very easy to meet, all you need to do is spend $20 within 30 days of opening your Varo account. Check out my step-by-step guide to learn how to earn this bonus.

Kevin is an attorney and the blogger behind Financial Panther, a blog about personal finance, travel hacking, and side hustling using the gig economy. He paid off $87,000 worth of student loans in just 2.5 years by choosing not to live like a big shot lawyer.

Kevin is passionate about earning money using the gig economy and you can see all the ways he makes extra income every month in his side hustle reports.

Kevin is also big on using the latest fintech apps to improve his finances. Some of Kevin's favorite fintech apps include:

- SoFi Money. A really good checking account with absolutely no fees. You'll get a $25 referral bonus if you open a SoFi Money account with a referral link, and an additional $300 if you complete a direct deposit.

- 5% Savings Accounts. I'm currently getting 5.24% interest on my savings through a company called Raisin. Opening a Raisin account takes minutes to complete, it's free, and all of your funds are FDIC-insured. I explain how it works, why I'm now using it to store my emergency fund and any other cash savings I have, and why I recommend everyone check it out in this review.

- US Bank Business. US Bank is currently offering new business customers a $400/$1200 signup bonus after opening a new account and meeting certain requirements.

- M1 Finance. This is a great robo-advisor that has no fees and allows you to create a customized portfolio based on your risk tolerance. You also get $75 for opening an account.

- Empower. One of best free apps you can use to monitor your portfolio and track your net worth. This is one of the apps I use to track my financial accounts.

Feel free to send Kevin a message here.

I know this lost is a few years old, just recently found your blog and started doing side hustles like Field Agent etc. I know you are not an accountant, but I have two questions. If my total income from any one source (ie Field Agent, WeGoLook, or EasyShift) is less than $600, do I still have to claim on taxes? What if the cumulative is above $600 And second question–can I claim mileage as a deduction for those type of jobs? Thanks, love the site!

Hey David,

The technical rule is that all income is taxable. With that said, once you make over $600 from any one app, by law, the company is required to send you and the IRS a 1099. If it’s under $600, then they are not required to send you a 1099.

Yes, you can claim mileage deductions from those gigs. That’s a 100% legitimate business expense.

Thanks for the follow-up! Would you treat each completed job starting from home? Or if you were at point A and had to get to a job, would you use that starting point? I need to buy a mileage book!

I’m not sure of the rules off the top of my head, so you’ll need to check when you can start deducting your mileage. You can use Everlance to keep track of your miles. That’s a free mileage tracking app that works well.

You said that if it’s under $600, they’re not required to send you a 1099. Would they still send a 1099 to the IRS though?

Sorry to bother you again. You’re the most helpful blogger I notice. I get most of my self-employment money from online survey sites and some from Rover/Wag. I hope to apply to online teaching one day. I just want to confirm I’m clicking the right options.

While completing the EIN application, I chose myself as a “Sole Proprietor” and that I “Started a new business”.

The part where I’m stuck is when it asks “What does your business or organization do?” There’s options such as construction, food service, insurance, etc. Since none of those are what I’m doing, I selected “Other”. After clicking that, it gives me choices such as service, consulting, etc and a final option where I can type in what my primary business activity is. Since dog-sitting is so different from online survey sites or online teaching, what do you recommend I do? For you I know you have a lot of different side hustles. What did you put down as your business? Thanks!!

Hey Dan, just pick anything you want. That part really doesn’t matter, so what you picked is fine. Ultimately, you’re just a business of you. As Jay-Z would say, you’re not a businessman. You’re a business, man!

I’ve been making money off of survey sites, Wag, and Rover. Do I need an EIN for each side hustle if I want to contribute to a solo 401k?

No, you can have one EIN for yourself and all of that income can go into the same Solo 401k. You’re a sole prop and your business is just your full name.

Thanks! So I put my full name as the d.b.a. on the EIN application? Do I have to also register for a d.b.a. separately?

Nope, you don’t need to register for anything. It’s just your name.

This was a very helpful post! Have you tried using the Savant app? It’s currently in beta mode but it supposedly helps track earnings, taxes, etc., as well as help manage all of your side hustles in one place. I am curious if anyone has had experience with it.

I’ve never tried that app but I might take a look.

This was a great breakdown! I’ll be sharing this on my social media.

Right now side hustle income isn’t a tax issue for me because I stick to AirBnB for 14 nights a year or less. I do some mystery shopping but most of it is reimbursements which are non taxable. I have enough deductions where the taxes on the $200 of income I’ve brought in are negligible. But this will come in handy in 2018 (depending on how the tax code changes and when) when I expand my side hustling to replace the income I lost when laid off.

Thanks! That’s awesome that you do Airbnb for 14 days or less – seems like everyone should do that since it’s literally one of the only ways to get legitimate, tax-free income.

Taxes are theft. It’s one of the nightmares we all have.

Thanks for this guide. A very helpful post.

Happy to help James. I don’t necessarily think taxes are theft, but it’s definitely important to do what you can to lower your own tax liability.

Thanks for the detailed guide! Taxes are one of my least favorite things to do in the world. I usually just use TurboTax to file my taxes. I currently don’t generate any side hustle income, but I’ve thought about whether I should even hire a CPA to help me pay less taxes (legally) when I do have a side business/hustle >_<

My side hustle is Uber, and this is my 3rd year running it at a “loss” when it comes to my tax filings. Miles driven x $0.535 per mile = a substantial tax deduction that exceeds my Uber income (and tips, if I’m being honest). But luckily my actual cost of operating is significantly less than 53.5cents per mile, so I do OK with Ubering. Definitely not getting rich at it, but it’s a nice little secondary income of $10k-ish per year.

Wow nice, Uber is perfect for tax deduction.

Do you file yourself? do you dont need to tax estimate tax or income tax , cause its technically a loss?

Sounds like the perfect side hustle

But i dont really like driving

How long do you drive a month doing uber?

The big monkey wrench, imho, are estimated taxes. Depending on your hustle income you have to calculate your estimated taxes ahead of April if you don’t want a penalty.

So, this is an interesting thing. Last year, I didn’t pay any quarterly taxes and owed a penalty. My penalty? A whopping $8. The penalty is apparently half a percent of whatever underpayment of taxes you owe. So, unless your side hustle is huge, for a lot of people, I think it seems like you’ll pay enough taxes in your day job to avoid any big penalty when you file.

My first year doing side hustle, not paying quarterly taxes right now either.

So you cant pay the full amount at the end of the year? You get charged the penalty for sure then right?

My side hustle is pretty huge.

How do you file online? using the etfps or something like that?

You file a 1040 with schedule c or you only need to pay some taxes?

Awesome! I was curious about how the side hustles taxes worked with me having a full-time job. I wasn’t sure if I would have to estimate my quarterly taxes.

Thanks for putting this together, FP. I booked marked this so I can come back when I hopefully get my side hustles going…

Thanks man!

Wow this is the information i needed. Great article, well written

You should do some more articles on filing taxes. Like schedule C , 1040, bank interest , deductions

Do you file yourself or you have an accountant?

I just started my own side hustle too, but the taxation is very scary.

Technically not a side hustle as its my main income, as im a full time student, but it gets taxed as a side hustle 🙁

Thanks Kevin. It’s a good idea – I’ll probably be writing more about this stuff as I do taxes.

I file myself for now, although we’ll have to use an accountant once my wife buys a dental practice. That’ll just be way too much stuff to do by ourselves.

Thank you so much for this! I’ve been waiting for it for a bit now. In the beginning I think you meant that if you make $100k and take the standard deduction you would be in the 28% bracket not 25%, since your AGI would be about ~$94k.

Have you found that Postmates / Field Agent / other apps send you 1099’s super late in the year?

Also AirBnB income cannot be put into a solo 401k correct?

Good catch! Will revise the post to say that!

Postmates, Field Agent, and the like won’t send you a 1099 unless you make over $600 in a year.

Correct, you can’t put Airbnb income into a Solo 401k IF you’re putting that income on Schedule E. If you’re providing substantial services, then it would fit under Schedule C. There’s some debate out there in the Airbnb world – some people say it’s schedule C, other people say it’s schedule E. I’d say it probably depends on how much like a hotel you really are.