I was recently talking to a buddy of mine about personal finance when we ended up on the topic of saving money. He knew he needed to save more money, but was having trouble actually doing it. To him, saving money came down to self-control. As he explained it, he was struggling to save more because he couldn’t resist the urge to spend. If he could just avoid buying the latest gadgets or going out to eat so often, he’d definitely be able to put more money away – or so he told himself. In short, saving money came down to willpower. If he wanted to save more, he needed to will himself to do it.

I’ve always seen it a little differently. I’m admittedly a terrible budgeter. I don’t give every dollar a job. And while I track my account balances regularly using both Mint and Personal Capital, I rarely, if ever, actually sit down and review my spending. I’m also horrible at self-control. I go out to eat all the time. And if I see something that I want that isn’t too expensive, I’ll just buy it without much thought.

Despite what appears to be a total lack of budgeting, my savings continues to grow by leaps and bounds. In 2016, I saved over $33,000, which is more astounding when you consider that I took a $50,000 pay cut in the middle of the year. In 2017, even with my pay cut, I still managed to save over $31,000.

My ability to save doesn’t have to do with willpower or self-control. Instead, it’s all about the systems I have in place to make my pool of money look as small as possible. You don’t need to exercise self-control because a computer can do all of the saving for you.

Think Of Money In Terms Of Portion Sizes

I’ve always thought that saving money is a lot like eating food. When it comes to food, most of us will pretty much eat whatever is put in front of us. Give your average person a huge plate of food and they’ll probably need to eat all of it before they feel full. Put a smaller plate in front of that same person and they’ll probably start feeling full once they’ve finished that smaller plate. It’s a weird psychological thing that our brains can’t seem to avoid.

Money works in pretty much the same way – we just sort of make do with whatever is put in front of us. If you give me $2,000 per month to spend, I’ll probably figure out a way to spend about that much every month. Cut that down in half and I can probably figure out a way to work with that too. Your brain will just sort of trick you into working with what you have.

If you think this isn’t true, just go back in time and look at what you did when you were a student. You probably didn’t have all that much money back then. Things that are necessities now – the big house, the luxury apartment, the car, the nice clothes, the better food – just didn’t seem all that necessary back then. Your portion size was just smaller, out of necessity obviously, rather than choice.

You can save more if you can just control this portion size. It has nothing to do with self-control. You just need to make your portions smaller.

Automate Your Savings

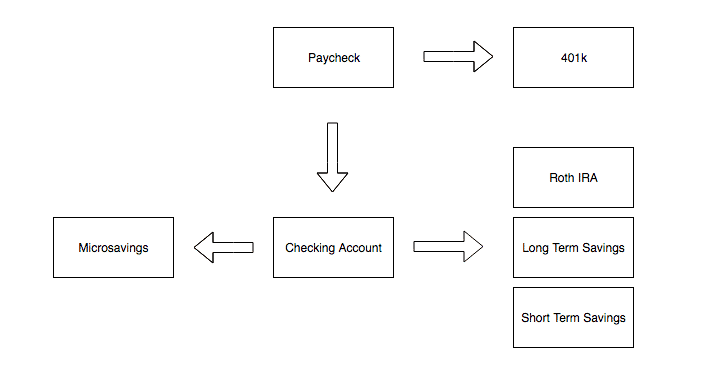

The secret to saving is setting up an automated system to get that money out of your hands as fast as possible. We all start with what I think is a pretty big plate – our paychecks. If you let that money sit in front of you, you’re going to find ways to spend it.

The great thing is that with technology the way it is, it’s easy to get that money out of our hands quickly. Below is an example of how your savings can be automated. You’ve got money coming out of your paycheck in the form of 401k deductions and things like that. Those are great ways to keep that plate smaller since you never even get a chance to spend that money.

Money that actually arrives in your checking account should also be moving towards other places to keep your money plate small. I have set amounts that I take out of each paycheck for Roth IRA contributions and long and short-term savings goals. This gets the money out of my hands so that I’m not tempted to use it. I then use microsavings apps like Dobot or Albert to squeeze out just a little more savings from my checking account.

Feel free to read my reviews on Dobot or Albert if you’re looking for more information on how these apps work:

- Dobot App Review – A Legit Free Alternative To Digit

- Albert App Review: Smart, Automatic Savings (And Another Free Alternative To Digit)

By setting up an automated system like this, you’ll naturally reduce the amount of money that you actually have in your hands. Your plate is getting smaller. No self-control is involved. Instead, you’re just tricking your brain to get used to living on the smaller amount.

Make Your Savings Hard To Get

Saving money doesn’t mean anything if you’re just going to dip into your savings whenever you want to buy something. That’s why you need to make sure that any money you save is in a place where you can’t reach it all that easily.

Employer-sponsored retirement plans are a great example of how you can make your money hard to get. You set a percentage to save – preferably as high as you can – and you never see that money in your paycheck. Since it’s not all that easy to pull money out of your retirement accounts, you’re much less likely to touch it.

This is another reason why I recommend saving your emergency fund in a 5% interest savings account with Netspend. Not only are you snagging 5% interest, you basically add another layer between you and your savings. That small layer makes it much less likely that you’ll dip into your emergency fund for things that you don’t really need.

Tools To Help You Automate Your Savings

There are a ton of tools to help you automate your savings and keep your money plate smaller. If you’re trying to save more money, you need to be using tools like these:

-

- Employer-Sponsored Retirement Plans: Almost every full-time employee will have access to a 401k or something similar. Take advantage of these accounts, preferably maxing out every plan you have access to if you can (assuming you have at least some decent investment options). It’s an easy way to save without having to exercise any self-control.

- Capital One 360: Everyone should have cash savings for short-term and longer-term goals. The best way to save for these types of goals is to automate your savings towards these goals. The key, though, is to keep that money separate from your primary stash. I have a bunch of different sub-accounts that I’ve opened up through Capital One 360. Each month, Capital One 360 withdraws a set amount from my primary bank account and into each of these accounts. I get to save without even noticing it. If you’ve never used Capital One 360, I highly recommend it.

An example of my own short-term savings goals. I automate deposits into these accounts each month. It allows me to save without even trying. - Dobot: Even after you’ve done all of your saving, there’s value in trying to squeeze out a little bit more savings by using microsavings apps. I use Dobot to do that for me. It monitors my checking account, figures out if I have a surplus, and saves small sums for me that it feels I won’t notice. It’s like making your plate smaller by having someone else pull food off your plate that you probably don’t need to eat. If you find that you can’t handle the extra savings, just turn off the app. My guess is most of you will start getting used to seeing extra money getting saved every few days. And once you’re used to it, it’s not a big deal. Check out my Dobot review for more info.

You Don’t Need To Force Yourself To Save

Saving money might involve some self-control, I won’t deny that. With things like credit cards, it’s not all that hard to spend more than you have. But when you make your pile of money look much smaller, you’ll naturally start spending less simply because you’ll feel like you have less money to spend.

You don’t need to force yourself to save. Just set up your savings once, put it as high as you can, and get used to living on the amount you see leftover. No self-control needed.

This post may contain affiliate links.

More Recommended Ebike/Scooters

Check out these other ebikes and scooters I've reviewed:

- Urban Arrow Ebike – Last year, I made one of the largest purchases I’ve ever made – I bought a $9,000 electric cargo bike from Urban Arrow. In my Urban Arrow review, I will discuss what it is and why I decided to buy this bike, as well as discuss how impactful a bike like this can be on your journey to financial independence.

- Troxus Explorer Step-Thru Ebike – The Troxus Explorer Step-Thru is a fat-tire ebike that I’ve had the pleasure of riding for a while now. It has amazing power, great looks, and awesome range. If you’re looking for a great fat-tire ebike that offers a lot for the price, the Troxus Explorer Step-Thru is definitely one for you to consider. Check out my Troxus Explorer Step-Thru Review.

- Hovsco HovBeta Ebike – The HovBeta is a folding ebike with great specs and a lot of interesting features, and importantly, it’s sold at a good price point. I’ve had a blast commuting with it and using it to do deliveries with DoorDash, Uber Eats, and Grubhub. Check out my Hovsco HovBeta Ebike Review.

- Vanpowers Manidae Ebike – The Vanpowers Manidae is a fat tire ebike that I’ve been riding as my primary winter commuting bike and have also been using it to do food delivery with apps like DoorDash, Uber Eats, and Grubhub. After clocking in a decent number of miles with this ebike, I wanted to write a post sharing what my experience with the Vanpowers Manidae ebike has been like. Check out my Vanpowers Manidae Review.

- Sohamo S3 Step-Thru Folding EBike Review – A Great Value Folding Ebike – The Sohamo S3 Step-Thru Folding Ebike is an entry-level folding ebike that offers a lot of value for the price point. I’ve been riding the Sohamo S3 for a while now, putting the bike through its paces, and I have to say, this bike has exceeded all of my expectations. Check out my Sohamo Review.

- KBO Flip Ebike – The KBO Flip is an excellent bike. I’ve had a great time riding it and think it’s a versatile bike that can be used for a lot of purposes and can fit a variety of lifestyles. It’s worked out great for me as a general commuter bike and as a food delivery bike. Check out my KBO Flip Review.

- Hiboy P7 Commuter Ebike – The Hiboy P7 is an excellent electric commuter bike that’s offered at an affordable price point. The range and speed of this bike are both very good, so you won’t have any trouble getting anywhere you need to go with it. As a food delivery vehicle, this is also good – with how much range it offers, you’ll be able to work all day on a single charge. Check out my Hiboy P7 Commuter Electric Bike Review.

- Himiway Escape Ebike – The Himiway Escape is an interesting bike for anyone looking for a moped-style ebike. If you’re a gig economy worker, the Himiway Escape is particularly interesting and it’s possible to think of it as an investment, especially if you can opt to do deliveries with the Himiway versus using a car. It’s not cheap, but you can definitely make your money back when you compare the mileage you’ll put on your car versus using an ebike. Check out my Himiway Escape Bike Review.

- Espin Sport Ebike – The Espin Sport is a good ebike for someone who is looking for an ebike that feels and rides more like a regular bike. There are many ebikes that are really only bikes in name. In reality, they’re basically electric mopeds. The Espin Sport, by contrast, is a bike you could probably ride without the battery and you’d feel like you’re just riding a regular bike. Check out my Espin Sport Review.

- Varla Eagle One Scooter – The Varla Eagle One is an excellent scooter that can make sense for a lot of people. It can work as a primary mode of transportation. You can use it to work on gig economy apps like DoorDash, Uber Eats, and Grubhub. And it can also be a recreational vehicle if you’d prefer to use it for that. Check out my Varla Eagle One Review.

- Varla Falcon Scooter – The Varla Falcon is an excellent scooter that offers a good amount of power at a lower price point compared to more powerful scooters. It’s not exactly an entry-level scooter, nor is it a high-powered scooter. I think it fits somewhere in-between those two categories – an intermediate scooter if I had to give it a category. Check out my Varla Falcon Review.

- Hiboy S2 Scooter – The Hiboy S2 is an excellent entry-level commuter scooter that's perfect for someone looking to save some money in transportation costs and improve their commute. Check out my Hiboy S2 Review.

- Hiboy S2R Scooter – The Hiboy S2R is one of the more interesting electric scooters I’ve been able to test out. It’s not a high-powered scooter, but for an everyday transport option, it’s very useful, especially given some of the unique features that it has. Indeed, for the price, the Hiboy S2R might be the best value scooter I’ve used. Check out my Hiboy S2R Review.

- Fucare H3 Scooter – The Fucare H3 is a fun scooter and I’ve enjoyed testing it out. For a daily commuter or quick trips or errands, the Fucare H3 is probably the scooter I’ll use. It’s portable and easy to maneuver, so it’s just easier to take on the road when I need it. Check out my Fucare H3 Scooter Review.

More Recommended Investing App Bonuses

For additional investing app bonuses, be sure to check out the ones below:

- M1 Finance ($75) – This is a great robo-advisor that has no fees and allows you to create a customized portfolio based on your risk tolerance. You also get $75 for opening an account. Check out my M1 Finance Referral Bonus – Step-By-Step Guide.

- SoFi Invest ($25) – SoFi Invest is an easy brokerage account bonus that you can earn with just a few minutes of work. Use my SoFi Invest referral link, fund your SoFi Invest brokerage account with just $10 and you’ll get $25 of free stock. I also have a step-by-step guide for the SoFi Invest referral bonus.

- Robinhood (1 free stock) – Robinhood gives you a free stock valued between $2.50-$225 if you open an account using my referral link.

- Public (1 free stock) - Public gives you a free stock valued between $3-$70 if you open an account using my referral link.

More Recommended Bank Account Bonuses

If you’re looking for more easy bank bonuses, check out the below options. These bonuses are all easy to earn and have no fees or minimum balance requirements to worry about.

- Ally Bank ($100) – Of all the banks out there, Ally is, without a doubt, my favorite. At the moment, Ally is offering $100 to customers who open an eligible Ally account and meet the requirements. Here are the step-by-step directions to earn your Ally Bank referral bonus.

- Chime ($100) - Chime is a free bank account that offers a referral bonus if you use a referral link and complete a direct deposit of $200 or more. In practice, any ACH transfer into this account triggers the bonus. This bonus is easy to earn and posts instantly, so you’ll know if you met the requirements as soon as you move money into the account. I wrote a step-by-step guide on how to earn your Chime referral bonus that I recommend you check out.

- US Bank Business ($400/$1200) – This is a fairly easy bank bonus to earn, since there are no direct deposit requirements. In addition, you can open the Silver Business Checking account, which comes with no monthly fees. Check out how to earn this big bonus here.

- Current ($50) – Current is a free fintech bank that’s offering new users a $50 referral bonus after signing up for an account using a referral link. Current is an easy bonus to earn and also gives you access to three savings accounts that pay you 4% interest on up to $2,000. That means you can put away up to $6,000 earning 4% interest. That’s very good and makes Current an account I recommend to everyone. Check out my step-by-step guide on how to earn your Current Bank bonus.

- Novo Bank ($40) - Novo bank is a free business checking account that’s currently offering a $40 bonus if you open a Novo business checking account using a referral link. In addition to being a good bank bonus, Novo is also a good business checking account. It has no monthly fees or minimum balance requirements and operates a good app and website. Indeed, it’s the business checking account I currently use for this blog. Check out my post on how to easily open a Novo account.

- Varo ($25) – Varo is a free fintech banking app similar to Chime or Current. It’s currently offering a $25 bonus to new users that open a new Varo account with a referral link. The bonus for this bank is very easy to meet, all you need to do is spend $20 within 30 days of opening your Varo account. Check out my step-by-step guide to learn how to earn this bonus.

Kevin is an attorney and the blogger behind Financial Panther, a blog about personal finance, travel hacking, and side hustling using the gig economy. He paid off $87,000 worth of student loans in just 2.5 years by choosing not to live like a big shot lawyer.

Kevin is passionate about earning money using the gig economy and you can see all the ways he makes extra income every month in his side hustle reports.

Kevin is also big on using the latest fintech apps to improve his finances. Some of Kevin's favorite fintech apps include:

- SoFi Money. A really good checking account with absolutely no fees. You'll get a $25 referral bonus if you open a SoFi Money account with a referral link, and an additional $300 if you complete a direct deposit.

- 5% Savings Accounts. I'm currently getting 5.24% interest on my savings through a company called Raisin. Opening a Raisin account takes minutes to complete, it's free, and all of your funds are FDIC-insured. I explain how it works, why I'm now using it to store my emergency fund and any other cash savings I have, and why I recommend everyone check it out in this review.

- US Bank Business. US Bank is currently offering new business customers a $400/$1200 signup bonus after opening a new account and meeting certain requirements.

- M1 Finance. This is a great robo-advisor that has no fees and allows you to create a customized portfolio based on your risk tolerance. You also get $75 for opening an account.

- Empower. One of best free apps you can use to monitor your portfolio and track your net worth. This is one of the apps I use to track my financial accounts.

Feel free to send Kevin a message here.

Yes! This is one of the reasons we did a 15 year mortgage!

An easy way to force yourself to live on less!

I agree that putting the right systems and automation in place is key. I also believe that a change in mindset is helpful. Instead of always thinking “No, I need to control myself and not buy the new gadget I want so badly” we can turn it around and say “I really want this new gadget, how can I afford to uy it?”

If we do that maybe we’ll start prioritizing purchases or even looking for new ways to make extra money to spend on those luxuries.

Great way to think about it – it’s not about forcing yourself not to buy stuff, but figuring out how you can buy the thing if you want it. If you think about it like this, you’re basically flipping your brain.

This is definitely my style, too. I make it a point that I always outwit my spending self. Instead of credit cards, I went for debit card. My paycheck also goes to separate accounts that is hard to withdraw. 🙂 That way, I have to get through with the right amount of money that I have. But I always address my desires, as well. Because for me, I work to satisfy myself and not to deprive me of good things. ^_^

If you go with debit card and no overdraft, you’ll definitely force yourself to outwit your spending stuff. Can’t spend what you don’t have!

Automating my savings has been huge- I’ve created separate savings account for everything from future vacations to car funds thanks to Capital One 360!

Awesome! I’m glad its been working out for you. I totally think it’s worthwhile to try using Dobot and Qapital as well on top of automated savings in Cap One 360. It’s basically forcing yourself to squeeze just a little bit more savings

I’m terrible with budgets and don’t use them. Similar to you I regularly monitor my cash flow and balances to be aware of what is going-on in terms of spending and make small adjustments as needed.

BTW, I had a hard time focusing on your article after I saw that picture of massive burger 🙂 I would like to counter it with a 7-decker burger picture I took in Japan and posted on my blog:

http://www.mrallthingsmoney.com/2016/09/quiting-my-job-may-have-saved-my-life.html

Haha, that burger in your post is awesome!

I don’t budget either but I do check my net worth weekly on Mint & Personal Capital. Why are they always different?

Anyway, my cashflow diagram looks like yours except I don’t have Microsavings. The only difference is the arrow goes from Checking to Short-Term Savings to Long-Term Savings to Roth IRA. Also, the arrow is bidirectional between Checking & Short-Term Savings to reflect months where I have unusually high expenses.

What I do is monitor my checking account balance on the 1st and 15th of each month. I compare it to the balance on the 1st or 15th of the previous month, respectively. I consider the expenses I have due before the next paycheck and may or may not sweep money from Short-Term Savings to the Checking Account or vice versa based on account balance and upcoming bills.

Some of the movement from Checking Account to Short-Term Savings is automated to encourage savings. I am also loathe to sign up for services with recurring charges. That is essentially automating your spending.

Do you mean your Mint and Personal Capital accounts have different Net Worth Amounts? Mint tends to support more banks, so that’s probably why. Also, Personal Capital sometimes has issues tracking HSAs for some reason.

Good point about signing up for services with recurring charges! It’s basically like the opposite of automated savings (which is why companies love subscription based spending).

I experience the same thing since I started to transfer money to my investment account the first thing when my salary arrives. If you want to save from whatever left at the end of the month, you probably end up saving nothing or very little.

Exactly! We just all spend whatever is in front of us. And we can all make do with whatever we have left over. It’s just about setting it all up in advance.

It’s true that budgeting really pays off with time. When I was asked to pay for my own car insurance, I was confused like never before. But it was a lesson that taught me to be responsible on road and towards managing my finances.

I see the value a budget provides because it enables us to have a gauge on our spending. However, we struggle sticking exactly to our budget. We do use the automated method to max out our retirement accounts. It makes it much easier to save!!

Totally does man. I’m always shocked at how much I’m able to put away each month just because I’ve set up my savings in advance.

We def. have fallen prey to credit card use but I try to move paycheck money over to savings as fast as possible when hubby gets paid. We have a Cap One 360 account and that Netspend one sounds interesting but I’m not really liking the fact that I have to open up 5 accounts per person cuz I can’t deposit more than 1k. Overall, great article!

Thanks! Yeah, the Netspend accounts take a little bit of work, but it’s really not much work to set up. I look at it just 4 times per year and my wife doesn’t look at her accounts at all.

I m horrible at keeping to a budget, lot’s of great information to get me started. I like the idea of automating your savings and making it harder to access.

Automating is the key! Get that money as far away from you as possible and you’ll figure out how to make do with the rest!

Mr. FAF and I don’t track every dollar we spend either. Our philosophy is to spend as little as possible. We discuss purchases bigger than $50. Our only weakness is food. There’s something so enjoyable and fulfilling about eating delicious Asian food that I just can’t explain!

Food is my definite issue too. I feel like if I did budget and track my spending better, I’d be able to avoid the unnecessary food spend. A part of it is laziness – I just sometimes feel too tired to cook. Other part of it is a lack of planning – I just sometimes don’t know what to eat and then going out to eat becomes the default option.

My best “no brainer” savings method is to cut the big expenses. You probably will miss $50/month from your account more than you will notice the difference in the house you can buy or rent for $X vs X-50. The same with the car. Heating or cooling a smaller place is an easier way to save money on electricity than following 101 steps to a lower electric bill.

Totally agree! If you can cut your expenses when it comes to the two most expensive things we have – house and car – you can really set yourself up to save a ton more money.

By the way, I’ve read your Kickfurther posts and I’ve also had some bad experiences with Kickfurther. It taught me a lesson about getting into weird investments.

I use this approach and I like it, but… It only works for those that are limited by what they make. Some folks go deeply in debt on credit cards each month. These people need either self control or no access to credit, no money in the bank clearly has no impact. I’d recommend adding to auto savings and evaluation of what you spend to see what you truly value. Then if you can’t handle them removing the cards.

Definitely true – and maybe it’s too broad to say that it’s not about self-control. I gotta go out there and makes waves 🙂

I’ve always just sort of treated my credit card like it was a debit card, so limiting the amount of money I “see” has always been a good way to save more money.