This Part 2 of my Decade-In-Review. Please read Part 1 if you’re interested in learning more about how I ended up here.

I left off my last post at the point where I’d just graduated from law school, moved into an apartment with my girlfriend, and was getting ready to start my first real job after having spent the summer studying for and then taking the bar exam. This was in September 2013 – four years after I had graduated from college, moved back home with my parents for a year, then moved to Minnesota to start law school.

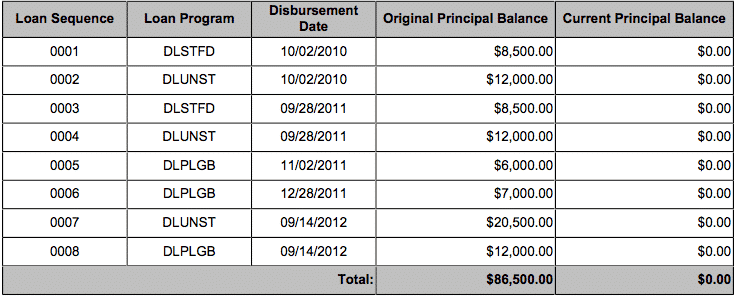

At this point, I had $87,000 worth of student loans and didn’t have any idea how I was supposed to handle it. I also had very little knowledge about how money worked in general, which isn’t the best thing when you consider that I was about to start a six-figure job at 26-years old after never having made any significant money in my entire life (before I started my first real job out of law school, I’d made a grand total of $31,000 in the previous three years, with $20,000 of that coming from my summer associate position).

I’d say the second half of the decade was when I started to learn more about who I was and what drove me. It also led me to start living life more out of abundance, rather than doing things out of fear. Let’s take a look at what happened over the rest of the decade.

A Rough Transition To The Working World

My first job was as an associate at a large law firm in Minneapolis. A sense of dread hit me soon into my career as the day-to-day reality of biglaw life started to take its toll on me. My issue was that this type of environment just wasn’t a good fit for me. I don’t think I was well-equipped to deal with the stuff that some people might thrive on – constantly hustling for work, billing hours, and dealing with office politics, all of which were things I was not good at and did not enjoy doing.

In retrospect, it’s sort of easy to see why biglaw (and corporate life in general) wasn’t a great fit for me. Up until this point, I’d been living a life that matched my personality pretty well. I’d had that one amazing year in 2010 where I’d lived at home and was working jobs that, even though they weren’t high paying, were at least fun to do and gave me a lot of freedom and autonomy to do my own thing while I was working.

My first year of law school was pretty miserable, but it still provided me with a lot of autonomy. Sure, I had basic parameters I had to work within, but my time was basically mine to use as I saw fit. I studied a lot, but it felt different because I could study wherever I wanted, whenever I wanted, and however I wanted. No one was looking over my shoulder and I didn’t have to report to anyone.

And then, those final two years of law school were basically college 2.0 in my eyes. I didn’t have a lot of worries since I had a good job waiting for me and thought that I had it made. Studying for the bar was also really enjoyable – again because it felt like I could do what I wanted and I made my own schedule without anyone looking over my shoulder.

I think that’s the theme of what type of work was going to make me happy. Having basic parameters around what I needed to do was fine, but I think I needed a sense of real autonomy more than anything. My “fake” low-wage jobs and law school provided that to me. I made my schedule around broad parameters, but it was up to me to decide how and when I got stuff done.

Feeling Trapped – So I Took Action

It was early in my legal career when I realized that the biglaw lifestyle wasn’t going to work for me. I was struggling professionally and never really felt like I was doing a good job. The constant stress also took a toll on me personally.

My only issue was that I still had $87,000 worth of student loans that I needed to get rid of. I was on a 10-year repayment plan. so my monthly payment was around $1,000 per month. As a point of comparison, my rent at the time was $575 per month and I didn’t have a car, so my highest monthly expense was my student loan payment. In other words, I needed this job.

2014 was when I started to take action on my student loans and also when I started to get very interested in personal finance. My first introduction to the personal finance world was through Dave Ramsey. I’ve got some problems with Dave Ramsey and a lot of the things he says, but I can’t deny that it was his YouTube channel that first made me feel like my debt was a problem and that it was something I could get rid of quickly if I really tried.

Later, I discovered the financial independence community, and this completely changed my world on what I thought was important. Instead of valuing stuff and prestige, I began to value time and freedom.

I ended up working at that biglaw job for about three years while I threw down as much money as I could into my student loans. During this time, I invested very little into my 401k, only putting about 5% of my income into it, which was the default amount that my employer took from our paycheck. From 2014 through 2016, I ended up paying a little over $102,000 towards my student loans and got them all paid off by the summer of 2016, about 2.5 years after I had started paying off my debt.

To do this, I did the basics that anyone paying off student loans has to do – I lived on much less than I earned and put the rest of my income towards my student loans. Doing this wasn’t particularly difficult for me, but it required me to do a few things that not everyone does.

- First, I lived in a “normal” apartment (i.e. not a luxury apartment). During my debt payoff journey, my wife and I always lived in 1-bedroom apartments, where my share of the rent was never more than $600 per month. We had one year in 2015 where we lived in a fancy luxury apartment because I took over a lease for a guy who had just signed it and needed to move. The cost for him to break his lease was really expensive, so he ended up paying for a few months of the rent so that I would take over his lease. Because of this, my share of the rent for this luxury apartment ended up being only $575 per month, which was a great deal for the fanciest place we’d ever lived in. This was the same apartment where I found that dumpster in the garage that literally made me $1,300 in a year.

- Second, I didn’t have a car and instead, I got around either by taking the bus, or even better, biking. I didn’t have my own bike either – instead, I used the Minneapolis bike share system, which cost me $65 per year and let me ride the bikes as many times as I wanted. There’s literally no cheaper way to get around a city – not even mass transit is cheaper than that.

- Third, I kept my food costs down a lot mainly because I took advantage of the perks that came with my biglaw job. Free food, for example, wasn’t hard to find most days. There were often CLE classes during the lunch hour where I could walk in and snag some free food pretty easily. During the summer, our meals were reimbursed if we went to lunch with summer associates, so from May to August, I’d basically eat for free every day.

During my time in biglaw, I made a lot of money, which is also why I was able to pay off my student loans as fast as I did. My starting salary in 2013 and 2014 was $110,000. In 2015, I got a raise to $115,000. And in 2016, my salary went up again to $125,000.

Turning To Side Hustles – But Not For The Normal Reasons

A lot of people think of this blog as a side hustle blog and it’s true that side hustling is something that has made up a big part of the last few years of my life. My side hustling adventure started in 2015 when a food delivery app called Caviar launched in Minneapolis. This was the first time I had used any of these gig economy apps and I became hooked on them. I didn’t have a car, so I used my bike to do my deliveries and for whatever reason, I found it ridiculously fun to do. In my mind, it felt like I was getting paid to go outside and bike, which was something that I was already doing anyway.

It was around this time that I realized the gig economy could be used by anyone, even someone like me who was working a lot of hours at a demanding, professional job. I found that all of these gig economy apps could easily fit into my day-to-day life if I used them right. As an example, on my way home from work, I’d turn on my delivery apps, find a few deliveries heading back towards my house, and deliver food to people on my way home. A few bucks here and there on my way home didn’t seem like a lot of money, but when I did the math, it surprisingly added up.

But side hustling did something even more important for me than to help me make a little bit of extra money. It served as a form of therapeutic relief from the daily stresses of work. After spending all day sitting at a desk and feeling stressed from so many obligations, there was some comfort in being able to get on my bike and do relatively simple tasks on my own schedule. It also gave me some confidence in knowing that I could figure out how to make things work and make money on my own, without relying on a normal job.

Over time, as I learned more about how to make side hustling work for me, I continued to add more side hustles into my repertoire. For example:

- In June 2015, I set up a profile on Rover and started my dogsitting business. My rationale here was that since I already had a dog, adding a second dog into the mix wouldn’t really be difficult. I already had to take care of my own dog, so in a way, dogsitting with Rover was a way for me to monetize the dog care tasks I was already doing anyway.

- In January 2016, my wife and I moved into a four-bedroom house. With so much space, we decided to start renting out a guestroom on Airbnb. This form of house hacking worked out very well and allowed us to dramatically reduce our housing costs over the next few years. On average, we made about $10,000 per year just from renting out one room in our house. In 2018, we increased our yearly earnings by occasionally renting out our entire house while we were traveling.

- In June 2018, Bird and Lime scooters were launched in Minneapolis and I signed up to start charging them. This was a side hustle that just a few years before, I’d have never even been able to imagine. Charging these scooters also got me obsessed with the idea of electric micromobility – which is something that I talk about a lot now when I’m around people.

Even though these gigs were “beneath” someone of my pedigree, I still did them. In a way, I think it helped keep me grounded and was part of the reason I was able to avoid the massive lifestyle inflation that often happens with bigshot lawyers.

New Jobs, But Still Not Happy

I ended up making my last student loan payment in the summer of 2016, about 2.5 years after I had started to pay them off. Paying off my student loans bought me a lot more flexibility since I didn’t have to worry about having a $1,000 per month fixed cost anymore.

So, in the summer of 2016, right after I paid off my student loans, I left my biglaw associate job and took a job as a public sector attorney at a large state agency. The new job paid $75,000 per year – i.e. a massive $50,000 pay cut from the $125,000 salary that I had before.

Unfortunately, this new job wasn’t what I expected. My thought going in was that it would have lighter hours and would maybe be a better fit for me. I struggled a lot at my biglaw job due to the pressure of billing and dealing with different partners. A government job, I thought, would be the opposite of that, with no pressure to bill and maybe less office politics to deal with. That wasn’t the case though. Instead, I felt like it was just as much a struggle for me. I worked a lot of hours, hated having to do status reports and deal with meetings, and worse yet, I was now making less money than I made before.

After a year in public service, I made another job switch in the summer of 2017, leaving my state attorney job to take a job as a legal attorney/editor at my state bar association. My thinking here was that I just wasn’t happy being an attorney, so maybe working in a sort of law-adjacent job would do the trick. The salary for this new job was $57,000 a year, so I took another big pay cut in my search for the right job for me. I was able to take another pay cut because I’d been used to living on less and didn’t have many expenses since I had already paid off my student loans.

This new job wasn’t terrible, but I also found myself not enjoying it very much. It turns out I’m not really great at editing and once again, I didn’t enjoy having to be an office every day, working on someone else’s schedule.

Quitting My Job

During this stretch, I’d been working on building up this blog and doing my side hustles, but my idea for financial independence and my future still came from working a job in the legal field for a decade or longer. I never thought about looking outside the legal field or looking inward at myself to see what I could do. My future, for some reason, always relied on someone else paying me.

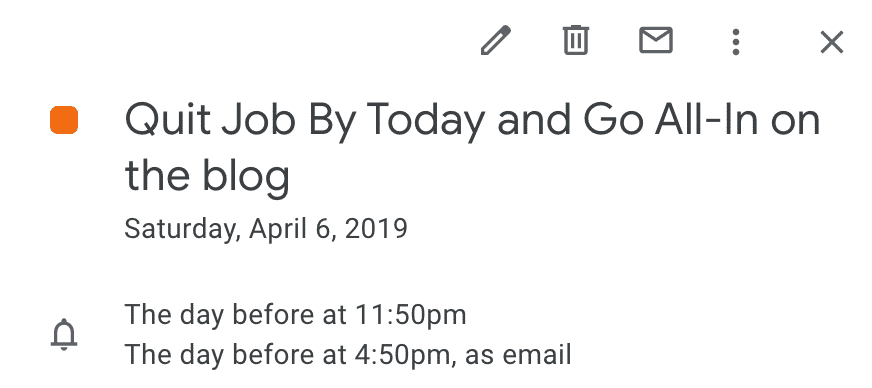

This changed in April 2018, when I had a really bad day at work. I ended up going to my calendar and writing a single goal to myself, which I still have saved. It said this:

After five years in the legal profession and three different jobs, it became clear to me that simply jumping around from one lawyer job to another wasn’t going to do the trick for me. I needed to take a leap and do something completely different.

I hit my goal sooner than I thought, quitting my job and making the leap to full-time blogging and side hustling in March 2019. Since then, I’ve felt a lot better and people have said they can see the difference in me.

There’s no doubt, my decade didn’t turn out the way I thought it would. At the beginning of the decade, I was all about following that clear, career path – studying hard in school, getting a good job, and working for someone until I could retire when I was old.

When I discovered financial independence, my view changed some more, with the idea that maybe I could move up that retirement date earlier. My future, however, would still be dependent on others employing me and paying me until I could quit and do what I wanted.

And when I started to believe in myself, my view changed some more again, with the idea that instead of waiting to do what I wanted to do, maybe I could go do it right now.

The important thing is, I took action to figure out what worked for me. This story obviously isn’t over – but one thing is for sure. I couldn’t have predicted my decade would turn out like this.

My Total Income Over The Decade

This is a personal finance blog, so of course, I think it’s helpful to see what type of income I’ve earned over the past 10 years of my life. Luckily, it’s not too difficult to pull this information up via the Social Security Administration website.

Below are what my taxable earnings have been from 2010 to 2018. I haven’t done my taxes yet for 2019, but most likely, my personal income will be around $60,000 to $70,000, so pretty similar to what it’s been in previous years.

- 2019: $60,000 – $70,000

- 2018: $76,479

- 2017: $76,676

- 2016: $98,140

- 2015: $114,478

- 2014: $106,675

- 2013: $41,963

- 2012: $20,160

- 2011: $526

- 2010: $10,822

One interesting thing I never realized. In the past decade, I made over $600,000 in income. That’s a lot more than I thought I had made.

A Timeline Of My Big Events Over The Past Decade

- August 2009: Moved back to my parent’s house. Spent the time working low-wage jobs and applied to law school.

- September 2010: Moved to Minnesota and started law school.

- September 2011: Interviewed and received an offer for a summer associate position at a large law firm in Minneapolis. I accepted the offer.

- December 2011: Met my wife, who was then in her second year of dental school.

- August 2012: Received an offer to return as an associate at the law firm I worked at over the summer.

- May 2013: Graduated from law school.

- September 2013: Started my first job as an associate attorney.

- June 2016: Paid off my student loans, then started a new job as a public sector attorney.

- April 2017: Got married.

- July 2017: Left my public sector attorney job and started a new job as a non-profit attorney/editor.

- March 2019: Quit my job to try my hand as a full-time blogger.

- Future: Unknown

This post may contain affiliate links.

More Recommended Ebike/Scooters

Check out these other ebikes and scooters I've reviewed:

- Urban Arrow Ebike – Last year, I made one of the largest purchases I’ve ever made – I bought a $9,000 electric cargo bike from Urban Arrow. In my Urban Arrow review, I will discuss what it is and why I decided to buy this bike, as well as discuss how impactful a bike like this can be on your journey to financial independence.

- Troxus Explorer Step-Thru Ebike – The Troxus Explorer Step-Thru is a fat-tire ebike that I’ve had the pleasure of riding for a while now. It has amazing power, great looks, and awesome range. If you’re looking for a great fat-tire ebike that offers a lot for the price, the Troxus Explorer Step-Thru is definitely one for you to consider. Check out my Troxus Explorer Step-Thru Review.

- Hovsco HovBeta Ebike – The HovBeta is a folding ebike with great specs and a lot of interesting features, and importantly, it’s sold at a good price point. I’ve had a blast commuting with it and using it to do deliveries with DoorDash, Uber Eats, and Grubhub. Check out my Hovsco HovBeta Ebike Review.

- Vanpowers Manidae Ebike – The Vanpowers Manidae is a fat tire ebike that I’ve been riding as my primary winter commuting bike and have also been using it to do food delivery with apps like DoorDash, Uber Eats, and Grubhub. After clocking in a decent number of miles with this ebike, I wanted to write a post sharing what my experience with the Vanpowers Manidae ebike has been like. Check out my Vanpowers Manidae Review.

- Sohamo S3 Step-Thru Folding EBike Review – A Great Value Folding Ebike – The Sohamo S3 Step-Thru Folding Ebike is an entry-level folding ebike that offers a lot of value for the price point. I’ve been riding the Sohamo S3 for a while now, putting the bike through its paces, and I have to say, this bike has exceeded all of my expectations. Check out my Sohamo Review.

- KBO Flip Ebike – The KBO Flip is an excellent bike. I’ve had a great time riding it and think it’s a versatile bike that can be used for a lot of purposes and can fit a variety of lifestyles. It’s worked out great for me as a general commuter bike and as a food delivery bike. Check out my KBO Flip Review.

- Hiboy P7 Commuter Ebike – The Hiboy P7 is an excellent electric commuter bike that’s offered at an affordable price point. The range and speed of this bike are both very good, so you won’t have any trouble getting anywhere you need to go with it. As a food delivery vehicle, this is also good – with how much range it offers, you’ll be able to work all day on a single charge. Check out my Hiboy P7 Commuter Electric Bike Review.

- Himiway Escape Ebike – The Himiway Escape is an interesting bike for anyone looking for a moped-style ebike. If you’re a gig economy worker, the Himiway Escape is particularly interesting and it’s possible to think of it as an investment, especially if you can opt to do deliveries with the Himiway versus using a car. It’s not cheap, but you can definitely make your money back when you compare the mileage you’ll put on your car versus using an ebike. Check out my Himiway Escape Bike Review.

- Espin Sport Ebike – The Espin Sport is a good ebike for someone who is looking for an ebike that feels and rides more like a regular bike. There are many ebikes that are really only bikes in name. In reality, they’re basically electric mopeds. The Espin Sport, by contrast, is a bike you could probably ride without the battery and you’d feel like you’re just riding a regular bike. Check out my Espin Sport Review.

- Varla Eagle One Scooter – The Varla Eagle One is an excellent scooter that can make sense for a lot of people. It can work as a primary mode of transportation. You can use it to work on gig economy apps like DoorDash, Uber Eats, and Grubhub. And it can also be a recreational vehicle if you’d prefer to use it for that. Check out my Varla Eagle One Review.

- Varla Falcon Scooter – The Varla Falcon is an excellent scooter that offers a good amount of power at a lower price point compared to more powerful scooters. It’s not exactly an entry-level scooter, nor is it a high-powered scooter. I think it fits somewhere in-between those two categories – an intermediate scooter if I had to give it a category. Check out my Varla Falcon Review.

- Hiboy S2 Scooter – The Hiboy S2 is an excellent entry-level commuter scooter that's perfect for someone looking to save some money in transportation costs and improve their commute. Check out my Hiboy S2 Review.

- Hiboy S2R Scooter – The Hiboy S2R is one of the more interesting electric scooters I’ve been able to test out. It’s not a high-powered scooter, but for an everyday transport option, it’s very useful, especially given some of the unique features that it has. Indeed, for the price, the Hiboy S2R might be the best value scooter I’ve used. Check out my Hiboy S2R Review.

- Fucare H3 Scooter – The Fucare H3 is a fun scooter and I’ve enjoyed testing it out. For a daily commuter or quick trips or errands, the Fucare H3 is probably the scooter I’ll use. It’s portable and easy to maneuver, so it’s just easier to take on the road when I need it. Check out my Fucare H3 Scooter Review.

More Recommended Investing App Bonuses

For additional investing app bonuses, be sure to check out the ones below:

- M1 Finance ($75) – This is a great robo-advisor that has no fees and allows you to create a customized portfolio based on your risk tolerance. You also get $75 for opening an account. Check out my M1 Finance Referral Bonus – Step-By-Step Guide.

- SoFi Invest ($25) – SoFi Invest is an easy brokerage account bonus that you can earn with just a few minutes of work. Use my SoFi Invest referral link, fund your SoFi Invest brokerage account with just $10 and you’ll get $25 of free stock. I also have a step-by-step guide for the SoFi Invest referral bonus.

- Robinhood (1 free stock) – Robinhood gives you a free stock valued between $2.50-$225 if you open an account using my referral link.

- Public (1 free stock) - Public gives you a free stock valued between $3-$70 if you open an account using my referral link.

More Recommended Bank Account Bonuses

If you’re looking for more easy bank bonuses, check out the below options. These bonuses are all easy to earn and have no fees or minimum balance requirements to worry about.

- Ally Bank ($100) – Of all the banks out there, Ally is, without a doubt, my favorite. At the moment, Ally is offering $100 to customers who open an eligible Ally account and meet the requirements. Here are the step-by-step directions to earn your Ally Bank referral bonus.

- Chime ($100) - Chime is a free bank account that offers a referral bonus if you use a referral link and complete a direct deposit of $200 or more. In practice, any ACH transfer into this account triggers the bonus. This bonus is easy to earn and posts instantly, so you’ll know if you met the requirements as soon as you move money into the account. I wrote a step-by-step guide on how to earn your Chime referral bonus that I recommend you check out.

- US Bank Business ($400/$1200) – This is a fairly easy bank bonus to earn, since there are no direct deposit requirements. In addition, you can open the Silver Business Checking account, which comes with no monthly fees. Check out how to earn this big bonus here.

- Current ($50) – Current is a free fintech bank that’s offering new users a $50 referral bonus after signing up for an account using a referral link. Current is an easy bonus to earn and also gives you access to three savings accounts that pay you 4% interest on up to $2,000. That means you can put away up to $6,000 earning 4% interest. That’s very good and makes Current an account I recommend to everyone. Check out my step-by-step guide on how to earn your Current Bank bonus.

- Novo Bank ($40) - Novo bank is a free business checking account that’s currently offering a $40 bonus if you open a Novo business checking account using a referral link. In addition to being a good bank bonus, Novo is also a good business checking account. It has no monthly fees or minimum balance requirements and operates a good app and website. Indeed, it’s the business checking account I currently use for this blog. Check out my post on how to easily open a Novo account.

- Varo ($25) – Varo is a free fintech banking app similar to Chime or Current. It’s currently offering a $25 bonus to new users that open a new Varo account with a referral link. The bonus for this bank is very easy to meet, all you need to do is spend $20 within 30 days of opening your Varo account. Check out my step-by-step guide to learn how to earn this bonus.

Kevin is an attorney and the blogger behind Financial Panther, a blog about personal finance, travel hacking, and side hustling using the gig economy. He paid off $87,000 worth of student loans in just 2.5 years by choosing not to live like a big shot lawyer.

Kevin is passionate about earning money using the gig economy and you can see all the ways he makes extra income every month in his side hustle reports.

Kevin is also big on using the latest fintech apps to improve his finances. Some of Kevin's favorite fintech apps include:

- SoFi Money. A really good checking account with absolutely no fees. You'll get a $25 referral bonus if you open a SoFi Money account with a referral link, and an additional $300 if you complete a direct deposit.

- 5% Savings Accounts. I'm currently getting 5.24% interest on my savings through a company called Raisin. Opening a Raisin account takes minutes to complete, it's free, and all of your funds are FDIC-insured. I explain how it works, why I'm now using it to store my emergency fund and any other cash savings I have, and why I recommend everyone check it out in this review.

- US Bank Business. US Bank is currently offering new business customers a $400/$1200 signup bonus after opening a new account and meeting certain requirements.

- M1 Finance. This is a great robo-advisor that has no fees and allows you to create a customized portfolio based on your risk tolerance. You also get $75 for opening an account.

- Empower. One of best free apps you can use to monitor your portfolio and track your net worth. This is one of the apps I use to track my financial accounts.

Feel free to send Kevin a message here.

Loved your story. Keep it up. Not sure how I ended up on your blog, but I will be coming back. 😉

I’ve been looking forward to reading your second installment. It’s very insightful to read about someone thinking through what really makes them happy in a profession. Great work! I love your blog and have pointed many colleagues in your direction when they inevitably share dissatisfaction with Attorney life. My favorite post you’ve done so far is the post about prestige. It helped me better articulate my own reasons for leaving regular law practice and I’m very grateful for that. Keep up the good work!

Thanks Teja! Appreciate the support. The prestige issue is something I still deal with, especially when people ask me what I do and I say I’m a “writer” or “blogger” which sort of sounds like I’m a bum.

Great article, thank you for sharing!!! Do you think you’ll ever, eventually go back to a law job or a traditional job?

What is the hardest part of being your own boss? What’s the best part? do you miss anything about practicing law?

What are your goals for 2020?

I’M NOSY!

I don’t think I can go back to law. My plan B and plan C are go back to school and get a library science degree to try to be like a librarian or law librarian, or go to a coding boot camp and learn to code and then just get a job doing that.

Best part of being my own boss is not having the anxiety of performance reviews and that kind of stuff. That always brought me a lot of anxiety.

Hardest part is, of course, motivating myself to hustle. In a job, my motivation is to not get fired or embarrassed at work. When you work for yourself, the motivation I guess is to be able to survive, which is sort of a different feel.

The only thing I miss about practicing law is the prestige it brought me, because it made me feel important.

Your story is so inspiring! I never thought to ask this before, but do you plan to keep up with your law license now that you’re not actively practicing law? I’ve only been practicing law for two years and I’m already looking at exit plans myself. Whether or not to keep up with my bar dues and CLE requirements when I leave to invest in real estate full time is something I’m trying to decide is worth it or not.

So, I am keeping my law license right now just because, like many of us, I’m scared and like the comfort of knowing I could maybe go back to something if I had to.

It’s $250 per year for me to keep my license and then I think I can mooch free CLEs from affinity groups and from my friends that work at law firms.

I find your blog very intriguing! Some questions immediately popped into my mind…I’m wondering throughout your entire career journey, was your wife always supportive of your decisions or were there moments of reluctance? In addition, because your wife is a dentist, which presumably makes a good salary, did that enable you to take more risk to leave your higher paying job(s)? Lastly, will any of your perspectives change when/if you have children? Babies and college can be expensive! 🙂

Good question Annie. Yes, my wife was supportive throughout. She could tell that I was not doing well working for others. Of course, there was reluctance, but we’ve been really seeing that money is out there.

My wife is absolutely the reason I made this jump and makes it much easier. In fact, the only reason I didn’t make the jump earlier was because we wanted to make sure my wife was settled in her business before jumping. She owns her own practice, so we’re already pretty big risk takers.

Children are on the horizon, and I don’t think it’ll change my perspective. If I made more money as a lawyer, then sure, but for me, the way I look at it, my income ceiling is far higher working for myself then it is doing law unless I went back into corporate law, which I know I cannot do for the rest of my life.

that’s guts – to leave high paying job to pursue satisfying ones 🙂 lovely read mr. panther.

Thanks! There’s a fine line between guts and stupidity. I guess we’ll see which one it is. In a few more months, it’ll be a year since I quit my job to go all-in on myself.